Motilal Oswal Financial Services predicts a major turnaround for private sector banks, forecasting 21% earnings growth compared to 8% for public sector lenders by FY28. While strong credit demand supports this outlook, investors should keep an eye on margin pressures and risks tied to unsecured retail lending, which remains a key area of regulatory focus.

What Happened

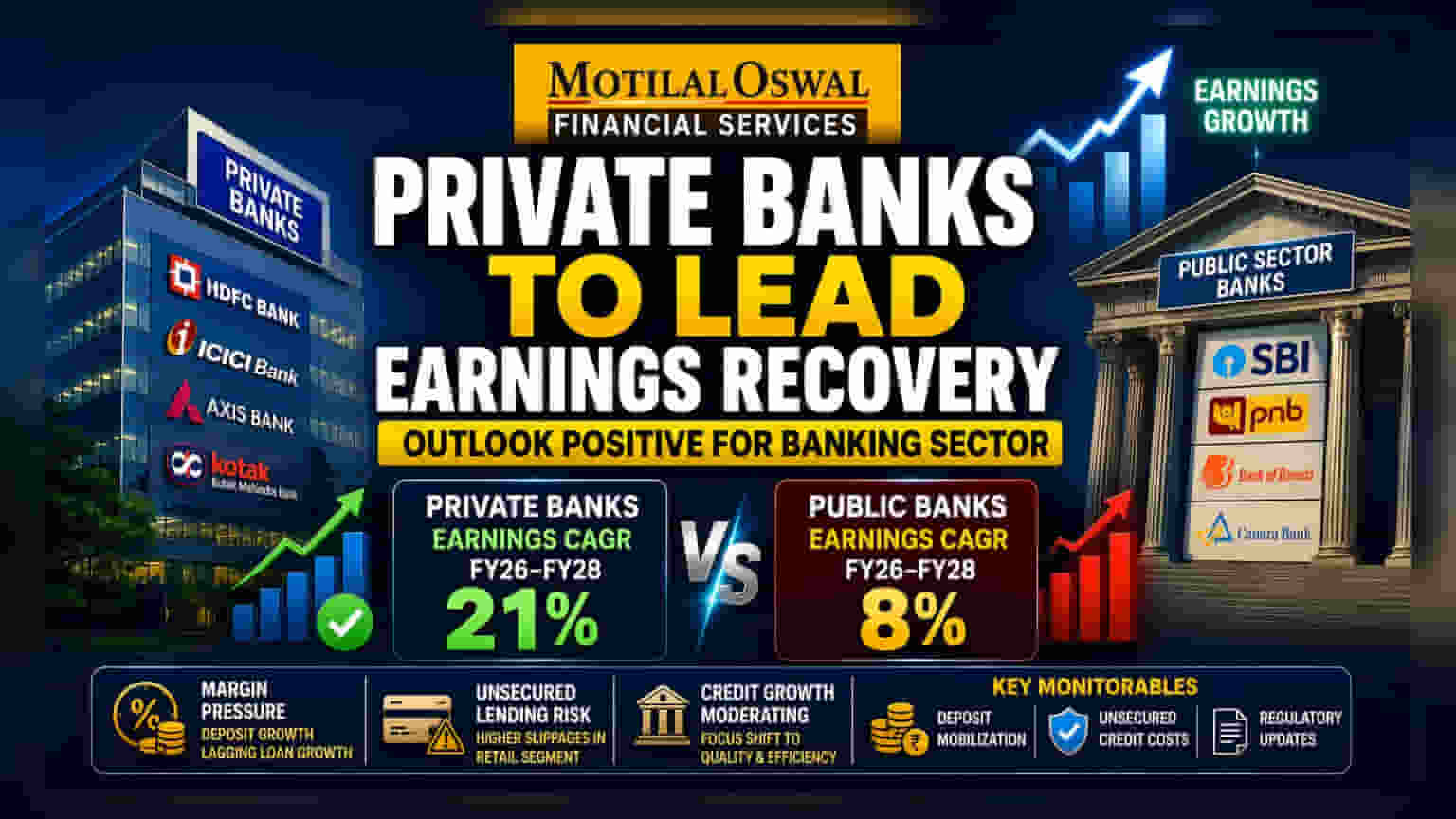

Motilal Oswal Financial Services (MOFSL) has released a positive outlook for India's banking sector, identifying large private banks as the primary drivers of an expected earnings recovery. According to the report, private sector banks are projected to outperform their public sector counterparts over the next few years. The brokerage estimates that private banks will deliver an earnings compound annual growth rate (CAGR) of approximately 21% between FY26 and FY28. In contrast, public sector banks are expected to see a more modest earnings CAGR of roughly 8% during the same period.

Why This Matters For Investors

The forecast highlights a potential shift in momentum within the Indian banking sector. For the past two years, many investors favored public sector banks due to their strong balance sheet improvements and operational turnarounds. However, this report suggests the tide may be turning back toward large private lenders. The projected 21% earnings growth reflects expectations that these banks have successfully navigated recent macroeconomic headwinds and are now positioned for a period of improved profitability and stable growth.

The Margin And Deposit Challenge

While the earnings outlook appears optimistic, the sector is not without its hurdles. Banking institutions across India are currently facing a persistent struggle to attract deposits at favorable interest rates. With deposit growth rates often lagging behind loan growth, banks have been forced to rely on more expensive sources of funding to meet credit demand. This dynamic places pressure on Net Interest Margins (NIM)—the difference between interest earned on loans and interest paid on deposits. Investors should note that even with robust loan growth, if banks cannot secure cheaper deposits, their overall profit margins may remain under pressure.

The Unsecured Lending Risk

A critical factor for investors to monitor is the exposure of private banks to unsecured retail lending, such as personal loans and credit cards. Data from financial stability reports suggests that private sector banks often have a higher share of these unsecured portfolios compared to public sector banks. Regulatory bodies, including the Reserve Bank of India, have expressed caution regarding rising slippages in this specific segment. While overall asset quality remains stable, a significant portion of new bad loans in the retail segment has originated from unsecured lending books. Banks with aggressive growth in this area may face higher credit costs if economic conditions tighten.

Broader Sector Context

Broadly, the Indian banking sector is transitioning from a phase of high-speed credit expansion to a more measured growth environment. Industry estimates project credit growth to moderate in FY27 compared to the double-digit highs seen in FY26. This moderation is a natural part of the economic cycle, as banks focus on maintaining a healthy credit-to-deposit ratio and prioritizing asset quality over aggressive loan book expansion. The focus for management teams across the sector is shifting toward efficiency, digital adoption, and managing the cost of funds rather than just chasing volume.

What Investors Should Track

As the sector evolves, investors may want to track several key performance indicators. First, deposit mobilization remains the most critical monitorable; banks that successfully grow their low-cost deposit base (Current and Savings Accounts) are better positioned to protect their margins. Second, credit cost trends in the unsecured retail segment will determine whether the banks' profitability targets are met. Finally, updates on regulatory policies regarding unsecured lending and provisioning requirements will provide insight into the potential impact on capital buffers. Watching these factors will help investors gauge whether the projected earnings growth can be sustained in a competitive and highly regulated environment.