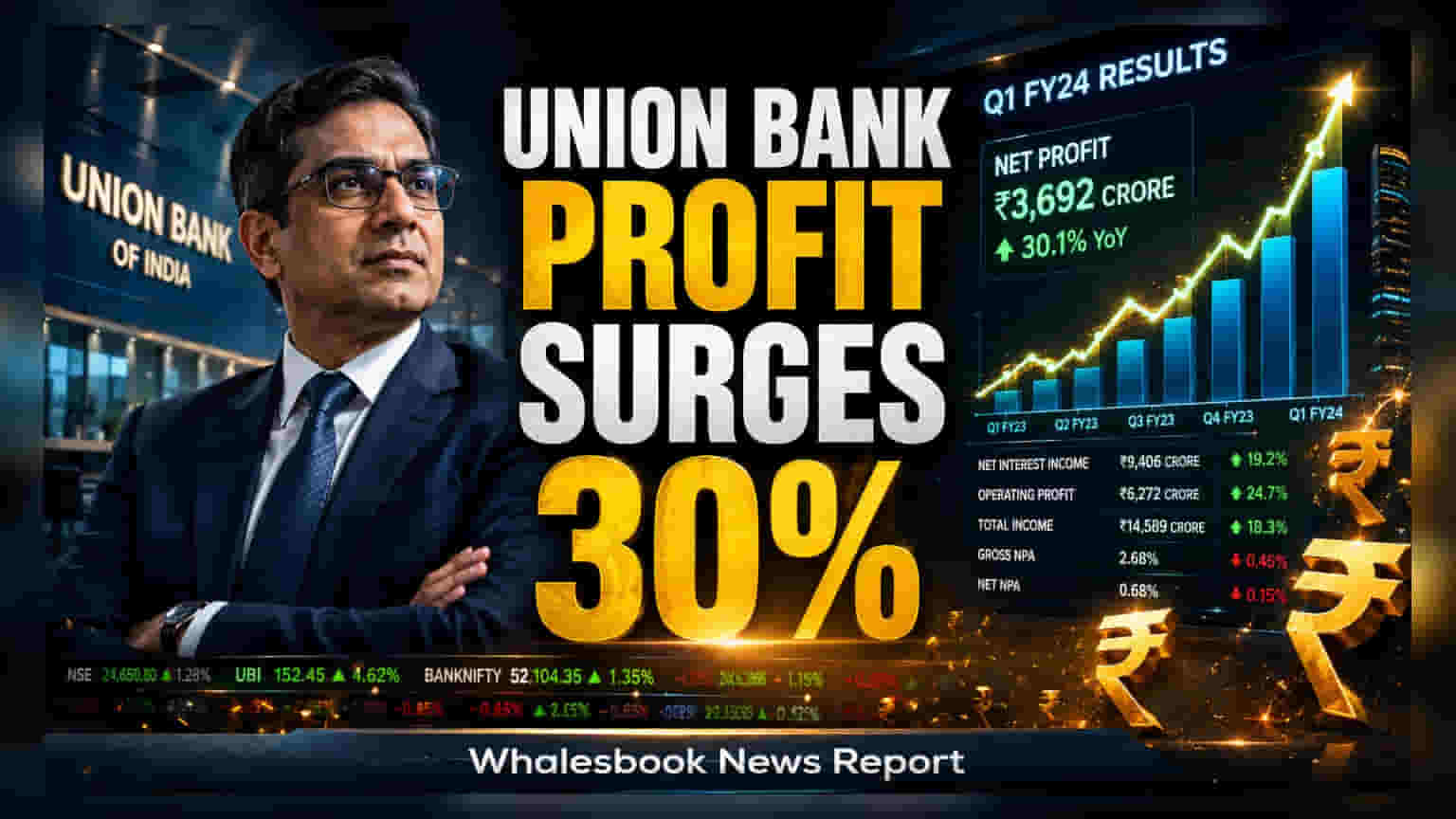

Union Bank of India reported a 29.5% increase in net profit for the June quarter, driven by higher net interest income and improved asset quality. The bank's gross NPA ratio declined to 2.65%, highlighting a strengthening balance sheet for the public sector lender.

Union Bank of India has reported a net profit of ₹5,332 crore for the quarter ended June 2026, marking a 29.5% increase compared to the same period last year. This performance was supported by a 10.1% rise in net interest income, which reached ₹10,037 crore. The bank also benefited from a steady expansion in its loan book, with global advances growing by 12.5% to touch ₹10.96 lakh crore.

Asset Quality and Margin Trends

The bank showed progress in managing its asset quality, which is a key metric for investors tracking public sector banks. The gross non-performing asset (NPA) ratio, which represents the portion of total loans that are overdue, improved significantly to 2.65% from 3.52% in the previous year. Similarly, the net NPA ratio reduced to 0.47%. The bank also reported a higher provision coverage ratio of 95.05%, suggesting that it has set aside adequate funds to cover potential bad loans. Furthermore, the net interest margin—a measure of profitability on interest-earning assets—improved slightly to 2.80%.

Revenue Sources and Capital Strength

Non-interest income, which includes fee-based earnings, contributed ₹4,603 crore to the total revenue. A notable highlight was the 45% surge in fee income to ₹3,215 crore, which helped the bank maintain overall revenue growth despite a decline in treasury income. On the deposit front, the bank saw a 3.5% growth in global deposits to ₹12.83 lakh crore, with the domestic CASA ratio—representing the proportion of low-cost savings and current account deposits—reaching 35.1%. A higher CASA ratio typically helps banks manage their cost of funds more efficiently.

The bank’s capital adequacy ratio, which measures the capital available to support risks and absorb losses, stood at 18.46%. Other profitability metrics, including the return on assets at 1.36% and return on equity at 17.23%, indicate an improvement in the bank's operational efficiency. The book value per share also rose to ₹162.15.

Monitorables for Investors

While the recent results indicate a positive trend in profitability and asset quality, investors may continue to track the bank’s ability to sustain margin levels in a changing interest rate environment. Other important areas to watch include the consistency of fee income growth and the bank's ability to maintain a low credit cost as it continues to expand its loan portfolio. The next update on quarterly loan growth and the sustainability of deposit mobilization will be important factors in understanding the bank's long-term performance trajectory.