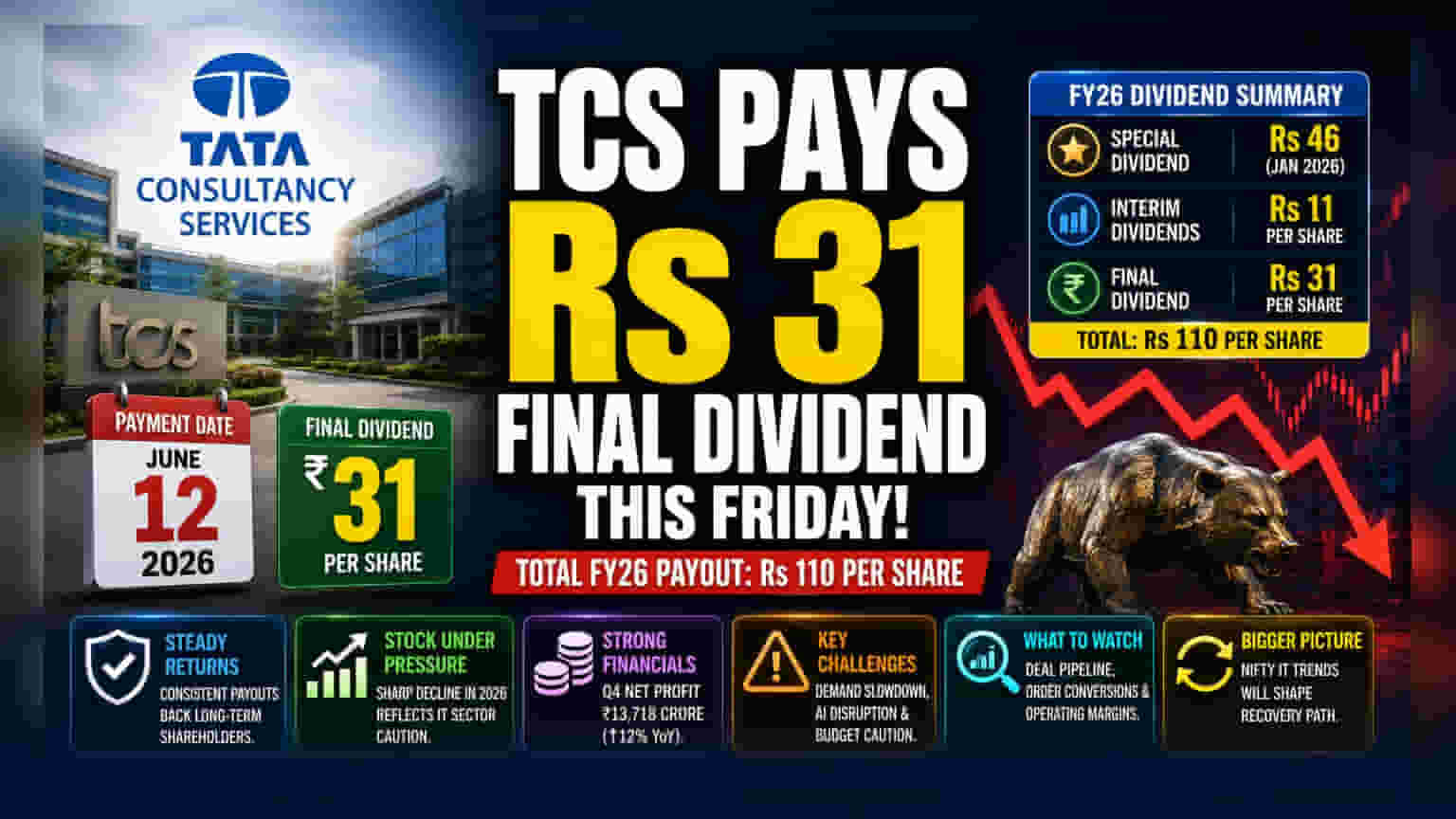

What Happened

Tata Consultancy Services (TCS) is scheduled to pay its final dividend of Rs 31 per equity share this Friday, June 12, 2026. The amount will be credited directly to the demat accounts of eligible shareholders. This final payment marks the conclusion of the company’s dividend cycle for the 2026 fiscal year, bringing the total payout for the year to Rs 110 per share. This includes the special dividend of Rs 46 paid in January and interim dividends totaling Rs 11 per share.

Why This Matters For Investors

For long-term shareholders, this dividend reinforces TCS's long-standing strategy of returning excess cash to investors. Even as the company navigates a challenging business environment, its ability to maintain consistent payouts provides a steady income stream. However, the dividend yield must be weighed against the recent decline in the share price. While dividends provide a cushion, the primary concern for many investors remains the stock's capital appreciation, which has been difficult to come by given the current market sentiment toward the IT sector.

The Stock Performance Gap

Despite the company’s solid financial track record and consistent dividend policy, TCS shares have struggled significantly in 2026. The stock has seen a sharp decline year-to-date, reflecting a broader trend of investor caution regarding large IT companies. This price correction suggests that the market is focusing less on the company's dividend history and more on its ability to grow revenue in a tough global economy. Investors have reacted to these concerns by reducing their holdings, leading to the notable volatility and price erosion seen over the past several months.

The Bigger Financial Context

Financially, TCS remains stable. For the January-March quarter, the company reported a consolidated net profit of Rs 13,718 crore, a 12% increase compared to the same period last year. Revenue grew nearly 10% year-over-year to Rs 70,698 crore. However, beneath these headline figures, the revenue growth on a constant currency basis has remained largely flat over the full year, indicating that the company is not immune to the slowdown in discretionary IT spending. While operating margins have held up well, investors are closely watching whether the company can drive meaningful growth in the coming quarters.

Sector Pressure and Risks

The primary challenge for TCS and its peers is the cautious approach taken by clients in the US and Europe. Many global businesses have tightened their technology budgets, delayed decision-making on large projects, and are carefully evaluating investments in artificial intelligence before committing large amounts of capital. This uncertainty has created a ripple effect across the Indian IT services sector, leading to lower-than-expected deal velocity. Additionally, the rapid emergence of AI has caused existential concerns about how traditional outsourcing models will evolve, adding a layer of risk that keeps valuations under pressure.

What Investors Should Track

Moving forward, the key monitorable is not just the dividend, but the demand environment. Investors may track commentary from management regarding the pipeline for large deals and any signs of recovery in discretionary client spending. The speed at which the company converts its order book into revenue and its ability to maintain healthy profit margins despite wage inflation will be critical factors. Additionally, monitoring the broader Nifty IT index can provide insights into whether the current sell-off is a reflection of company-specific issues or a wider shift in global investor sentiment toward technology stocks.