Shriram Finance has raised interest rates on fixed deposits and investment plans by up to 25 basis points, effective July 2, 2026. The new rates apply to deposits of up to ₹10 crore, with longer-term tenures seeing the most significant increase. This change is relevant for investors seeking fixed-income returns from a highly-rated non-banking finance company.

What Happened

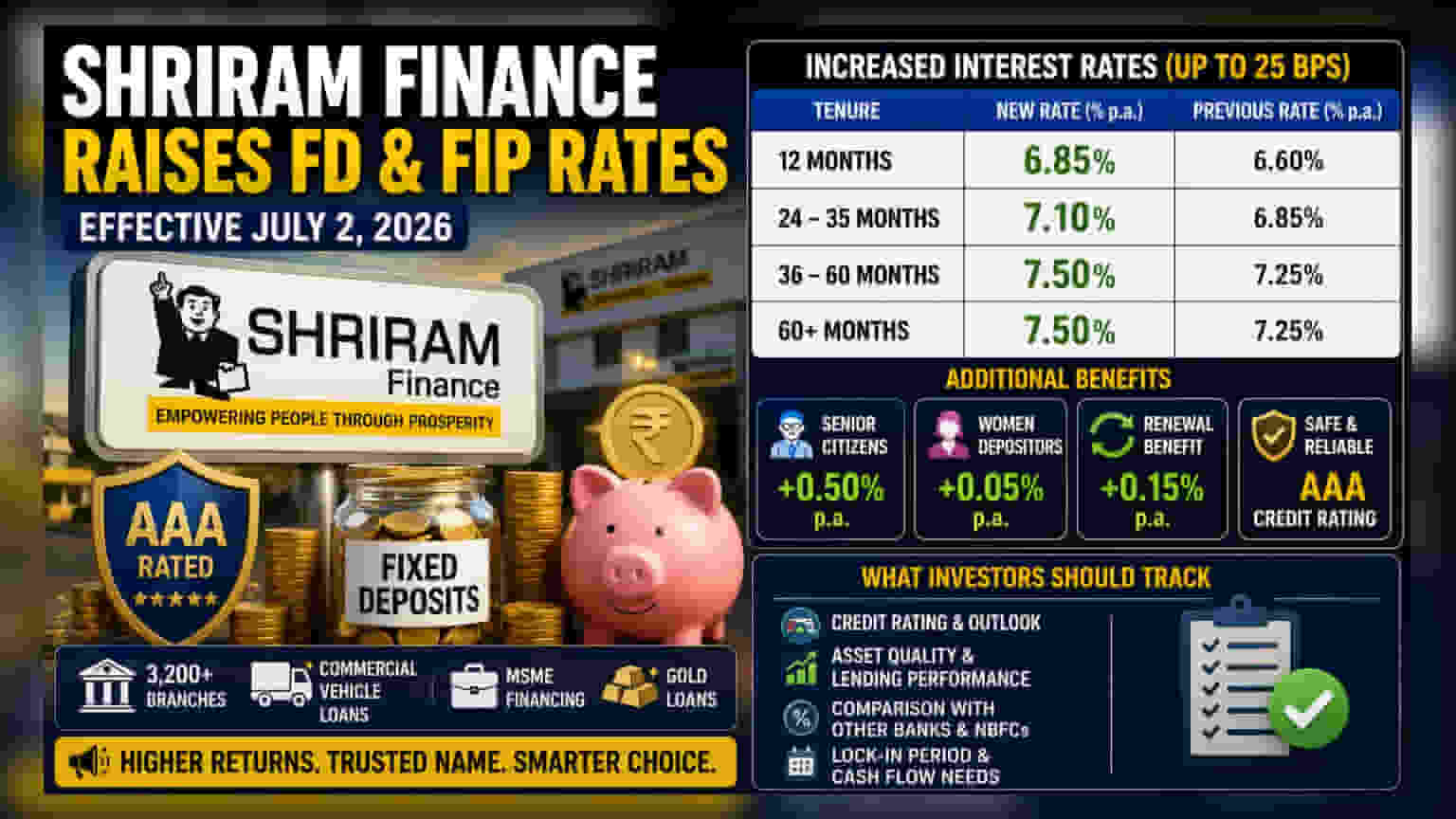

Shriram Finance has announced a revision in interest rates for its Fixed Deposit (FD) and Fixed Investment Plan (FIP) products. Effective July 2, 2026, the company is increasing interest rates by up to 25 basis points (0.25%) on selected tenures for deposits valued up to ₹10 crore.

The adjustments specifically target medium to long-term deposits. For instance, the annual interest rate for 36 to 60-month deposits has been increased to 7.50% from 7.25%. Other tenures, such as the 12-month deposit, will now offer 6.85%, while deposits maturing between 24 and 35 months will offer 7.10%.

Why Finance Companies Raise Rates

Non-banking financial companies (NBFCs) like Shriram Finance often adjust their deposit rates to manage their cost of funds and ensure they have enough liquidity to support their lending activities. By offering slightly higher interest rates, these companies aim to attract more retail deposits, which are often considered a stable and consistent source of funding compared to market-linked borrowings.

For investors, these hikes reflect the current competitive environment in the retail financial sector, where companies compete for savings to fund their loan books. Shriram Finance, which focuses on segments like commercial vehicle loans, MSME financing, and gold loans, requires a steady flow of capital to maintain its lending operations across its network of over 3,200 branches.

The Safety And Credit Rating Context

Shriram Finance currently holds a credit rating of "AAA/Stable" from major agencies, including CRISIL, ICRA, India Ratings, and CARE. In the financial world, a "AAA" rating is the highest grade, indicating the company has a very strong capacity to meet its financial commitments, such as paying interest and returning the principal amount to depositors.

However, it is important for investors to remember that an NBFC deposit is different from a bank deposit. While the credit rating is high, NBFC deposits are not covered by the Deposit Insurance and Credit Guarantee Corporation (DICGC), which provides insurance cover of up to ₹5 lakh for bank deposits. Investors typically choose highly-rated NBFC deposits for the extra yield over bank rates, provided they are comfortable with the company's credit profile.

Additional Benefits To Track

Beyond the base interest rates, the company continues to offer preferential benefits for specific groups. Senior citizens receive an additional 0.50% per annum, and women depositors are eligible for an extra 0.05% interest. Additionally, customers who choose to renew their matured deposits rather than withdrawing them can earn an extra 0.15% interest.

What Investors Should Track Next

When considering these deposits, investors should evaluate the lock-in period and their own cash flow needs. Since these rates are locked for the chosen tenure, it is useful to compare them with current interest rates offered by other large NBFCs and banks to see how they align with market standards. The most important monitorable for any fixed deposit investor remains the credit rating, which serves as a guide to the safety of the capital. Any change in the company’s credit outlook or its ability to manage its asset quality in its core lending sectors should also be monitored.