The Reserve Bank of India’s latest Financial Stability Report confirms that Indian banks can withstand economic stress, with capital levels staying above regulatory minimums through 2028. However, the report signals caution for non-banking financial companies (NBFCs), noting that 15 of them could fall below the mandatory capital threshold under severe economic conditions.

What Happened

The Reserve Bank of India (RBI) has released its bi-annual Financial Stability Report, providing a stress test for the health of India's banking and non-banking financial sectors. The report evaluates how these institutions would hold up if the economy faces shocks like high energy prices, geopolitical instability, or currency pressure. While the banking sector appears well-prepared, the report highlights clear signs of stress for the NBFC segment, with some companies potentially struggling to meet safety requirements if the economic environment worsens significantly.

Banks: The Capital Buffer

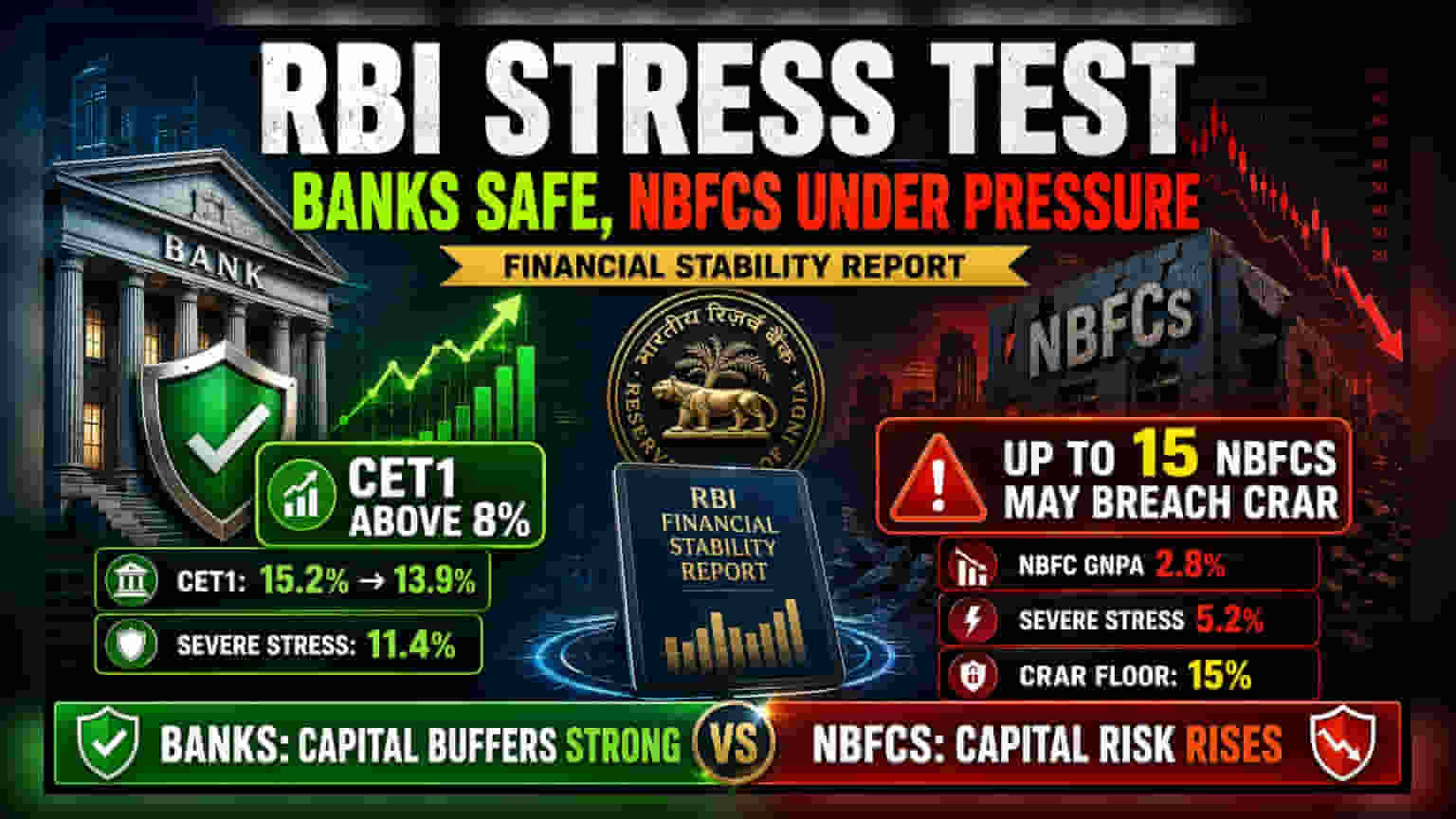

For investors, the core takeaway is the strength of the capital buffers in banks. The RBI analyzed 46 major banks and concluded that even under an adverse economic scenario, their Common Equity Tier 1 (CET1) capital—which is essentially the core money kept aside to absorb losses—would remain above the 8% regulatory requirement.

Under a baseline outlook, the aggregate CET1 capital ratio is expected to move from 15.2% in March 2026 to 13.9% by March 2028. In a severe stress scenario, this figure could dip further to 11.4%. While this reflects a drop, it remains safely above the mandatory floor, suggesting that major banks have enough financial muscle to handle tough times without a crisis. The report also noted that while bad loans, or Gross Non-Performing Assets (GNPA), might rise from 1.8% to 1.9% in the baseline, they could climb to 4.1% if conditions become severe.

The NBFC Stress Point

The findings for non-banking financial companies are more concerning. The RBI analyzed 174 NBFCs and found that their capital position is more sensitive to stress. Under the baseline scenario, their GNPA ratio is projected to rise to 2.8% by March 2027. If the economic climate turns hostile, this could jump to 5.2%.

Most importantly, the report warns that up to 15 NBFCs could breach the mandatory 15% Capital to Risk-weighted Assets Ratio (CRAR) under severe stress scenarios. This is a crucial metric, as it indicates the amount of capital an NBFC has relative to its loans. A breach here means the company may not have enough buffer to cover potential defaults, which could force them to raise more capital or limit their lending ability.

Why This Matters For Investors

This report creates a clear distinction between the two types of lenders. Banks operate under stricter regulations and generally have a more stable deposit base, which helps them survive downturns. NBFCs often rely on wholesale funding, which can be more expensive and harder to secure during economic stress.

When the RBI flags potential capital breaches for 15 NBFCs, it highlights a risk for shareholders in that sub-sector. If these companies are forced to raise fresh capital to stay compliant, it could lead to share dilution. Alternatively, they might have to slow down their loan growth, which would directly hurt their revenue and profit targets. For banks, the data suggests overall stability, which supports investor confidence, even if profitability remains sensitive to economic cycles.

What Investors Should Monitor

The most important monitorable for the next few quarters is how banks and NBFCs manage their asset quality. Investors may watch for any uptick in the percentage of bad loans in upcoming quarterly results, as this is often the first sign of financial strain. For NBFC stocks specifically, keeping an eye on their capital adequacy ratios (CRAR) and liquidity coverage levels in company disclosures will be vital to see if they are maintaining the safety buffers required by the regulator.