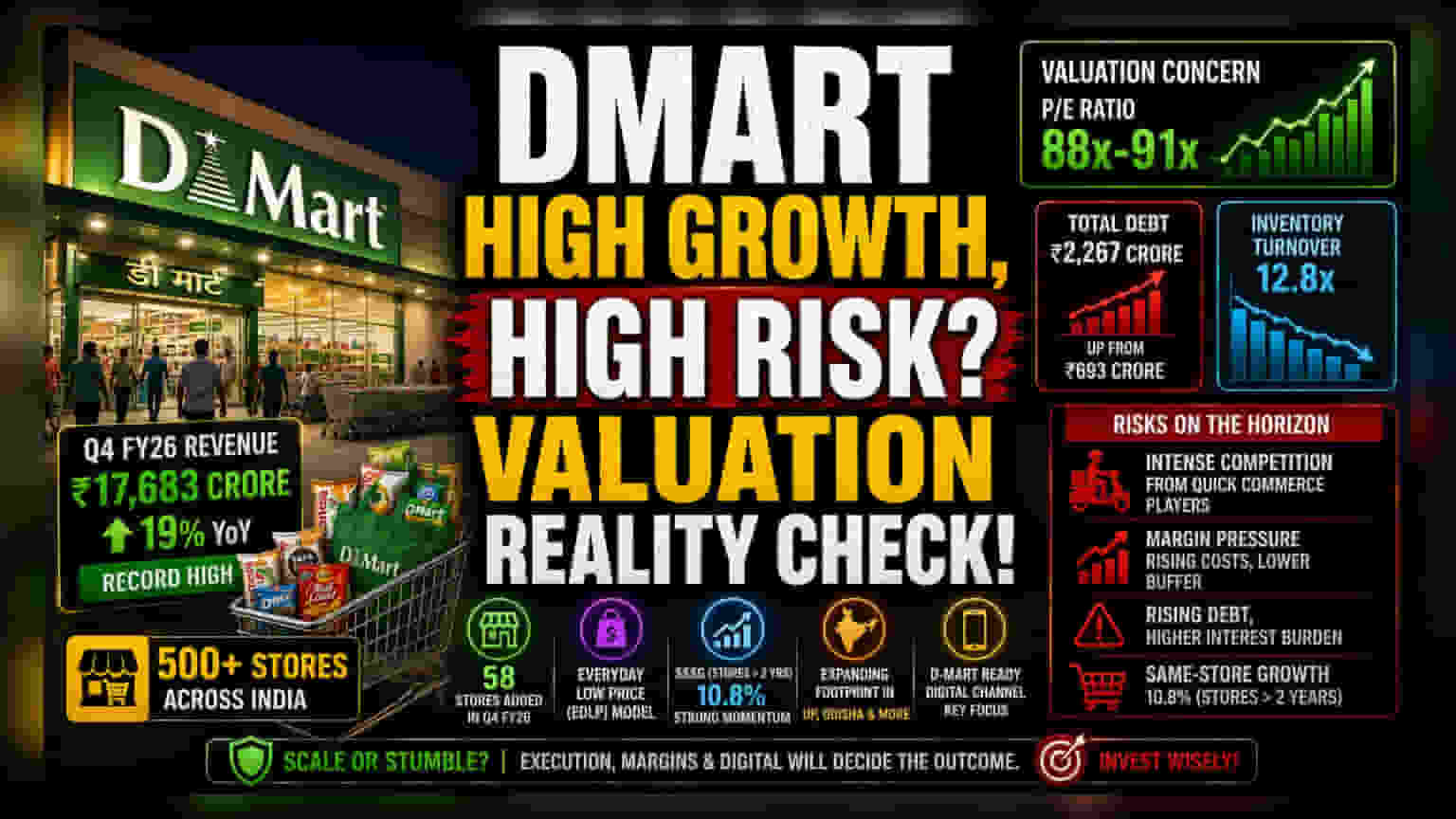

The Valuation Gap and Operational Reality

Following a record-breaking fiscal year that saw Avenue Supermarts cross the 500-store milestone, the stock is currently trading at a P/E ratio of approximately 88x to 91x. This valuation remains a point of contention for institutional investors. While the company delivered a robust 19% revenue growth in Q4 FY26, reaching ₹17,683 crore, the market’s reaction has been lukewarm, often retreating after initial gains. The core tension lies between the company's traditional “Everyday Low Price” (EDLP) model and the modern need for rapid digital adaptation, as investors weigh the benefits of physical footprint expansion against the encroaching threat of quick-commerce giants.

The Strategic Pivot: Scale Versus Speed

Unlike the measured, slow-burn expansion that once defined the company, the recent addition of 58 stores in a single quarter signals a departure from its historical cadence. This pivot appears designed to capture market share before competitors saturate the urban addressable market. However, this aggressive capital deployment has tangible side effects. Total debt has risen to ₹2,267 crore in FY26, up from ₹693 crore the previous year, while inventory turnover has softened to 12.8x. While same-store sales growth for locations older than two years clocked in at a healthy 10.8%, the broader margin profile is under pressure, leaving little room for error in a competitive retail environment.

The Forensic Bear Case: Structural Weaknesses

From a risk-averse perspective, the company’s transition into a more debt-reliant expansion model is a departure from its once pristine, debt-free balance sheet. Rising competition from entities like Zepto, Blinkit, and Swiggy Instamart poses a structural threat to the company’s core FMCG segment, where speed is becoming more valuable than the price gaps DMart historically maintained. Furthermore, key profitability metrics—specifically Return on Capital Employed (ROCE) and Return on Net Worth (RONW)—have seen a slight contraction. Analysts remain concerned that if the company fails to translate this new store footprint into significantly higher throughput per square foot, the current premium valuation could face a sharp correction.

The Future Outlook

Brokerage consensus remains split. While some analysts maintain a constructive view, citing the strong 19% revenue trajectory and successful penetration into new states like Uttar Pradesh and Odisha, others advise caution, noting that the retail landscape has fundamentally shifted. The company’s ability to defend its market share through its digital channel, D-Mart Ready, will be critical. Moving into FY27, investors will be closely watching whether the company can stabilize its margins while continuing to scale, or if the rising interest burden and competitive pricing environment will force a re-evaluation of its growth targets.