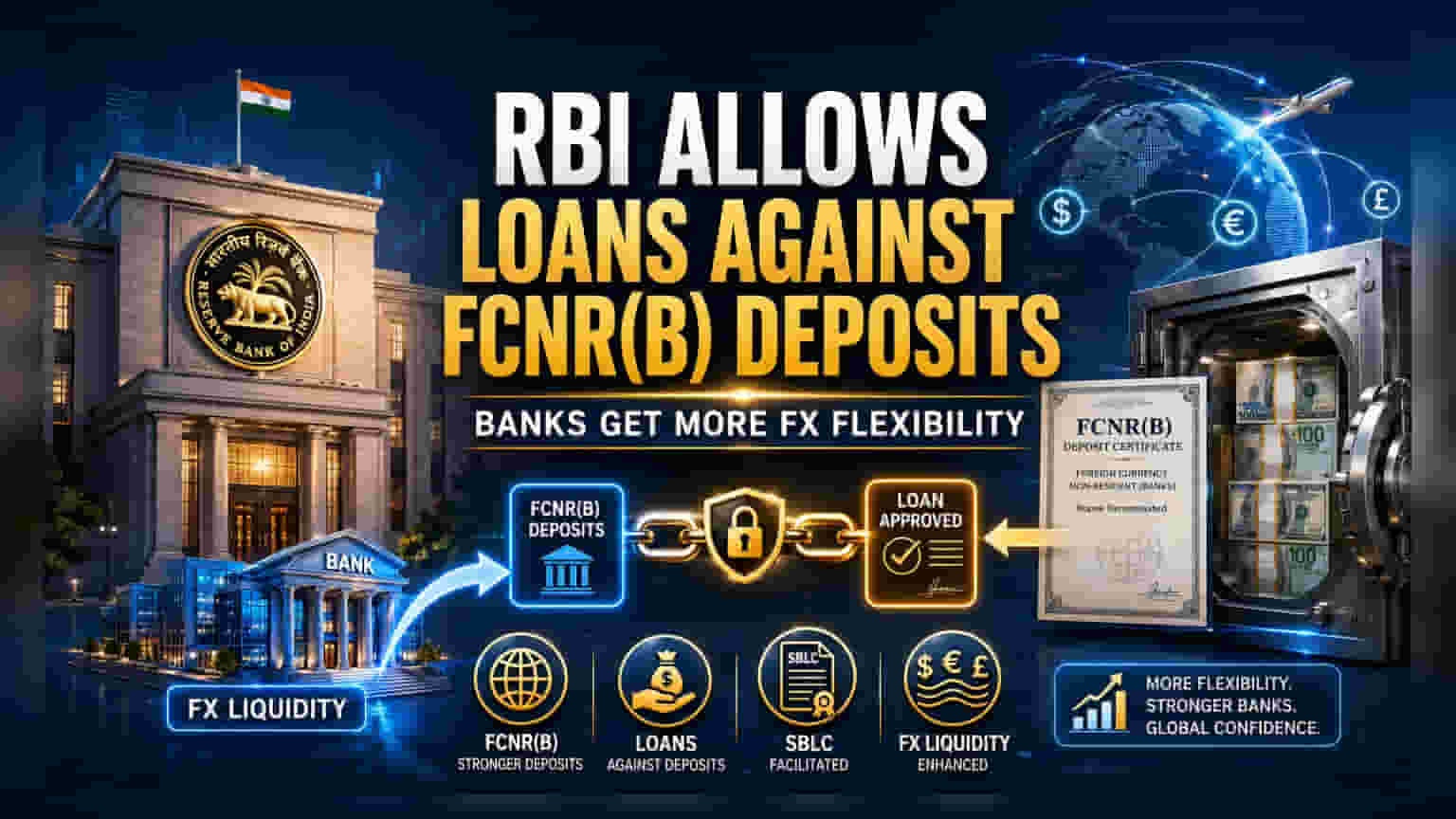

The Reserve Bank of India has updated its guidelines to allow banks to extend loans and issue credit guarantees against FCNR(B) deposits. This policy change is designed to attract greater foreign currency inflows by making these deposits more flexible for non-resident investors and cost-effective for banks through a new swap facility.

What Happened

The Reserve Bank of India (RBI) has introduced a new framework allowing banks to offer loans and issue Standby Letters of Credit (SBLC) against Foreign Currency Non-Resident (FCNR(B)) deposits. By allowing banks to place a 'lien' on these deposits, the regulator has effectively turned these long-term foreign currency accounts into usable collateral for borrowers. This change applies to both domestic and overseas branches of Indian banks, enabling them to provide credit facilities to non-resident account holders without requiring the prior liquidation of the deposit.

Why This Matters For Banks

For financial institutions, this update addresses a core challenge: liquidity management. By permitting loans against these deposits, banks can attract larger FCNR(B) inflows from non-resident Indians who might otherwise be hesitant to lock away their capital. This creates a dual benefit; it boosts the bank's foreign currency resources while simultaneously expanding their credit product offerings. The ability to use these deposits as security for SBLCs also allows banks to support their corporate clients' overseas financing needs more effectively.

The Role Of The Swap Facility

A significant part of this announcement is the concessional swap facility introduced by the RBI on June 5. The central bank is allowing banks to swap fresh three- to five-year FCNR(B) deposits with the regulator at a rate that neutralizes the cost of hedging. Hedging is the process banks use to protect themselves against currency fluctuations. By absorbing this cost, the RBI is making it cheaper for banks to mobilize and hold foreign currency deposits, thereby incentivizing them to aggressively pursue this funding avenue until the September 2026 deadline.

How It Changes The Deposit Landscape

Previously, FCNR(B) deposits were often viewed as static assets. The new flexibility brings them closer to standard domestic fixed deposits in terms of utility, yet with the added advantage of being held in foreign currency. The alignment with the External Commercial Borrowing (ECB) framework further streamlines the process, as banks can now match the swap tenor with the repayment schedules of their loans. This synchronization helps banks manage their balance sheets more efficiently while minimizing the risk of currency mismatches.

What Investors Should Track

Investors and market participants should monitor how quickly banks integrate these new lending capabilities into their product suites. The primary monitorable will be the growth in FCNR(B) deposit mobilization reported by major banks in upcoming quarterly results. Additionally, analysts will look for commentary on whether this initiative leads to a noticeable improvement in the foreign currency liquidity position of lenders, which could influence their ability to fund cross-border activities or manage their own hedging costs more efficiently. The success of this move will depend on how effectively banks market these flexible deposit products to the non-resident Indian community.