Banks are offering up to 8.05% on 5-year fixed deposits for senior citizens, with Small Finance Banks leading the yield charts. While higher rates look attractive, investors must balance the extra return against the safety profiles of different lenders and the Rs 5 lakh DICGC insurance limit.

The 5-Year FD Landscape

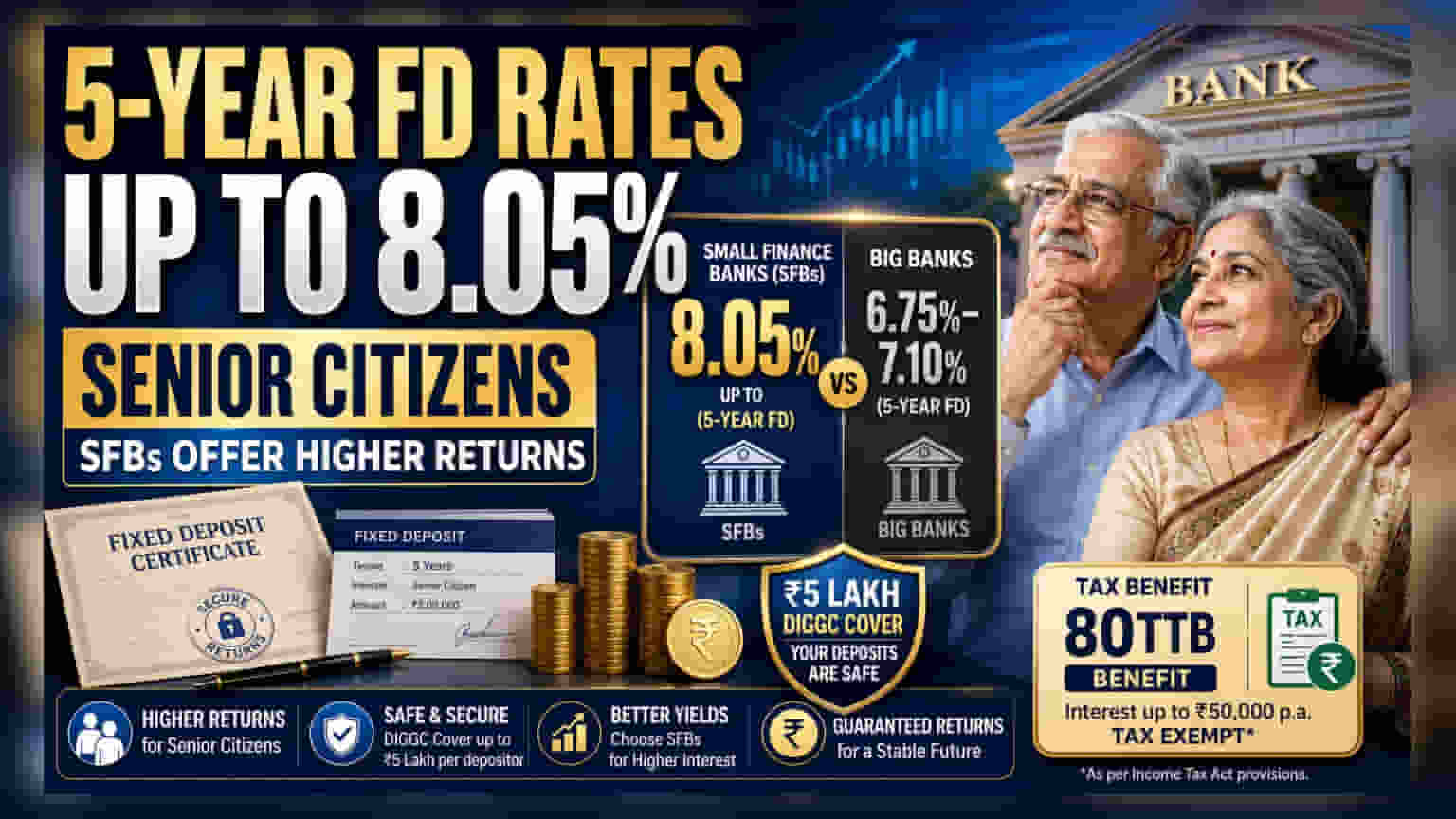

Senior citizens looking for steady income are finding that 5-year fixed deposits (FDs) from Small Finance Banks (SFBs) currently offer the highest returns, reaching up to 8.05%. In contrast, major public and private sector banks are providing rates typically ranging between 6.75% and 7.10% for the same tenure. For example, Suryoday Small Finance Bank and Jana Small Finance Bank are among those offering the 8.05% mark. Meanwhile, larger institutions like State Bank of India (SBI) offer around 7.05%, while private lenders like ICICI Bank provide 7.10% and HDFC Bank offers 6.90% for senior citizens.

Why Rates Differ Across Banks

The gap in interest rates is primarily driven by the business models of these lenders. Large banks benefit from a massive, low-cost deposit base and higher systemic trust, allowing them to attract capital without offering the highest market rates. Small Finance Banks, however, often need to offer higher yields to attract depositors and fund their loan books, which are usually focused on under-served segments. Investors should view the extra interest as a premium for accepting the risk profile of a smaller, potentially more volatile institution compared to a large, established bank.

Safety and the DICGC Limit

When chasing higher yields, safety is a key factor. All bank deposits in India are insured by the Deposit Insurance and Credit Guarantee Corporation (DICGC). This insurance covers a maximum of Rs 5 lakh per depositor, per bank, which includes both principal and interest. If an investor puts a large amount in a single Small Finance Bank that exceeds this Rs 5 lakh threshold, the excess amount is not backed by this government-guaranteed protection. For seniors with larger investable corpuses, diversifying across multiple banks or sticking to larger institutions is often a strategy to manage this specific risk.

Tax Considerations for Seniors

Interest income from fixed deposits is fully taxable at the investor's applicable income tax slab. However, under Section 80TTB of the Income Tax Act, senior citizens can claim a deduction of up to Rs 50,000 in a financial year on interest earned from bank FDs. This deduction can help improve the post-tax return. Investors should calculate their post-tax yield rather than looking only at the headline interest rate to understand the actual benefit.

What Investors Should Track

Beyond the interest rate, investors should pay attention to the penalty structure for premature withdrawal. Many banks charge a fee if the deposit is broken before the 5-year maturity, which can eat into the returns. Additionally, investors should monitor the interest rate cycle; if central bank rates remain stable or decrease, locking in a 5-year deposit at current levels might be a strategic move to secure income for the long term. Conversely, if inflation rises and rates climb, long-term locked deposits might eventually yield less than newer market offerings.