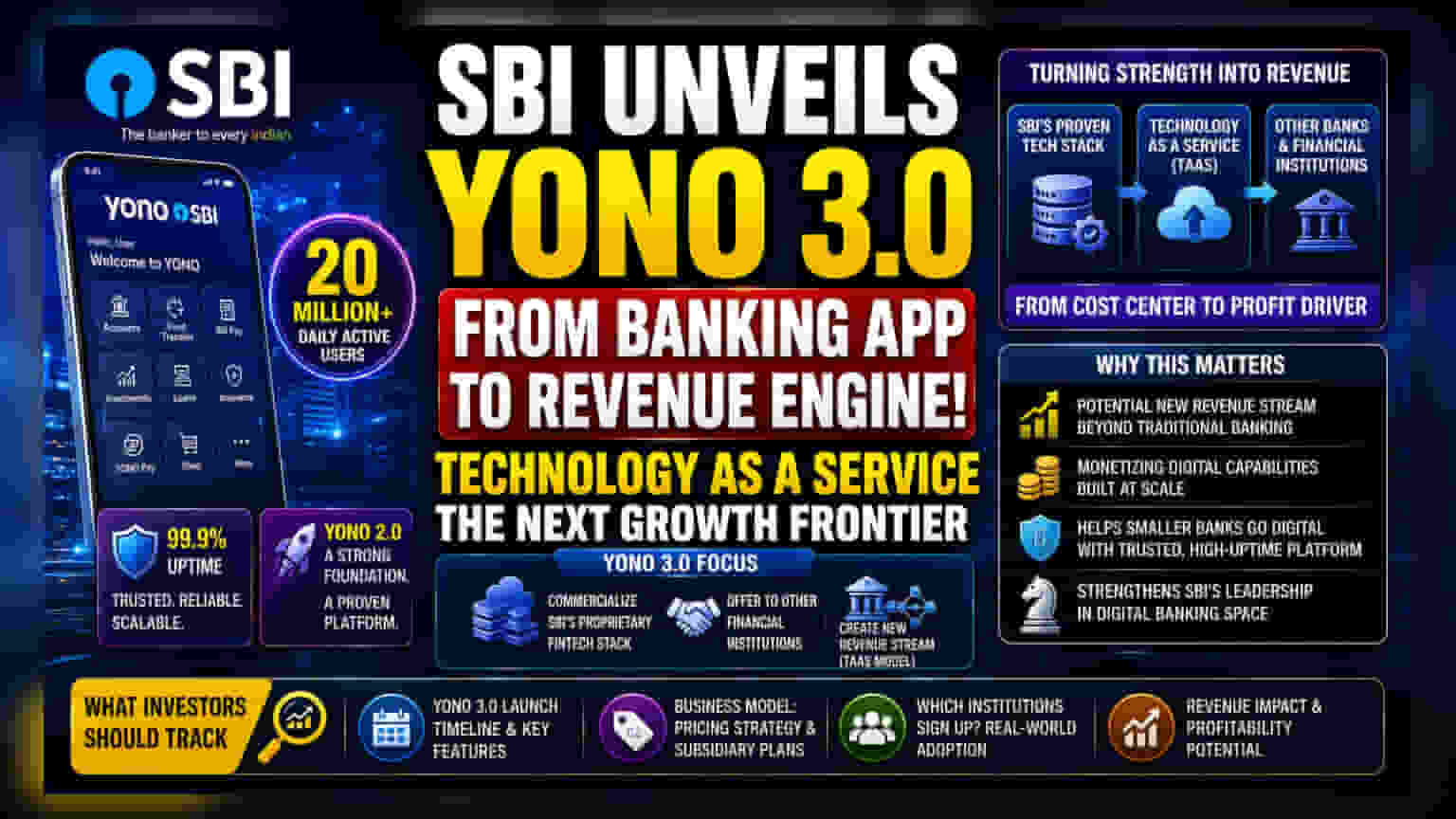

What Happened

State Bank of India (SBI) has announced plans for the next iteration of its digital banking platform, YONO 3.0. Building on the success of YONO 2.0—which features a fully rebuilt interface and currently serves approximately 20 million daily active users—the bank is shifting its strategy. Chairman C S Setty stated that the upcoming version will focus on commercializing the platform's technology. This involves offering SBI's proprietary fintech stack to other financial institutions, effectively turning the bank's internal digital capability into an external service.

Why This Matters For Investors

The move suggests a shift in SBI's digital strategy. Until now, YONO functioned as a tool to improve customer experience and reduce service costs by moving transactions from physical branches to a digital interface. By potentially selling this technology to other banks, SBI could create a new revenue stream. For shareholders, this represents a transition from treating the app as a pure cost center—focused on maintenance and customer support—to a potential revenue-generating asset, often referred to as 'Technology as a Service' (TaaS).

The Business Logic and Competition

India's digital banking sector is highly competitive, with large private players like HDFC Bank and ICICI Bank continuously upgrading their own mobile applications to improve engagement. SBI's decision to offer its tech to others implies confidence in the platform's stability, citing its 99.9% uptime. However, the success of this business model will depend on who the potential customers are. While smaller banks may lack the resources to build robust, high-uptime digital platforms and might welcome such solutions, they must also weigh the risk of relying on technology owned by a direct, much larger competitor. Trust, data security, and platform neutrality will be critical factors if SBI intends to secure third-party clients.

Operational and Execution Risks

While the plan to commercialize technology is ambitious, it brings new challenges. Selling software to other banks is a different business model from running a consumer-facing app. It requires building a dedicated support structure, managing external client expectations, and ensuring the platform can scale for diverse banking environments beyond SBI’s own internal needs. Any technical glitch in a platform used by multiple banks would carry higher reputational and regulatory risks than a platform used only internally.

What Investors Should Track

Investors will likely watch several key areas as this strategy develops. First, the timeline for the launch and the specific features of YONO 3.0 will be important to monitor. Second, any commentary regarding the business model—specifically, how the bank plans to price these services and whether it will create a separate subsidiary to handle this technology business—will provide clarity on potential profitability. Finally, market participants will track whether any smaller financial institutions actually sign up to use the platform, as this will prove the real-world demand for SBI's tech stack outside of its own ecosystem.