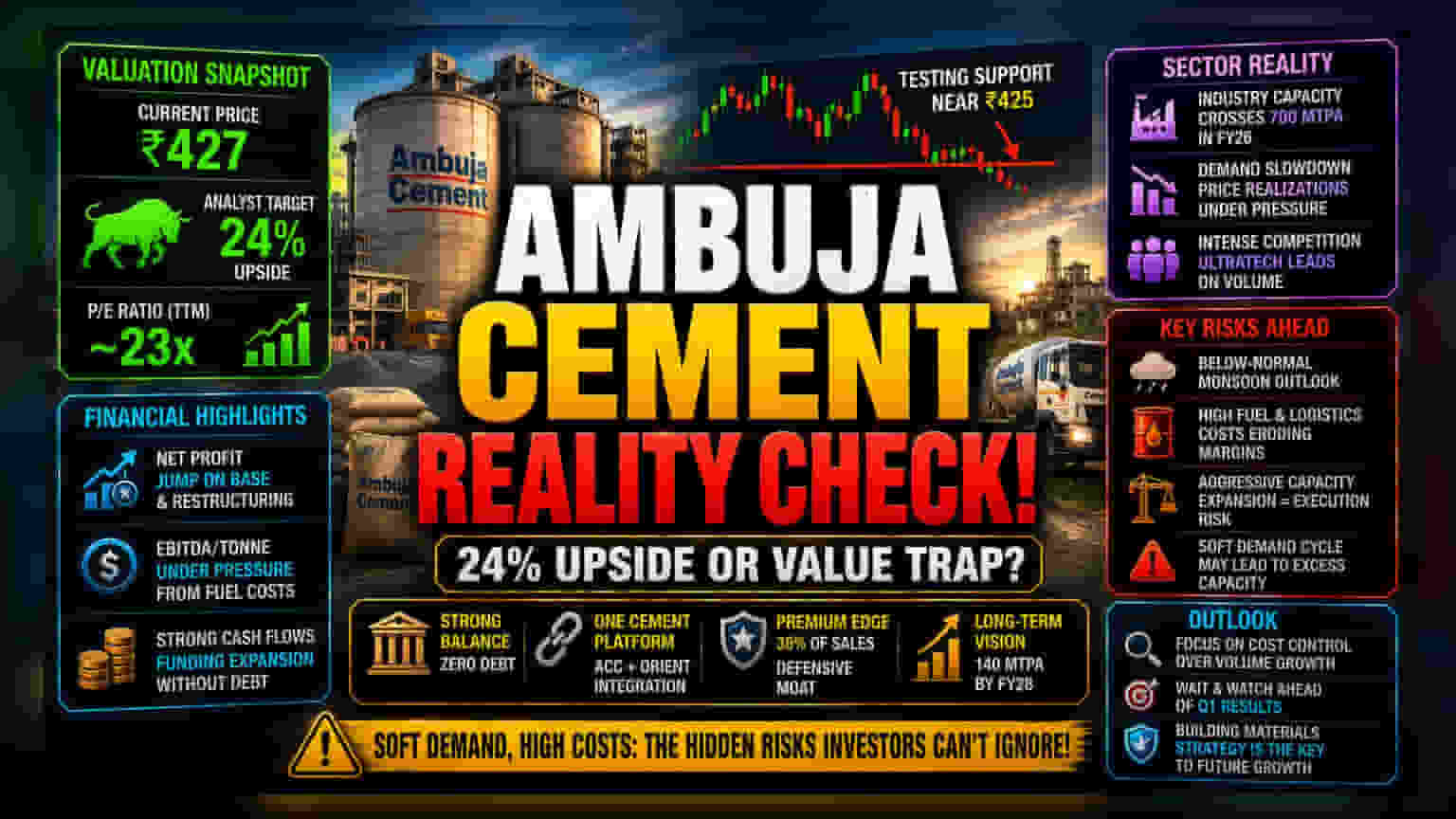

The Valuation Gap

While institutional sentiment remains theoretically bullish, the market’s current pricing of Ambuja Cements suggests a more tempered reality. Trading at approximately ₹427, the stock has recently tested support levels near ₹425, reflecting broader sector malaise. Although analysts project an ambitious 24% upside, the valuation multiple—currently sitting at a trailing P/E of roughly 23x—indicates that investors are increasingly sensitive to the gap between long-term capacity expansion goals and the immediate pressure on profitability. The disparity between brokerage targets and live market performance highlights a growing skepticism regarding the speed at which operational efficiencies can offset rising fuel and logistics costs.

The Analytical Deep Dive

Ambuja’s strategy relies heavily on the integration of its 'One Cement Platform,' which recently received 'no objection' letters from the NSE and BSE regarding the amalgamation of ACC and Orient Cement. While this consolidation is intended to drive economies of scale and optimize supply chain logistics, the company is currently navigating a soft demand cycle. Industry capacity has expanded rapidly, crossing 700 MTPA in FY26, which has naturally intensified competitive pressure. Unlike historical cycles where volume growth was consistent, the current market is witnessing a deceleration in demand, leading to muted price realizations. The company’s focus on premium cement—which grew to 36% of trade sales—is a defensive moat, but it faces stiff competition from peers like UltraTech, which remains the volume leader even as sector margins remain constrained.

The Forensic Bear Case

Investors should look past the headline growth metrics. The company’s recent performance shows that while net profit can jump due to base effects and operational restructuring, the underlying EBITDA-per-tonne remains vulnerable to fuel price volatility and global geopolitical friction. Management has already signaled a 'soft' outlook for FY27, specifically citing below-normal monsoon forecasts and the impact of state-level demand fluctuations. Furthermore, the aggressive capacity-led strategy—aiming for 140 MTPA by FY28—creates significant execution risk. Should the anticipated demand surge fail to materialize, the company risks holding excess capacity in a price-sensitive market, which would inevitably lead to further margin erosion. The recent withdrawal of Alok Sanghi’s legal challenge, while positive for governance optics, underscores the complexity of the ongoing integration and the administrative overhead that comes with such rapid M&A activity.

The Future Outlook

As the industry moves toward a commoditized model, Ambuja’s future hinges on its ability to transition from a pure cement manufacturer to a holistic building materials provider. Consensus remains cautious, with a wait-and-watch approach prevailing ahead of quarterly results. If the company successfully leverages its zero-debt balance sheet to weather the current cycle, it may stabilize, but the immediate path forward will likely be defined by the management’s ability to control operational costs rather than relying on volume-driven revenue spikes.