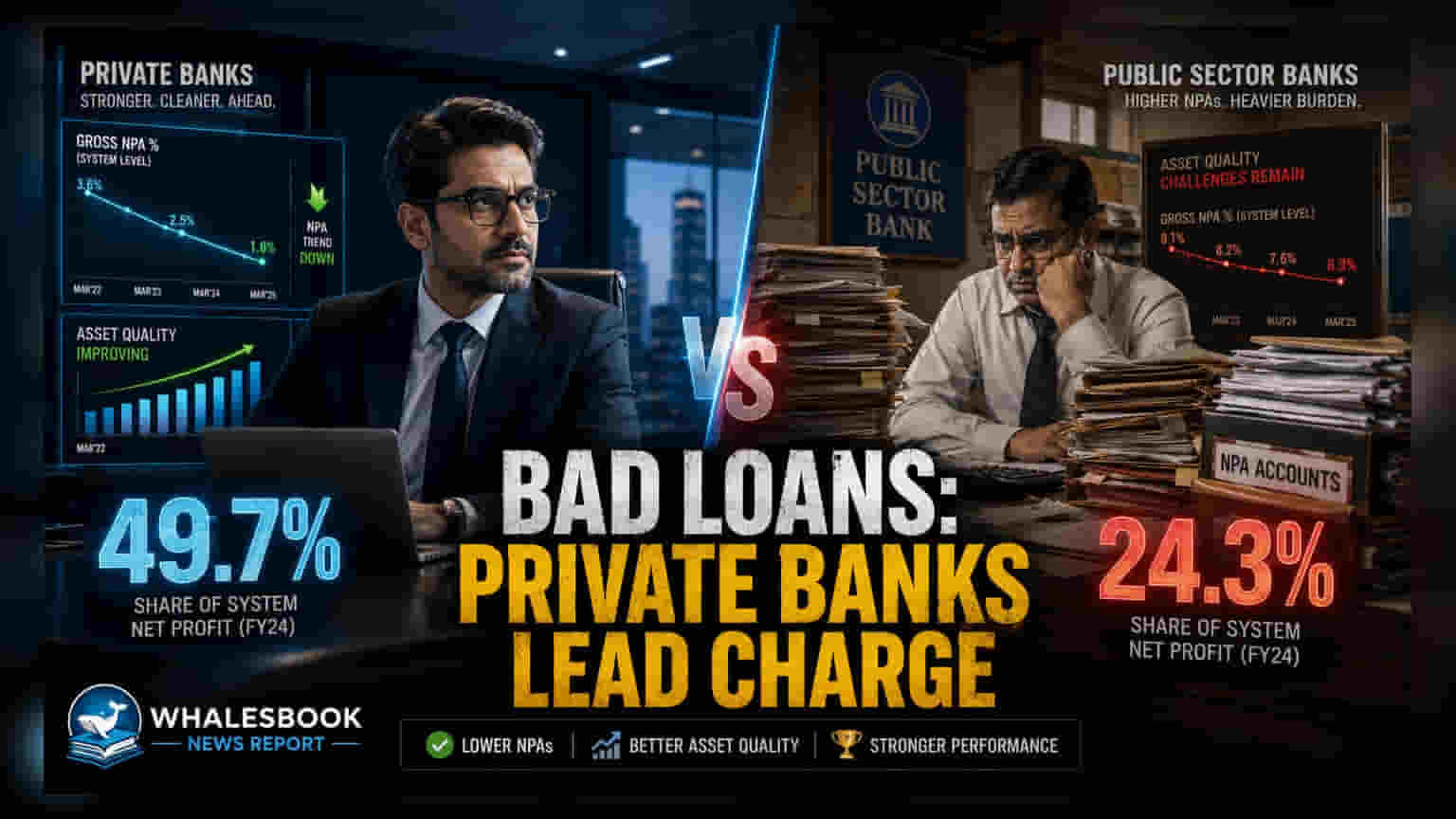

Private sector banks cleared nearly half of their non-performing assets in FY26, far exceeding the 24.3% write-off rate recorded by public sector banks. This strategy helps private lenders maintain cleaner balance sheets, though public banks continue to hold a larger share of the total bad loans in the banking sector.

Indian private sector banks have intensified their efforts to clean up their balance sheets, with new data showing they wrote off 49.7% of their non-performing assets, or bad loans, during the 2025-26 fiscal year. This aggressive approach is notably higher than that of public sector banks, which removed 24.3% of their bad loans from their books during the same period.

Impact on Bank Balance Sheets

While private banks are moving quickly to remove bad loans, public sector banks still account for 63.2% of the total bad loans within the Indian banking system. The sector as a whole wrote off approximately Rs 1.28 lakh crore in bad loans during FY26, representing about 33.2% of total non-performing assets. Write-offs are a common accounting practice where banks remove loans that are considered unrecoverable from their active balance sheets, allowing them to focus on new lending.

Strategic Differences in Loan Recovery

The difference in write-off rates highlights a divergence in how different types of banks handle loan defaults. Private banks often prioritize cleaning their balance sheets to improve financial ratios and reduce the burden of older, non-performing accounts. In contrast, public sector banks frequently focus on long-term recovery processes, such as legal actions or restructuring, to claw back funds over time.

Industry analysts suggest that the rise in write-offs at private banks may be linked to the current credit landscape. Deterioration in certain retail loan segments and microfinance portfolios has necessitated higher provisions and subsequent write-offs. By proactively clearing these accounts, private lenders aim to prevent non-performing assets from accumulating and affecting their overall profitability and capital adequacy.

For investors, the primary monitorable will be the impact of these write-offs on the profit margins of individual banks. While cleaning a balance sheet is generally seen as a positive step for long-term health, investors should track whether the pace of new bad loan formation remains under control. High write-off levels in sectors like microfinance or unsecured retail credit remain a risk factor that could affect future earnings quality for banks heavily exposed to these segments. Moving forward, the focus will be on the asset quality performance of both private and public lenders in the upcoming quarterly results to see if these write-off patterns continue to stabilize the banking sector.