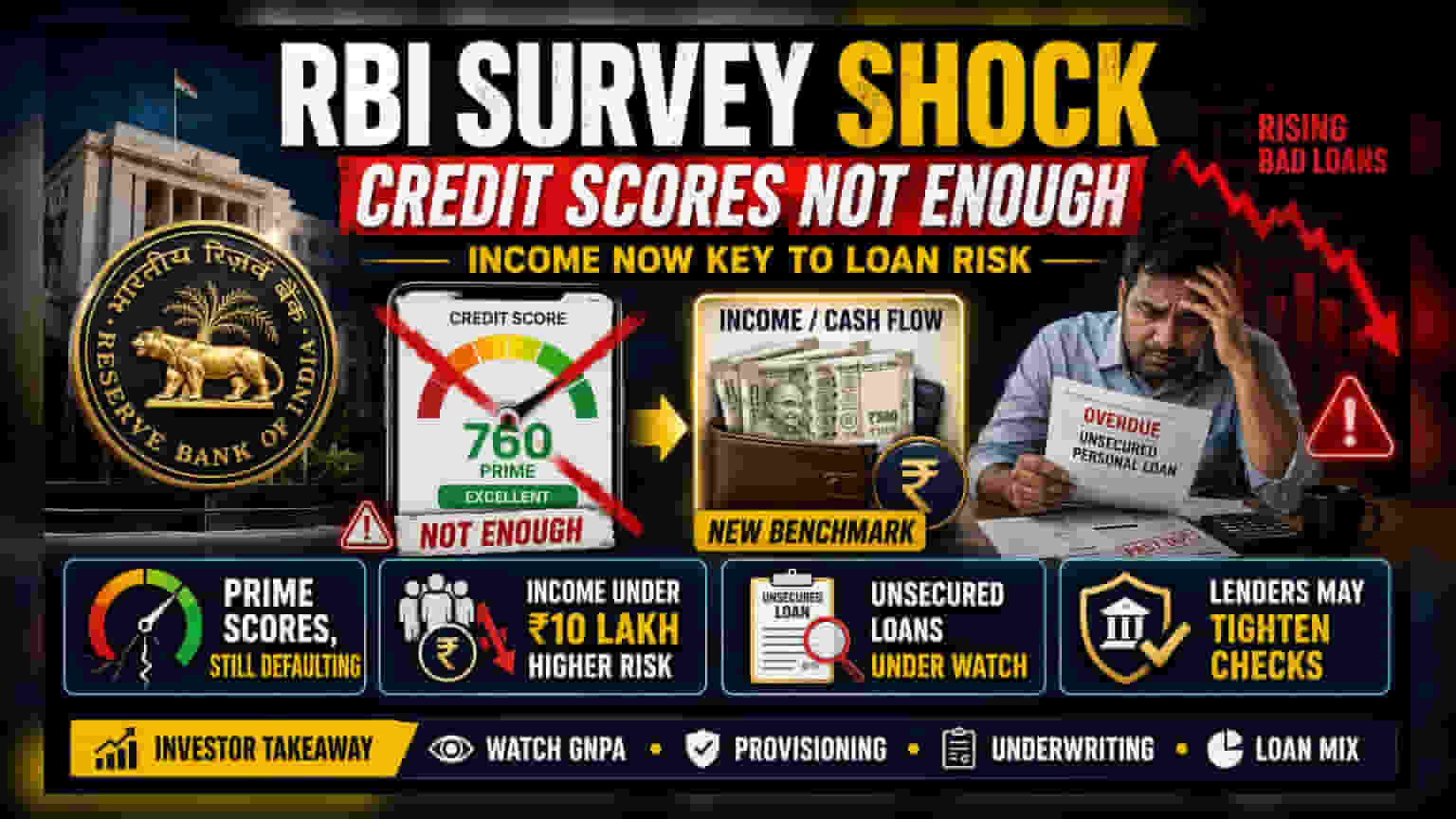

A new RBI survey reveals that high credit scores do not guarantee loan repayment, especially for unsecured personal loans. Borrowers earning up to ₹10 lakh are contributing significantly to defaults despite holding 'prime' credit scores. This suggests that income, rather than just past credit history, is a more accurate measure of financial stability, which may prompt lenders to rethink their risk assessment models.

What Happened

The Reserve Bank of India (RBI) has released findings suggesting that credit scores—long considered the gold standard for assessing a borrower's reliability—are not always a perfect predictor of loan repayment. The survey focused on the rapidly growing segment of unsecured personal loans. It found that a significant number of borrowers, specifically those earning up to ₹10 lakh annually, are contributing to a rise in bad loans.

Crucially, many of these individuals held 'prime' or 'prime-plus' credit scores, which are traditionally interpreted by banks and lenders as signs of a low-risk borrower. The findings indicate a gap between historical credit behavior and actual current financial ability to repay debt.

Why Income Is Becoming The New Benchmark

While a credit score tracks how someone has repaid debts in the past, it does not necessarily capture a borrower's current ability to handle new monthly payments. The RBI survey highlights that for the segment of borrowers earning under ₹10 lakh, income levels are a more reliable indicator of repayment capacity.

This is particularly relevant for unsecured loans—credit products given without any collateral like property or gold. Because these loans depend solely on the borrower’s promise to pay, lenders often relied heavily on credit scores for approval. However, the data shows that when financial pressure hits, a person's current income becomes the ultimate buffer against default, regardless of their past credit history.

Implications For Indian Lenders

This shift in perspective by the regulator is likely to force banks and Non-Banking Financial Companies (NBFCs) to re-evaluate their lending strategies. If credit scores alone are failing to capture the full risk, lenders may have to move toward stricter income verification and cash-flow analysis before approving personal loans.

Recent data from the RBI’s Financial Stability Report also reflects growing concerns regarding small-ticket unsecured loans, particularly in the fintech space. Lenders may now need to balance the need for rapid digital loan growth with the reality that 'prime' credit scores do not make a loan risk-free. This could lead to more conservative lending practices or higher interest rates for certain borrower profiles as banks adjust their risk models to avoid a spike in bad loans.

What Investors Should Track

Investors in banking and financial stocks should watch how companies manage their retail loan books. Key indicators to monitor include:

- Asset Quality Trends: Keep an eye on Gross Non-Performing Asset (GNPA) ratios, specifically in the personal loan segment.

- Provisioning: Observe if banks increase their loan-loss provisions (money set aside for potential bad loans) for personal credit.

- Management Commentary: Listen to earnings calls for updates on how credit underwriting models are being tightened to account for income-based risk.

- Loan Growth Mix: Check if there is a pivot toward more secured lending or if the bank remains aggressive in the unsecured retail segment.