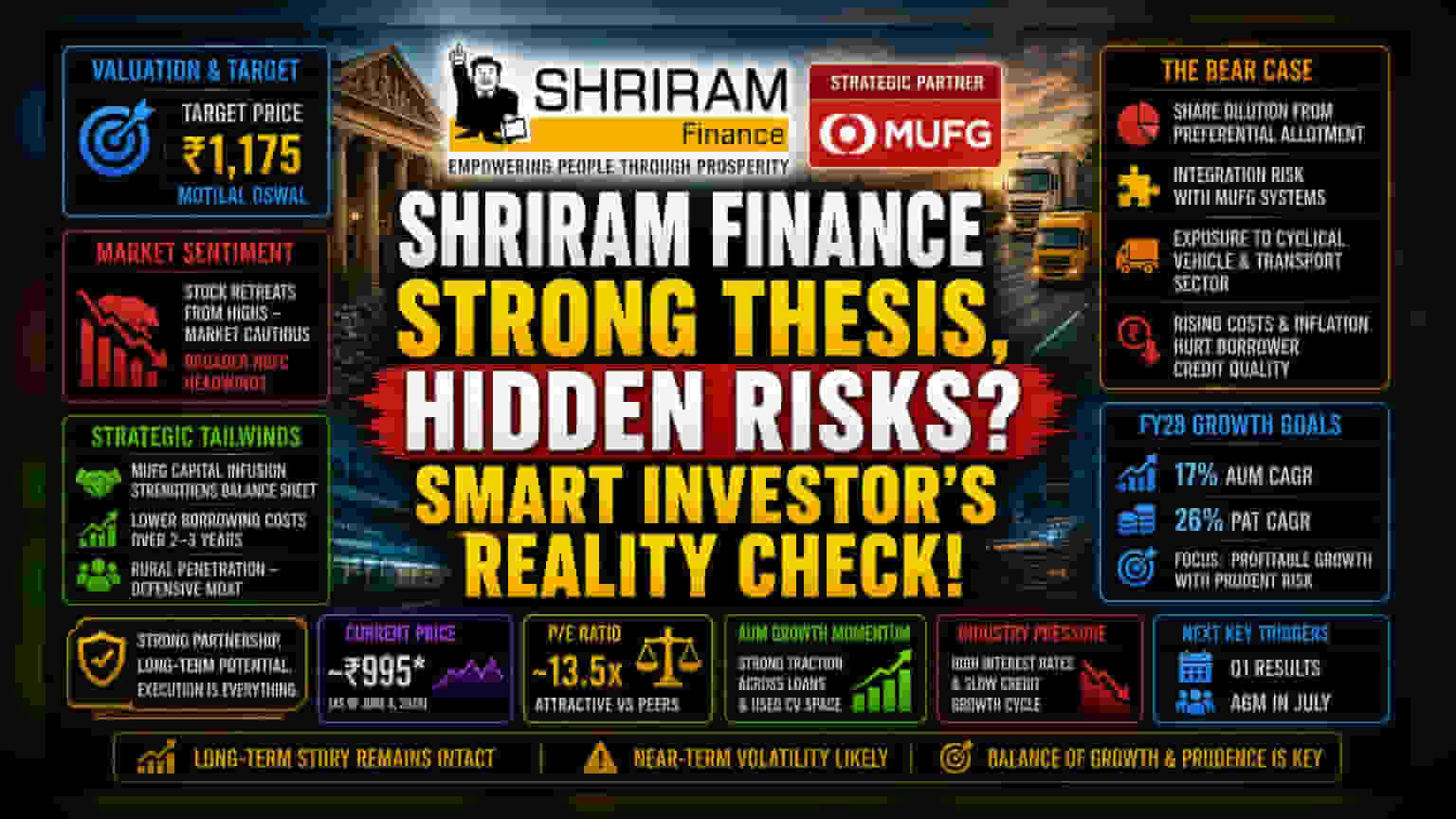

The Valuation Gap and Market Sentiment

Shriram Finance currently trades at a valuation that implies significant investor confidence in its structural transformation, yet the market is exhibiting signs of caution. Despite being assigned a target price of Rs 1,175 by Motilal Oswal, the stock has faced downward pressure, retreating from recent highs. This divergence is symptomatic of a broader trend: while brokerage sentiment remains structurally bullish based on the strategic partnership with MUFG, the immediate price action reflects a market wary of macroeconomic volatility and the cooling of the credit growth narrative across the non-banking financial sector.

Strategic Tailwinds vs. Operational Reality

Following the influx of primary equity capital from MUFG, Shriram Finance is repositioned with a strengthened balance sheet, anticipated to lower borrowing costs over the next two to three years. Management’s focus on leveraging this capital to accelerate Assets Under Management (AUM) growth remains the primary thesis for institutional support. However, the path to achieving a 17% AUM CAGR and 26% Profit After Tax (PAT) CAGR through FY28 is not without hurdles. While rural penetration remains a defensive moat, the NBFC’s reliance on vehicle financing leaves it exposed to cyclical downturns in the transport sector. Furthermore, as the company scales, maintaining cost efficiency in a high-interest-rate environment will be essential to protecting margins that have faced consistent pressure across the industry.

The Forensic Bear Case

From a risk-averse vantage point, the exuberance surrounding the MUFG integration obscures several structural vulnerabilities. First, the preferential allotment of shares has fundamentally altered the equity base, introducing dilution concerns for existing shareholders that are often overlooked in standard growth models. Second, integration risk remains a significant, yet under-discussed, variable. Merging the operational workflows of a massive, decentralized, rural-focused Indian NBFC with the global risk-management frameworks of a major international bank is a multi-year project prone to friction. Finally, the NBFC sector is contending with rising fuel costs and inflationary pressures that directly impact the creditworthiness of its primary borrower base—truckers and small fleet operators. Unlike more diversified peers, Shriram’s concentration in vehicle lending acts as a double-edged sword; should the cyclical recovery in commercial vehicle demand falter, the company’s asset quality metrics may see deterioration not fully captured by current earnings models.

Future Outlook

Looking forward, the brokerage consensus remains heavily tilted toward a 'Buy,' with a mean target price hovering above Rs 1,140. Investors are closely monitoring the upcoming quarterly results and the Annual General Meeting in July for cues on whether the firm can successfully execute its deleveraging strategy and sustain NIMs. While the long-term thesis anchored by the MUFG partnership is compelling, the stock’s near-term performance will likely remain tethered to its ability to navigate the precarious balance of rising operational costs and the need for prudent, non-aggressive credit expansion.