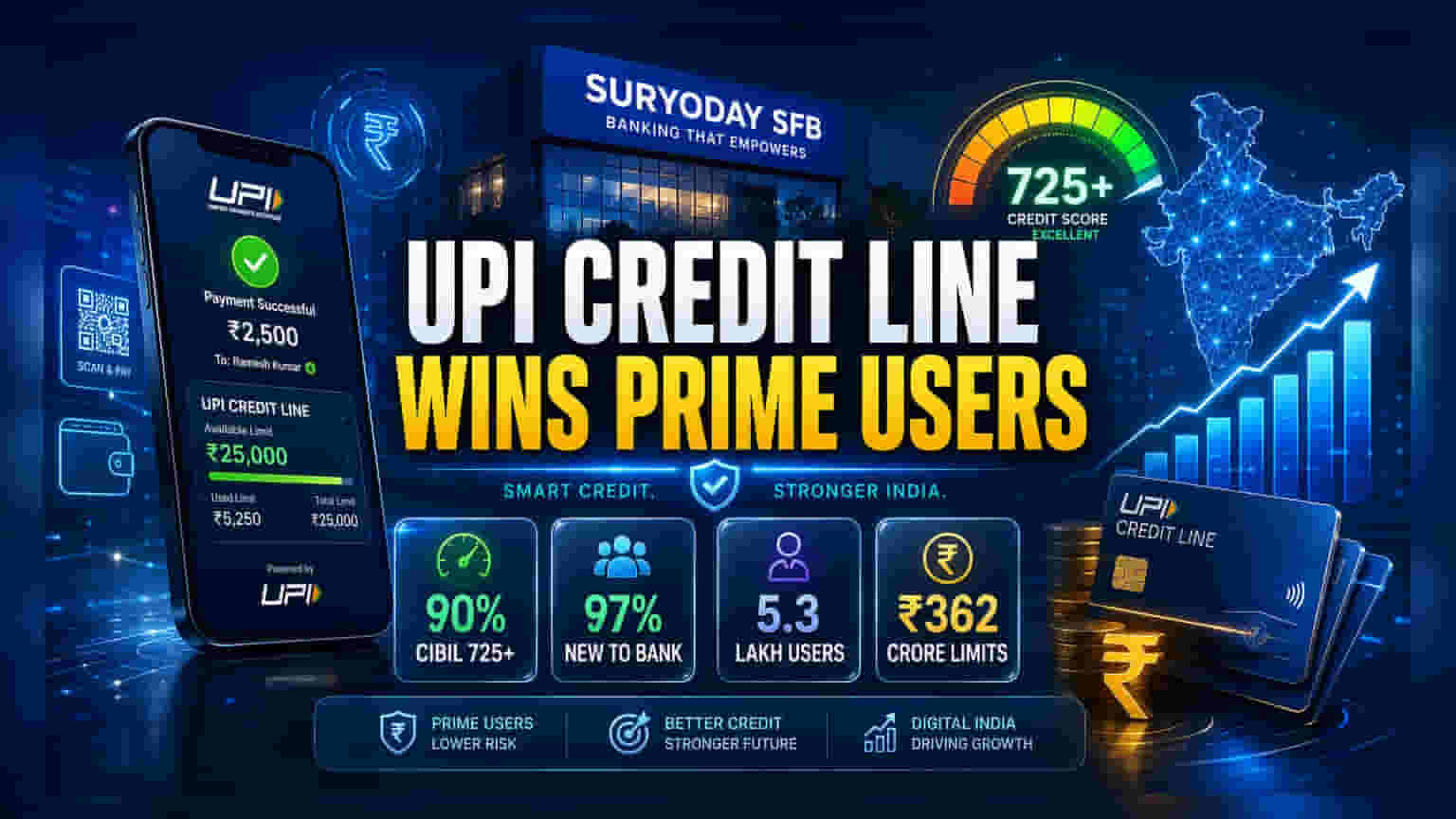

New data from Suryoday Small Finance Bank shows that 90% of its 'Credit Line on UPI' users have CIBIL scores above 725. This indicates that prime borrowers are using the service for convenience, helping the bank acquire new customers. Since launching in August 2025, the bank has sanctioned over ₹362 crore in credit lines, marking a significant step in its digital lending strategy.

What the Data Reveals

Suryoday Small Finance Bank has shared insights into the usage of its 'Credit Line on UPI' (CLOU) product, launched in August 2025. The data challenges the assumption that digital credit lines are mostly used by those with limited credit history. Instead, the bank reported that approximately 90% of its CLOU customers hold CIBIL scores exceeding 725. This suggests that the product is primarily attracting 'prime' borrowers—individuals with stable credit profiles—who value the convenience of digital credit for daily payments.

Why This Matters for the Bank

For a Small Finance Bank, which traditionally focuses on microfinance and semi-urban lending, acquiring prime customers is a significant shift. Typically, these banks face higher risks due to their reliance on micro-borrowers. By using digital products to attract customers with high credit scores, the bank is attempting to diversify its loan book and reduce risk exposure.

Additionally, the bank reported that over 97% of these CLOU users are 'new to bank' (NTB) customers. This indicates that the Credit Line on UPI serves as an efficient digital channel for acquiring new clients without the overhead costs of traditional branches. If this trend continues, it could lower the cost of customer acquisition for the bank over time.

Operational Progress

Since its launch, the bank has pre-qualified nearly 1.1 million customers and successfully sanctioned credit lines to 530,000 users. The total sanctioned limits stand at over ₹362 crore, with customers having utilized approximately ₹102 crore so far. The average drawdown amount per user is around ₹7,000, which aligns with the product's design for small, frequent payments rather than large-sum loans. Geographic adoption is strongest in regions with high digital payment penetration, particularly in North and West India, with Jaipur and Delhi-NCR emerging as top contributors.

How Investors May Read This

While the adoption metrics are promising, the utility of this product as a revenue driver depends on how the bank manages margins and asset quality. Currently, the overall utilization rate against the total sanctioned limit is around 28%. A higher utilization rate usually generates more interest income for the lender, but it also increases the risk of defaults if not managed carefully. Investors may monitor whether this digital lending segment becomes a meaningful contributor to the bank's net interest margin and whether it maintains low delinquency rates compared to the bank’s traditional microfinance portfolio. The reliance on digital channels like Paytm is also a monitorable, as the bank's success is tied to the platform's ability to maintain high user engagement.