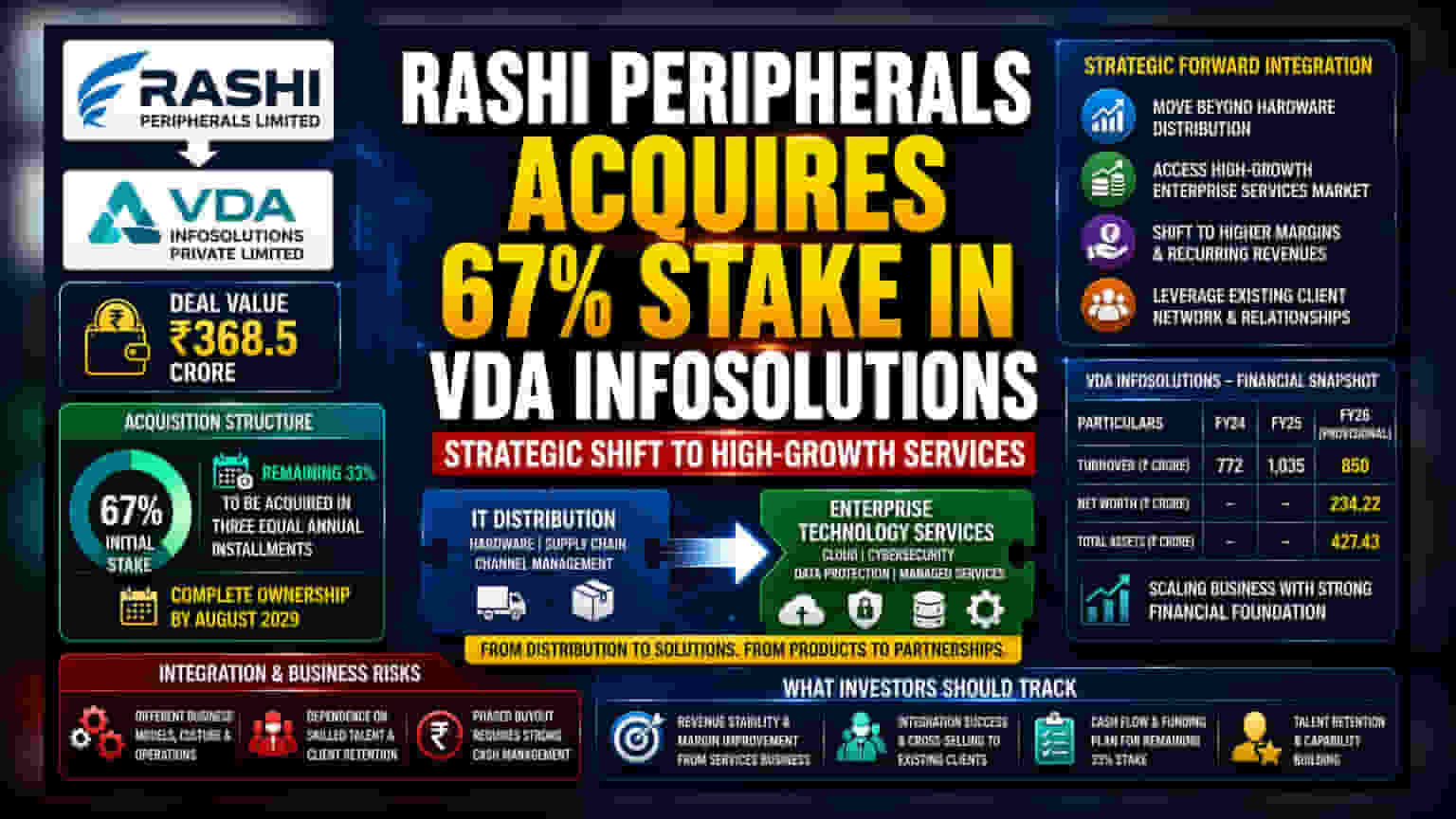

Rashi Peripherals has announced the acquisition of a 67% equity stake in VDA Infosolutions for ₹368.5 crore in cash. The company plans to acquire the remaining 33% in three annual tranches, finalizing full ownership by August 2029. This acquisition marks a strategic shift to integrate cloud and enterprise technology services into its core IT distribution business.

What Happened

Rashi Peripherals Ltd. has announced a definitive agreement to acquire a 67% controlling stake in VDA Infosolutions Private Ltd. for a cash consideration of ₹368.5 crore. The transaction, described as a strategic forward integration, will see VDA Infosolutions become a subsidiary of the company. The acquisition structure is phased, with the remaining 33% equity to be bought in three equal annual installments, aiming for complete ownership by August 2029.

Strategic Shift To Services

Rashi Peripherals is primarily known for its IT distribution business, where it manages the supply chain for various technology brands. By acquiring VDA Infosolutions, the company is attempting to move beyond hardware distribution and enter the high-growth enterprise technology sector. VDA Infosolutions offers specialized services, including cloud technology, cybersecurity, data protection, and infrastructure management. For investors, this represents a transition from a pure-play trading and distribution model, which typically operates on thin profit margins, toward a services-led model that often commands better margins and recurring revenue streams.

The Financials And The Growth Trend

VDA Infosolutions brings an established operational history, having been founded in 2010. Its financial data indicates a scaling business but with some variability. The company reported a turnover of ₹772 crore in FY24, which grew to ₹1,035 crore in FY25. However, provisional financials for FY26 show a turnover of ₹850 crore. Investors should note this fluctuation in revenue, which could be due to project-based income or specific market conditions. The company reported a net worth of ₹234.22 crore and total assets of ₹427.43 crore in its FY26 provisional report.

Integration And Business Risks

While the expansion into services is strategically sound, it comes with integration challenges. The distribution business and the enterprise services business operate under different models. The distribution business relies heavily on inventory turnover and channel management, whereas the services business depends on skilled talent, long-term client contracts, and technical delivery capabilities. Managing this cultural and operational shift will be a key task for the management. Furthermore, the phased acquisition over the next three years implies that the company must maintain a strong cash position to fund the remaining 33% stake purchase, which could impact free cash flow depending on the company’s capital allocation priorities.

What Investors Should Track

Investors may monitor how effectively the company integrates these new service offerings into its existing client base. The key monitorable will be whether the management can stabilize the revenue volatility seen between FY25 and FY26 and whether the services business begins to contribute meaningfully to profit margins in the coming quarters. Other factors to watch include the company’s ability to manage its cash reserves while funding the phased buyout of the remaining equity by 2029 and whether the services division can retain key technical talent.