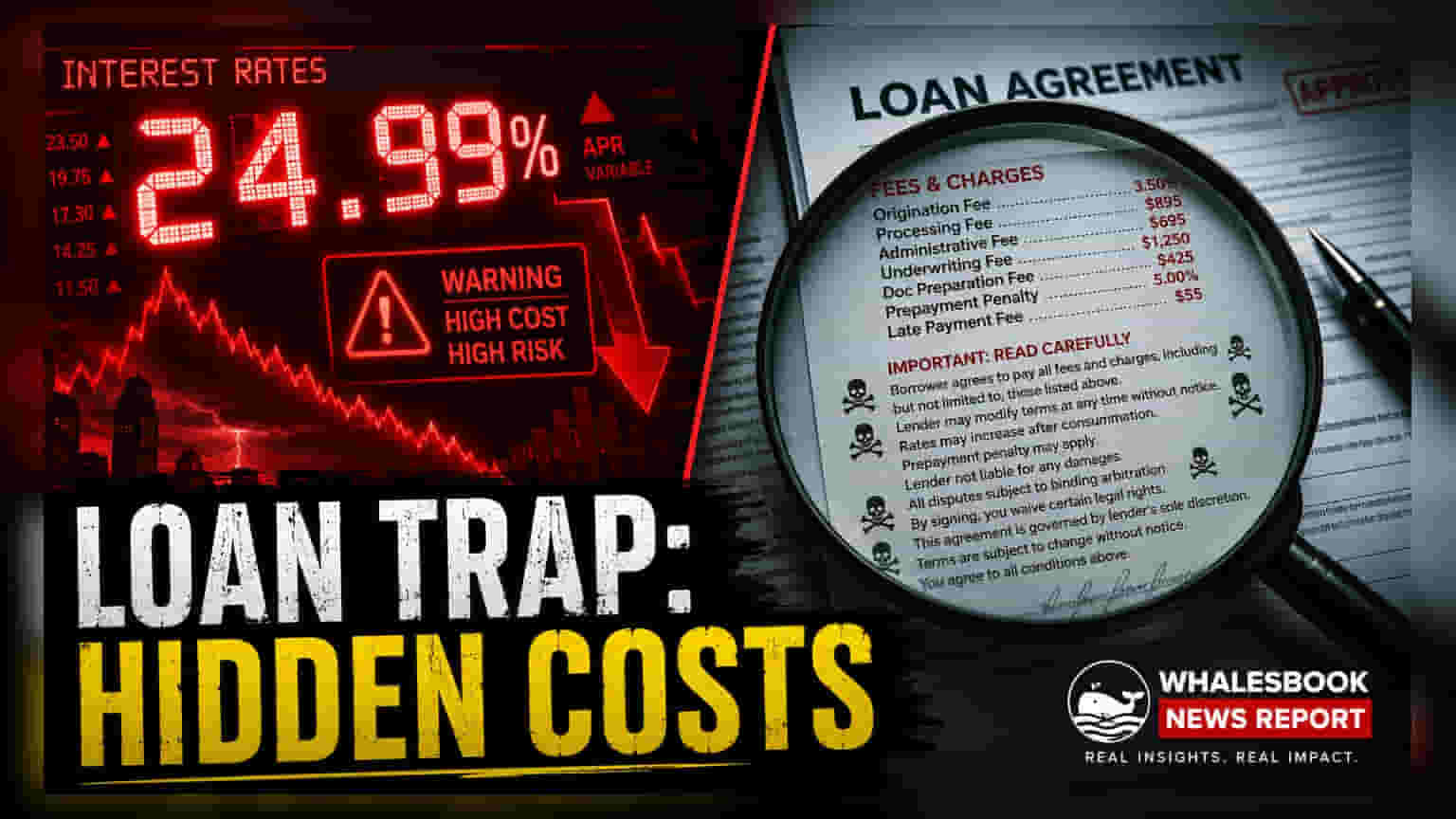

Focusing only on advertised interest rates can mislead borrowers regarding the total cost of a loan. Additional charges like processing fees, insurance, and prepayment penalties significantly increase repayment obligations. Investors and borrowers should conduct a comprehensive review of all loan terms to understand the actual financial burden.

What Happened

Borrowers often prioritize low nominal interest rates when selecting a loan, but these figures frequently exclude significant additional expenses. Lenders levy various fees—ranging from processing costs and insurance premiums to documentation charges—that effectively reduce the net loan amount received or increase the total repayment sum. Because these charges are often itemized separately or deducted upfront, they can create a disparity between the advertised rate and the actual cost of borrowing. Recognizing these hidden costs is essential for making informed financial decisions, as they can quickly negate the perceived savings from a lower headline interest rate.

The Impact of Upfront Fees

Processing fees are among the most common hidden costs. While they appear as a small percentage of the loan value, they are often deducted directly from the principal before the funds are disbursed to the borrower. For example, if a borrower expects to receive the full principal amount, the deduction of a processing fee means they are effectively borrowing less capital than requested while still paying interest on the full amount. This nuance is frequently overlooked, yet it raises the effective annual percentage rate beyond what the lender advertises.

Why Insurance and Administrative Charges Matter

Financial institutions frequently bundle products such as credit protection insurance or add-on administrative services with loan packages. While these may provide security in specific scenarios, they are not free. These premiums add to the total debt obligation, often without the borrower fully assessing whether the cost aligns with the perceived benefit. Similarly, administrative and verification fees, though individually minor, accumulate during the loan process, contributing to a higher total repayment liability than a simple interest rate calculation would suggest.

Managing Penalties and Repayment Terms

Loan agreements often contain clauses that restrict early repayment through prepayment penalties. These fees are designed to protect the lender's interest income but can severely undermine a borrower's strategy to save money by clearing debt ahead of schedule. Furthermore, late payment penalties represent a significant risk; a single missed EMI can trigger substantial fines and accrued interest, complicating the borrower's financial position. Understanding these conditions before signing a loan contract is critical to maintaining a predictable repayment schedule and avoiding unnecessary financial strain.