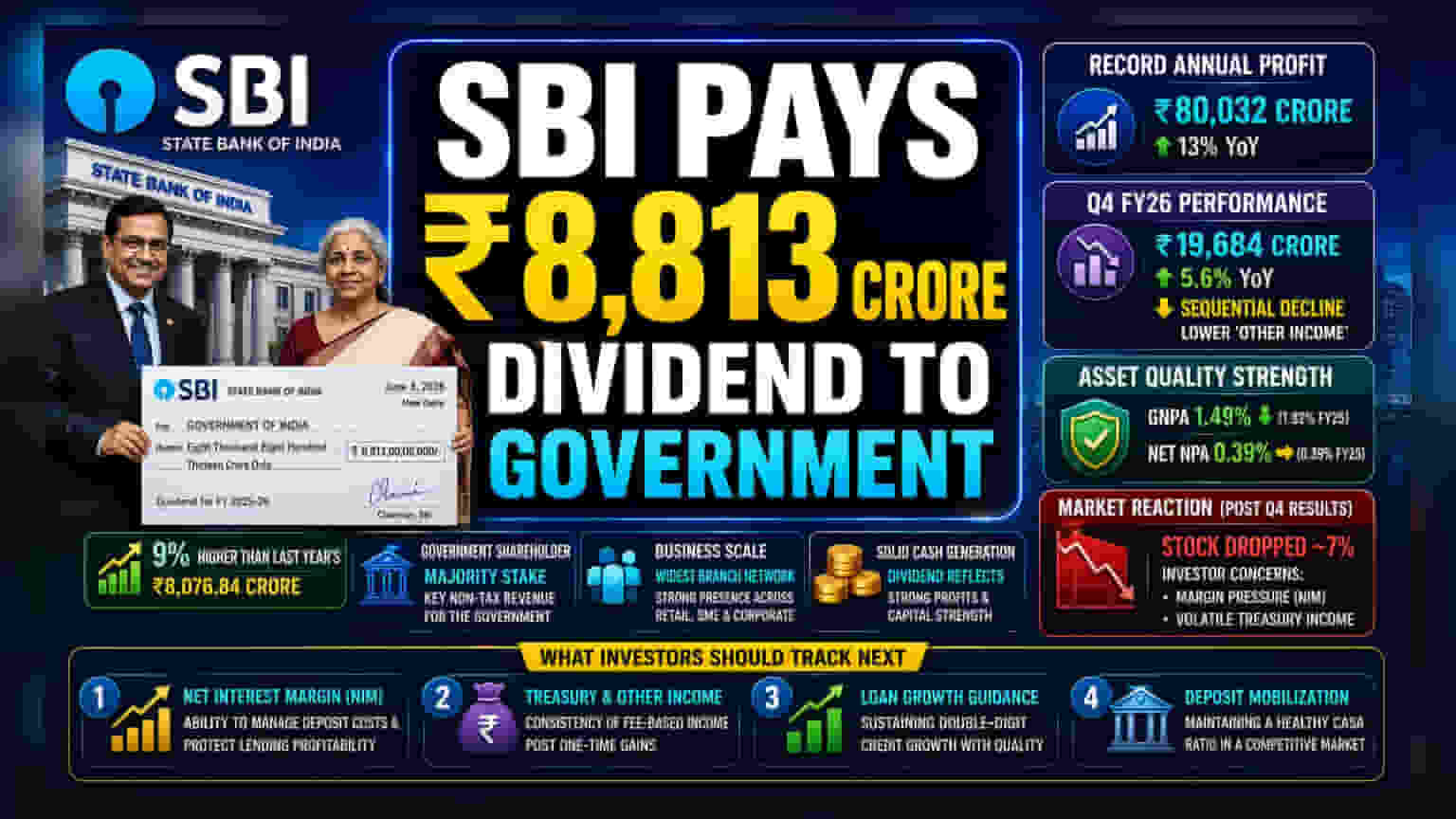

What Happened

State Bank of India (SBI), the country's largest public sector lender, has presented a dividend cheque of Rs 8,813 crore to the Indian government for the financial year 2025-26. The cheque was handed over by the bank's Chairman to the Union Finance Minister in New Delhi. This payout is a 9% increase compared to the Rs 8,076.84 crore dividend paid in the previous fiscal year. As the majority shareholder, the government receives this dividend as part of its non-tax revenue collection.

Strong Annual Performance vs. Quarterly Challenges

The dividend payout is supported by the bank's record-breaking performance for the full 2025-26 fiscal year. SBI reported a standalone net profit of Rs 80,032 crore, marking a roughly 13% increase from the previous year. This annual profit milestone underscores the bank's scale and operational reach across the country.

However, the picture is more nuanced when looking at the recent fourth-quarter results. For the quarter ending March 2026, the bank reported a net profit of Rs 19,684 crore. While this was a 5.6% increase compared to the same quarter last year, it reflected a sequential decline from the third quarter. The bank also faced pressure on operating profit, which was impacted by a drop in 'other income.' Investors should note that a significant portion of this income volatility in the past year was tied to exceptional gains from the sale of stake in subsidiaries, such as Yes Bank, which were present in the previous year's figures but not repeated.

Asset Quality Remains a Key Strength

One of the most stable aspects of SBI's recent performance is the continued improvement in asset quality. The bank’s Gross Non-Performing Asset (GNPA) ratio improved to 1.49% for FY26, down from 1.82% in the previous year. Similarly, Net NPA levels remained stable at 0.39%. This improvement in loan quality is a positive signal for the bank's risk management, especially as it continues to expand its loan book across retail, SME, and corporate sectors.

How Investors May Read This

Market participants have been closely watching the bank's ability to maintain margins in a high-interest-rate environment. When the Q4 results were announced in May 2026, the stock saw a notable reaction, dropping approximately 7% on the trading day following the announcement. This reaction reflected investor concerns regarding margin pressure (Net Interest Margin or NIM) and the volatility in treasury income rather than the bank's fundamental asset quality.

For investors, the dividend payment confirms the bank's solid cash-generating ability and capital strength. With a Capital Adequacy Ratio of 15.40%, the bank maintains a healthy buffer to support future lending growth.

What Investors Should Track Next

The focus for the coming quarters will shift toward the bank's ability to protect its margins against rising deposit costs. As the industry faces a tighter liquidity cycle, investors may track:

- Net Interest Margin (NIM) stability: Whether the bank can manage the cost of deposits without sacrificing its core lending profitability.

- Treasury and Other Income: Monitoring the consistency of fee-based income now that the impact of large one-time gains from divestments has faded.

- Loan Growth Guidance: Tracking whether the bank can maintain its double-digit credit growth as it continues to prioritize quality lending.

- Deposit Mobilization: How the bank balances its CASA (Current Account Savings Account) ratio in a competitive deposit market.