HDFC Securities has set a target price of Rs 2,080 for Dalmia Bharat, pointing to volume growth and strategic acquisitions. However, the brokerage also highlighted a rise in debt and reduced profit estimates for the coming years due to the costs associated with these expansion plans.

What Happened

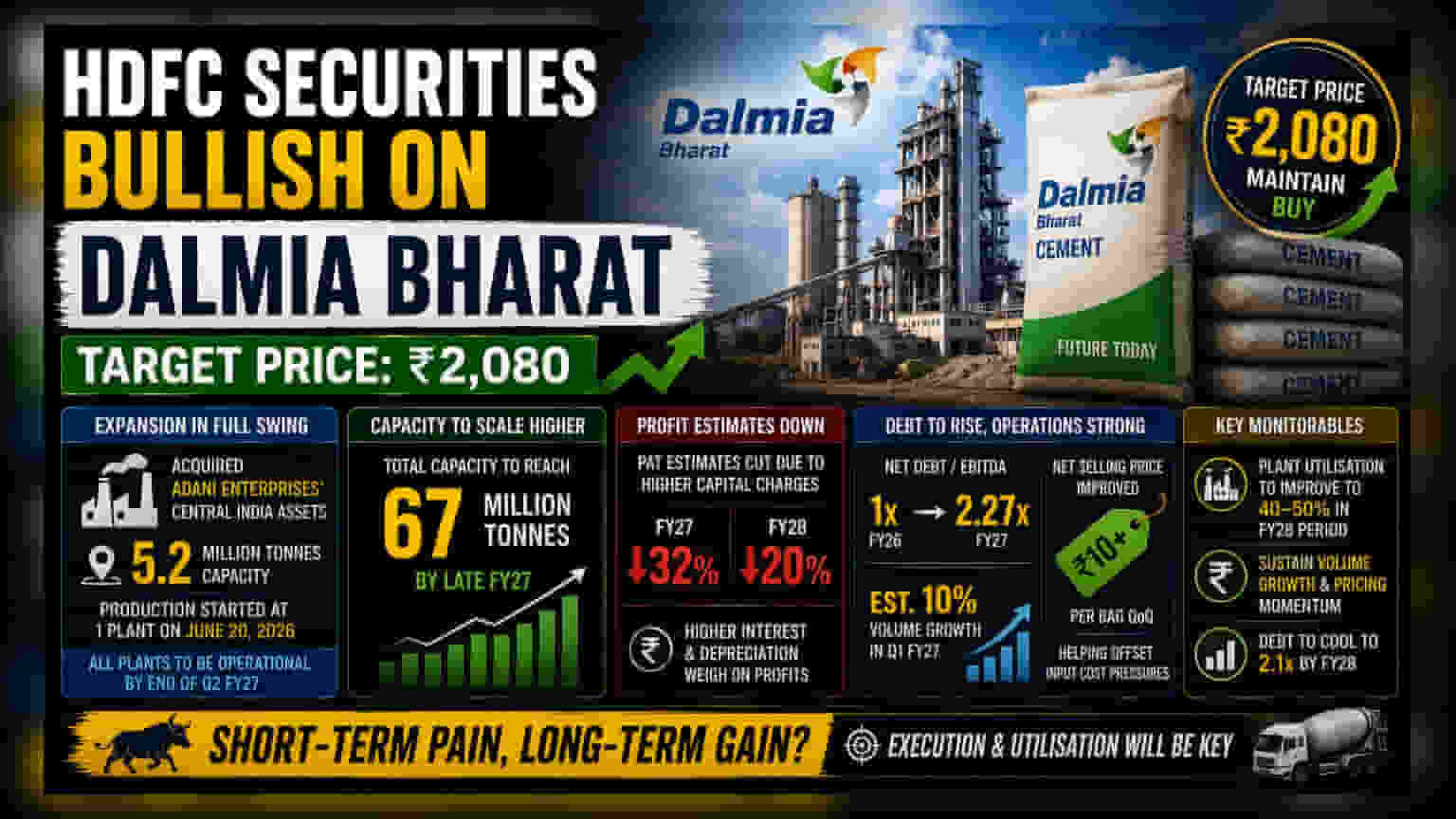

HDFC Securities has released a report on Dalmia Bharat, setting a target price of Rs 2,080 for the stock. The brokerage has maintained a positive outlook, citing an expected increase in industry demand and the company’s ongoing efforts to expand its production capacity. While the report highlights operational strengths, it also warns of a temporary impact on the company's bottom line due to recent large-scale investments.

The Expansion Strategy

A core part of the brokerage's outlook involves the company’s recent acquisition of assets from Adani Enterprises. Specifically, Dalmia Bharat acquired assets in the central region with a capacity of 5.2 million tonnes. The report notes that production has already begun at one of these facilities as of June 20, 2026. The firm expects all acquired plants to be fully operational by the end of the second quarter of the 2027 fiscal year. These additions, combined with other projects, are projected to increase the company's total capacity to 67 million tonnes by late 2027.

Why Profit Estimates Were Revised

Despite the growth in capacity, HDFC Securities has lowered its profit after tax (PAT) estimates for fiscal years 2027 and 2028 by 32% and 20%, respectively. This revision is primarily driven by the financial costs of expansion, often referred to as higher capital charges—which include the interest payments on loans taken for these acquisitions and the depreciation costs of new machinery. Because these costs are front-loaded, they are expected to weigh on the company's reported profit in the near term.

Debt and Operational Health

The brokerage highlighted that the company's net debt to core operating profit (EBITDA) ratio is set to rise, moving from 1x in the 2026 fiscal year to an estimated 2.27x in 2027. This increase reflects the debt taken on to fund the recent acquisitions. However, the report also points to some positive operational signs. The company is estimated to achieve 10% volume growth year-on-year for the first quarter of fiscal year 2027. Additionally, net selling prices for cement have improved by more than Rs 10 per bag compared to the previous quarter, which helps the company manage rising energy and packaging costs.

What Investors Should Track

For investors, the key monitorables will be how quickly Dalmia Bharat can improve the utilization rates of its newly acquired plants. The brokerage anticipates utilization to reach 40-50% in the 2027-2028 period. Tracking whether the company can maintain volume growth and effectively manage its debt levels—which are expected to cool to 2.1x by 2028—will be important for assessing the long-term impact of this expansion strategy.