A brokerage firm has upgraded Dixon Technologies to 'Buy' with a target price of ₹14,200. The upgrade reflects optimism around rising smartphone average selling prices and export growth. Investors are focused on upcoming contributions from the Vivo joint venture and the scaling of IT hardware production to meet FY28 and FY29 growth targets.

What Happened

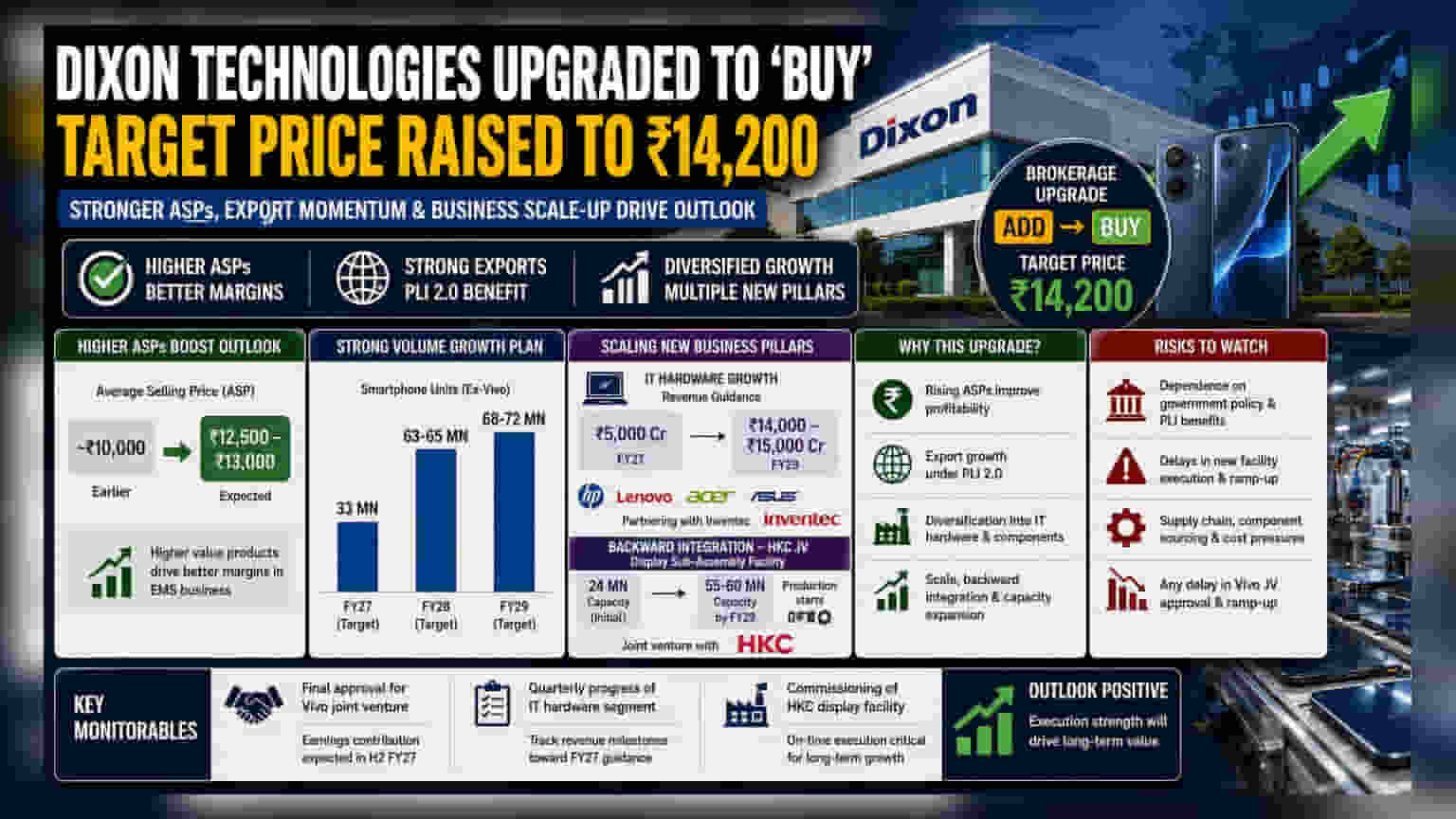

A prominent brokerage has upgraded Dixon Technologies from 'Add' to 'Buy', raising the target price to ₹14,200. This change in stance comes as analysts anticipate stronger financial performance driven by an increase in smartphone average selling prices (ASPs). The company is also seeing momentum in export volumes under the government’s PLI (Production Linked Incentive) 2.0 scheme, which rewards companies for increasing local manufacturing and exports.

The Shift to Higher Value Products

A key reason for the positive outlook is the expected rise in the average price of smartphones Dixon manufactures. Analysts estimate that average selling prices may climb from around ₹10,000 to a range of ₹12,500–₹13,000. In the electronics manufacturing services (EMS) business, selling higher-value products often allows companies to improve their profit margins, as the cost of manufacturing does not always rise at the same rate as the final product price.

Dixon is also planning for significant volume growth. The company is on track to hit its target of approximately 33 million smartphone units (excluding Vivo) for FY27. Looking further ahead, it has set ambitious targets of 63-65 million units for FY28 and 68-72 million units for FY29, which would signal a major expansion of its operations.

Scaling New Business Pillars

Beyond smartphones, the company is diversifying into IT hardware, which includes making products for brands like HP, Lenovo, Acer, and Asus. While this segment faced delays in the past, it is now expected to scale up significantly. The company has maintained its FY27 revenue guidance for this segment at ₹5,000 crore, with projections jumping to ₹14,000-15,000 crore by FY29. To support this, Dixon is partnering with Inventec for servers and accessories.

Furthermore, the company is moving toward 'backward integration'—meaning it is starting to make its own components rather than importing them. A new joint venture with HKC for a display sub-assembly facility is set to start production in the fourth quarter of FY27. This is a critical move, as it gives Dixon more control over its supply chain and costs, with an initial capacity of 24 million displays, eventually ramping up to 55-60 million by FY29.

Execution and Policy Risks

While the outlook is positive, investors should be aware of the specific risks in the electronics manufacturing sector. The business is heavily dependent on government policy, particularly the PLI schemes. If there are changes in government policy or delays in receiving benefits, it could impact profit margins.

Additionally, there is the risk of execution. Bringing large-scale facilities like the HKC display plant or the IT hardware production lines to full capacity on time is complex. Delays or cost increases in setting up these plants could result in lower earnings than what analysts currently project.

What Investors Should Track Next

The most immediate monitorable is the final approval for the joint venture with Vivo. Once operational, this is expected to contribute to earnings by the second half of FY27. Investors will also track the quarterly progress of the IT hardware segment to ensure it is meeting the revenue milestones that support the long-term growth targets. Finally, monitoring any updates on the commissioning of the HKC display facility will be important to confirm the company’s ability to execute its expansion plans as promised.