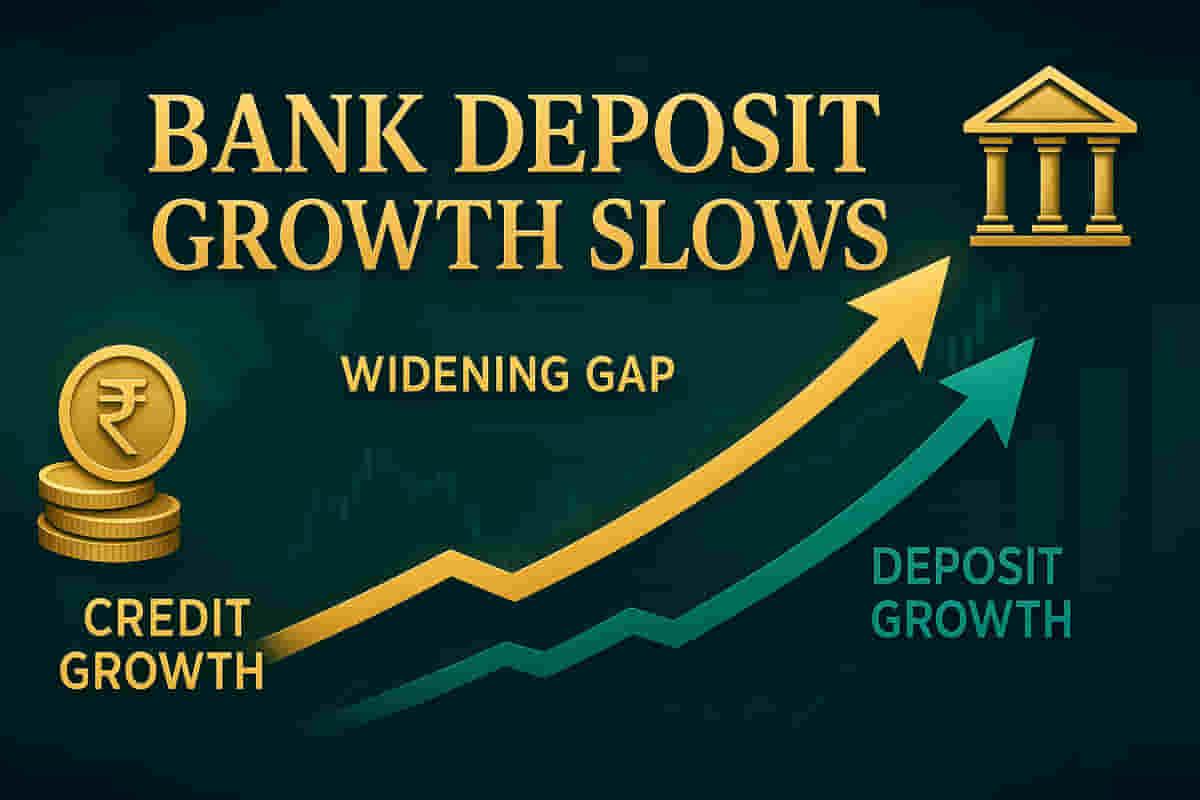

Bank Deposit Growth Slows to 9.5%, Widening Gap with Credit Growth

Banking/Finance

|

30th October 2025, 5:12 PM

▶

Short Description :

Detailed Coverage :

Data from the Reserve Bank of India reveals a further slowdown in bank deposit mobilization, with annual growth standing at 9.5% by October 17, a decrease of 40 basis points from the 9.9% recorded a fortnight earlier. In contrast, yearly credit growth saw a marginal improvement, staying around 11.5%, slightly up from 11.4% previously. This divergence has led to a wider gap between credit and deposit growth rates. Banks are facing challenges in attracting public deposits because current low interest rates make them less appealing. The situation is particularly acute for Current Account and Savings Account (CASA) deposits, as customers are moving their liquid funds to fixed deposits, which offer better returns.

Impact This trend could pressure banks' liquidity and net interest margins if it persists, potentially leading to higher lending rates or increased competition for deposits. The widening gap suggests strong demand for credit, which banks must fund. The Reserve Bank of India will be monitoring this closely. Impact Rating: 7/10

Difficult Terms Basis points: A basis point is one-hundredth of a percentage point, or 0.01%. It is commonly used in finance to denote small changes in interest rates or other percentages. Credit growth: The rate at which the total amount of loans issued by banks to individuals and businesses increases over a period. Deposit mobilisation: The process by which banks attract funds from the public in the form of savings, current, and fixed deposits. CASA (Current Account and Savings Account): These are typically low-cost deposits for banks, representing funds that customers can access immediately. They are crucial for a bank's profitability. Floating funds: Funds that are not tied up in long-term investments and can be moved easily by investors. Time deposits: These are fixed deposits where money is deposited for a specific period, offering a fixed interest rate. They are generally less liquid than savings accounts.