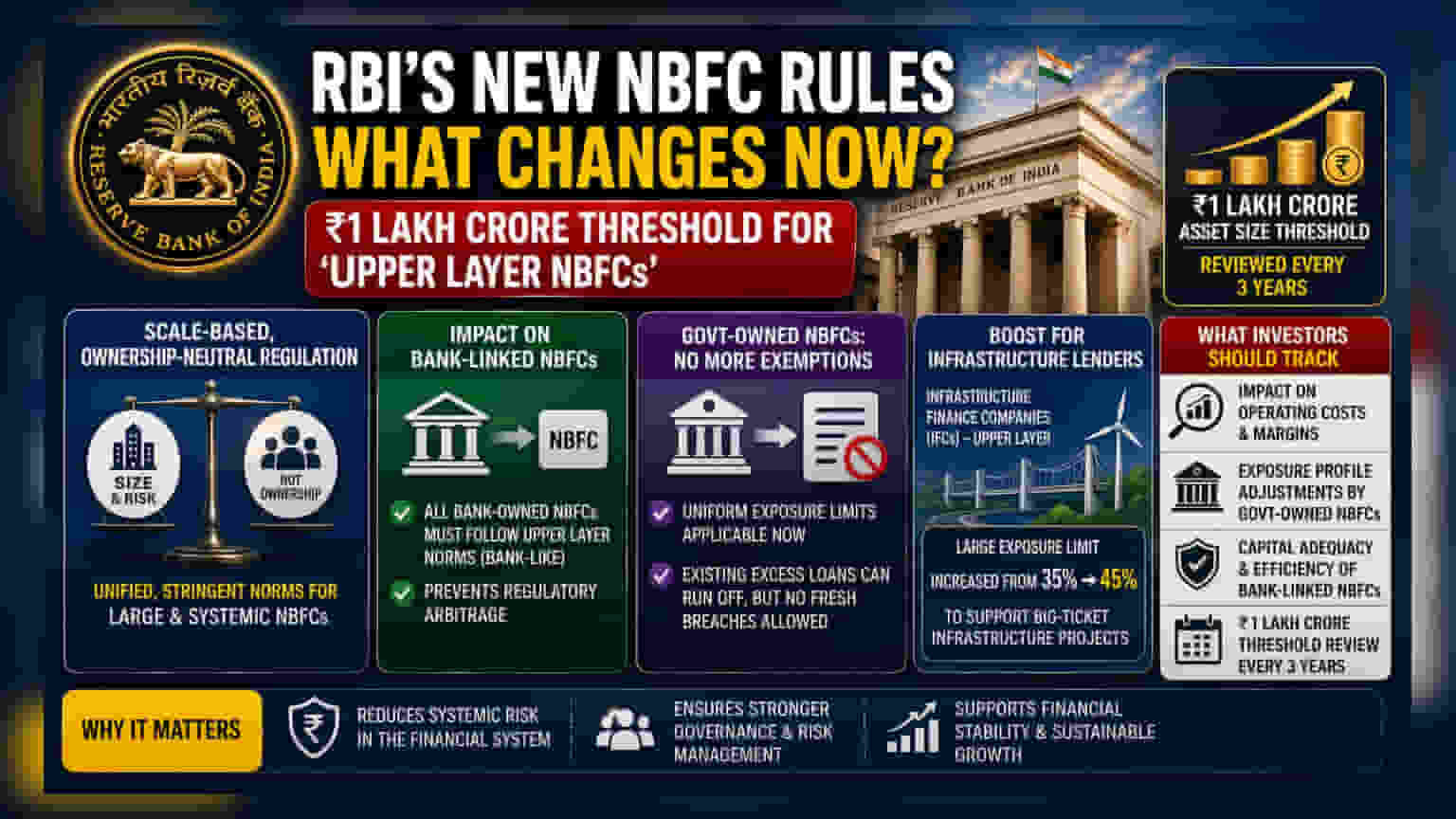

The Reserve Bank of India has announced a final scale-based regulatory framework for Non-Banking Financial Companies (NBFCs). Key changes include a fixed ₹1 lakh crore asset threshold for 'Upper Layer' classification, stricter norms for bank-linked NBFCs, and the removal of regulatory exemptions for government-owned entities. Infrastructure finance companies will see an increase in large exposure limits to 45% of their capital base.

What Happened

The Reserve Bank of India (RBI) has released its final framework for the scale-based regulation of Non-Banking Financial Companies (NBFCs). The central bank has set a clear asset-size threshold of ₹1 lakh crore to classify NBFCs into the 'Upper Layer'—a category for the largest, most systemically important financial institutions. This threshold will be reviewed every three years to keep pace with economic growth and market risks. The updated rules, which took effect immediately, signal a more stringent and unified approach to overseeing large non-bank lenders.

Why The Changes Matter

The regulator is moving toward an 'ownership-neutral' system, meaning that rules are being applied based on size and risk rather than whether the company is owned by the government, a bank, or private promoters. By bringing all entities under the same set of strict guidelines, the RBI aims to reduce systemic risks. When an NBFC grows large, its failure can create ripples across the entire financial system. These new norms ensure that large NBFCs, regardless of their parentage, must adhere to high standards of risk management, governance, and capital adequacy.

The Impact on Bank-Linked and Gov-Owned NBFCs

One of the most significant changes is the stricter oversight of bank-owned NBFCs. Regardless of their asset size, these entities must now comply with the stringent standards applicable to Upper Layer NBFCs, similar to the regulations banks themselves follow. This is a clear move to prevent regulatory arbitrage, where financial activities are moved to less regulated entities to avoid strict bank norms.

Similarly, government-owned NBFCs have lost the exemptions they previously enjoyed. They are now required to follow uniform exposure limits—the cap on how much a lender can lend to a single borrower or group. While existing loans that exceed these limits are allowed to continue until they run off, the companies cannot extend fresh credit that breaks these new caps.

Why Infrastructure Lenders Get a Boost

In a targeted measure to support long-term economic growth, the RBI has provided relief to Infrastructure Finance Companies (IFCs) in the Upper Layer. The regulator has increased the 'Large Exposure Limit' for these companies from 35% to 45% of their eligible capital base. This adjustment acknowledges the specialized and long-term nature of infrastructure financing. Without this change, IFCs might have struggled to fund large-scale projects, as high project costs often require significant exposure to single large borrowers or project groups. This move is intended to ensure that essential national projects do not face funding delays.

What Investors Should Track Next

Investors should pay close attention to how these changes influence the operational costs and lending strategies of large NBFCs. Higher compliance requirements often mean that companies may need to invest more in governance and risk reporting, which could impact their near-term operating margins.

For government-owned NBFCs (like REC, PFC, or IRFC), tracking how they adjust their exposure profiles over the coming quarters will be important. Similarly, for bank-linked NBFCs, monitoring their capital adequacy and operational efficiency under the new, stricter 'bank-like' norms will be key for assessing their long-term growth capacity. The three-year review cycle for the asset-size threshold also means that the list of companies in the 'Upper Layer' will be dynamic, and companies nearing the ₹1 lakh crore mark will need to prepare for enhanced regulatory scrutiny well in advance.