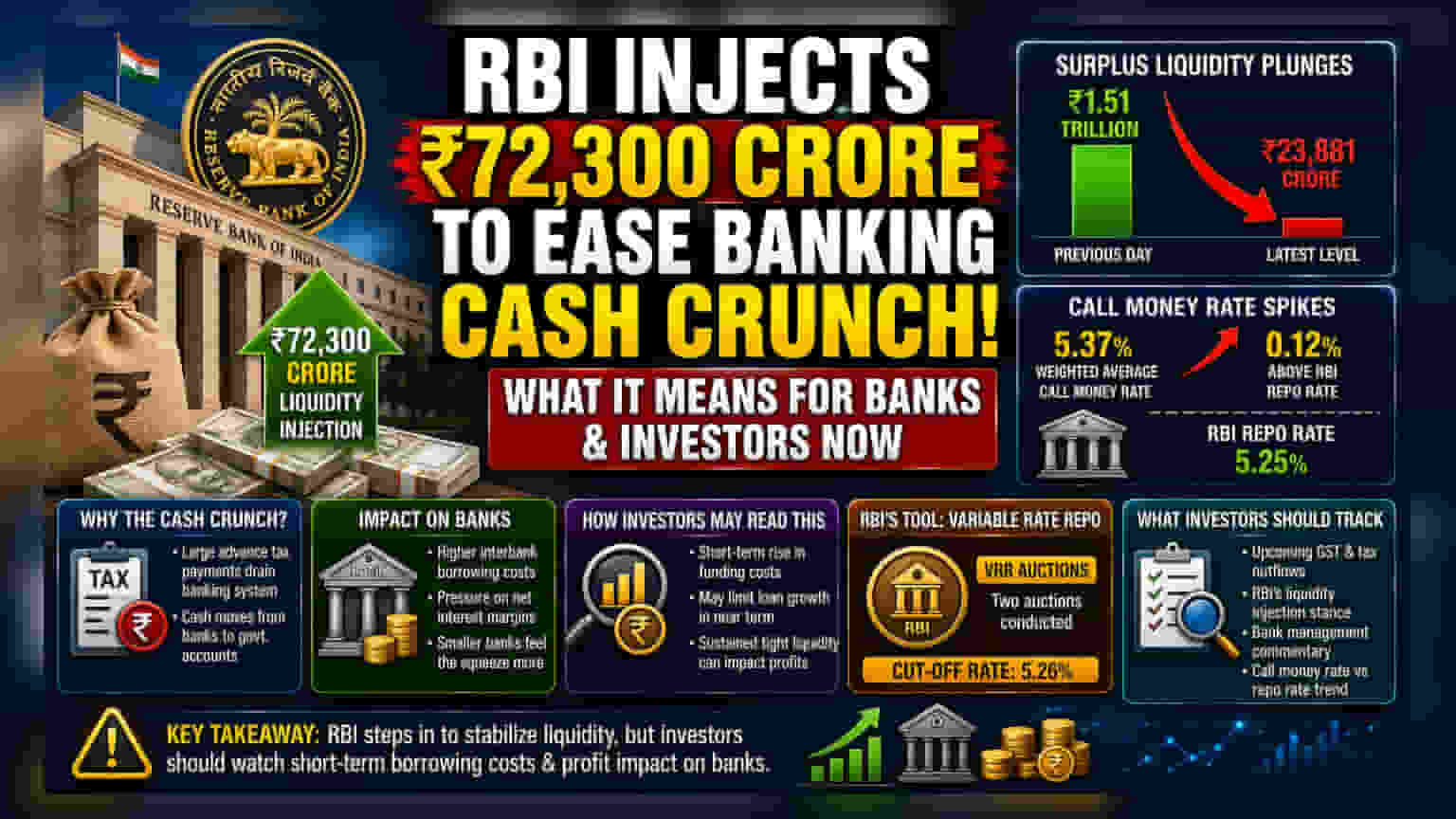

The Reserve Bank of India has injected ₹72,300 crore into the banking system to tackle a sharp liquidity squeeze caused by advance tax payments. With surplus cash dropping significantly and short-term borrowing costs rising above the repo rate, investors should monitor how this tightening impacts bank profit margins and funding costs in the near term.

What Happened

The Reserve Bank of India (RBI) recently injected ₹72,300 crore into the banking system to address a sudden shortage of funds. This was done through variable rate repo (VRR) auctions, a tool used by the central bank to manage short-term cash flow needs. This intervention became necessary after surplus liquidity in the banking system fell sharply to ₹23,881.21 crore, a steep decline from the previous day's level of ₹1.51 trillion. The central bank conducted two separate auctions to pump this capital into the market, with the primary auction seeing a cut-off rate of 5.26%.

Why the Cash Crunch Occurred

Banking liquidity often fluctuates due to government-related cash movements. In this instance, the tightening was largely driven by advance tax payments. When corporations and individuals make large tax payments to the government, cash flows out of the banking system and into government accounts. This reduces the amount of surplus money available with commercial banks to lend to one another. The sharp drop from over ₹1 trillion to roughly ₹23,800 crore shows how quickly these tax outflows can drain the system.

Understanding the Banking Impact

When liquidity tightens, the cost of borrowing money in the interbank market typically rises. This was visible on Wednesday, as the weighted average call money rate—the interest rate banks charge each other for overnight loans—traded at 5.37%. This rate is 0.12% higher than the RBI’s policy repo rate. For investors, this is a signal that banks are facing higher short-term costs to keep their operations running smoothly. When banks have to pay more for funds, it can put pressure on their net interest margins, which is the difference between the interest they earn on loans and the interest they pay on deposits.

How Investors May Read This

The immediate effect of this liquidity crunch is an increase in short-term borrowing costs for banks. While larger banks may have better access to funds, smaller or mid-sized lenders might feel this pressure more directly. If tight liquidity persists, it may limit the ability of banks to aggressively grow their loan books in the short term, as they focus on managing their own cash positions. Investors typically monitor these liquidity fluctuations because sustained tight conditions can eventually impact the quarterly profitability of banking stocks, especially if banks are unable to pass on higher funding costs to their customers immediately.

What Investors Should Track

Moving forward, market participants will likely keep an eye on upcoming tax deadlines, such as Goods and Services Tax (GST) outflows, which can continue to pull cash out of the system. The RBI’s willingness to conduct more liquidity injections will be a key factor in keeping borrowing rates stable. Investors should watch for management commentary from major banks in upcoming result seasons regarding their cost of funds and how they are managing liquidity during these high-outflow periods. Additionally, any trend of call money rates remaining consistently above the repo rate would indicate that the central bank needs to remain active with its liquidity management operations.