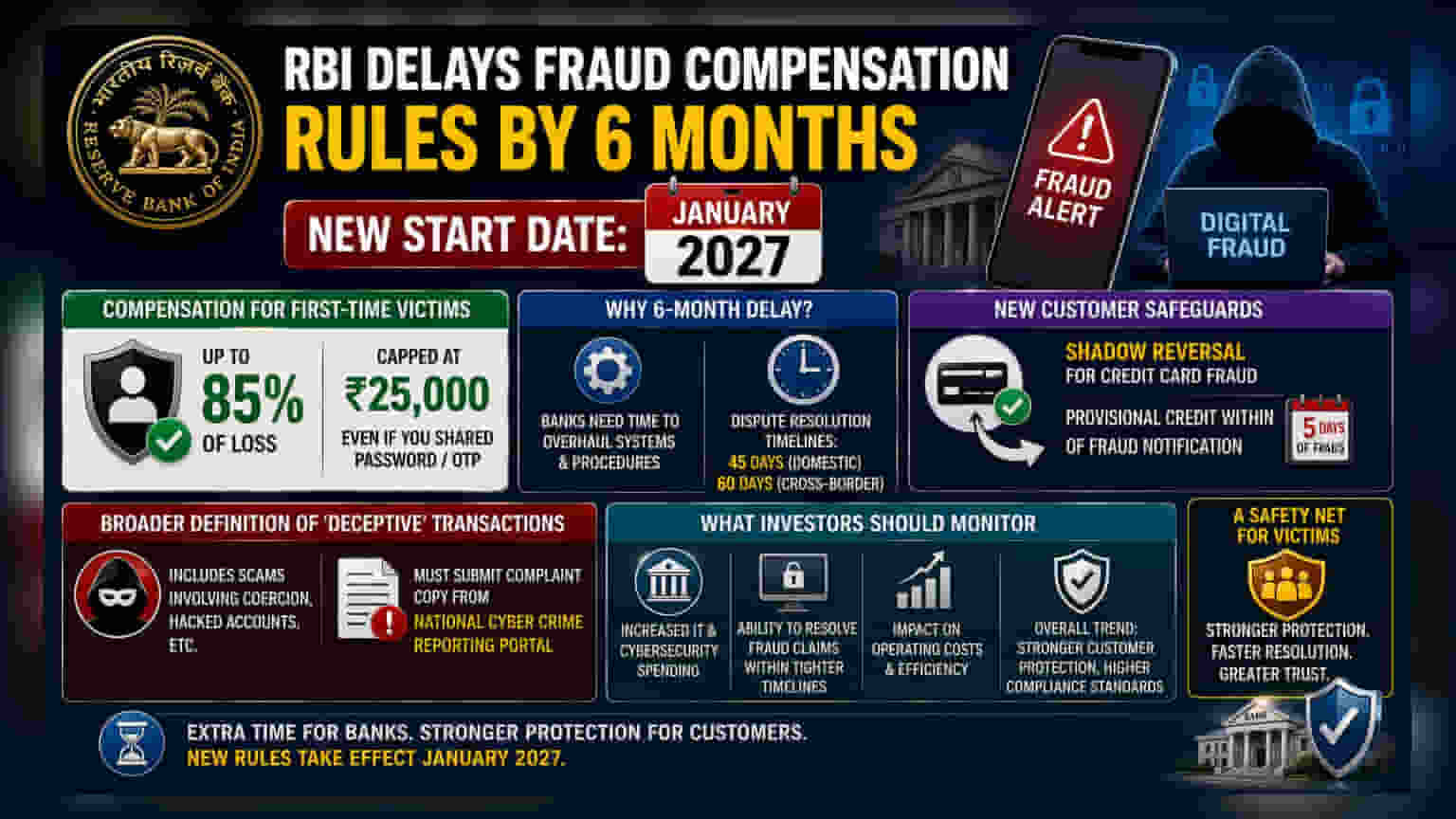

The Reserve Bank of India has extended the deadline for its new electronic fraud compensation norms to January 2027. While this gives banks more time to upgrade systems, the upcoming rules will provide first-time victims up to Rs 25,000 in relief. Investors should note that banks now face stricter mandates, including a five-day 'shadow reversal' timeline for credit card fraud, which may impact operational workflows.

What Happened

The Reserve Bank of India (RBI) has decided to push back the implementation of its new electronic fraud compensation framework by six months, moving the start date to January 2027. This regulatory move aims to provide a safety net for victims of digital fraud. Under the proposed guidelines, first-time victims can seek compensation for up to 85% of their losses, capped at Rs 25,000. This relief is designed to apply even if the victim inadvertently shared sensitive details like passwords or One-Time Passwords (OTPs), a scenario previously often classified as an 'authorized' transaction with no recourse.

Why Banks Needed More Time

The six-month extension reflects the operational challenges financial institutions face. The RBI acknowledged that banks require significant time to overhaul their backend systems and procedures to comply with the new rules. This includes adjusting for faster dispute resolution timelines—now set at 45 days for domestic cases and 60 days for cross-border issues. For investors, this adjustment highlights the ongoing need for banks to increase their spending on IT infrastructure and cybersecurity to meet stricter regulatory standards.

New Customer Safeguards

A notable change in the upcoming rules is the 'shadow reversal' mechanism for credit card fraud. Under this system, if a customer reports a fraudulent credit card transaction, the bank is required to provisionally credit the disputed amount back to the customer’s account within five days of the notification. This is a move to protect the customer while the bank investigates the transaction. While this is a positive step for consumer rights, it places higher operational pressure on banks to process fraud claims with greater speed and efficiency.

Changes to Transaction Definitions

The RBI is also broadening the scope of what it defines as a 'deceptive' transaction. Previously, many scams involving coercion or hacked accounts were treated as transactions authorized by the user, leaving the victim with little protection. The new definitions aim to widen the scope of recourse, meaning more types of digital fraud will now fall under the protection umbrella. However, this comes with stricter requirements for customers, who must provide an official complaint copy from the National Cyber Crime Reporting Portal to qualify for claims.

What Investors Should Monitor

Investors tracking the banking sector should watch for the associated costs of these compliance measures. As banks prepare for the January 2027 deadline, there may be an uptick in technology-related capital expenditure. Additionally, the ability of banks to efficiently manage fraud resolution within the new, tighter timelines will be a metric of operational capability. While the delay provides breathing room for system implementation, the overall trend toward stricter consumer protection and faster dispute resolution remains a key operational theme for the banking industry.