Paisabazaar and SBM Bank India have introduced a secured credit card requiring a minimum ₹2,000 fixed deposit. This move targets the growing 'new-to-credit' population in India, offering a safer way for users to build credit history while earning interest. For investors, this partnership highlights the focus on low-risk lending products within the fintech space and the continued push to capture the underserved credit market.

What Happened

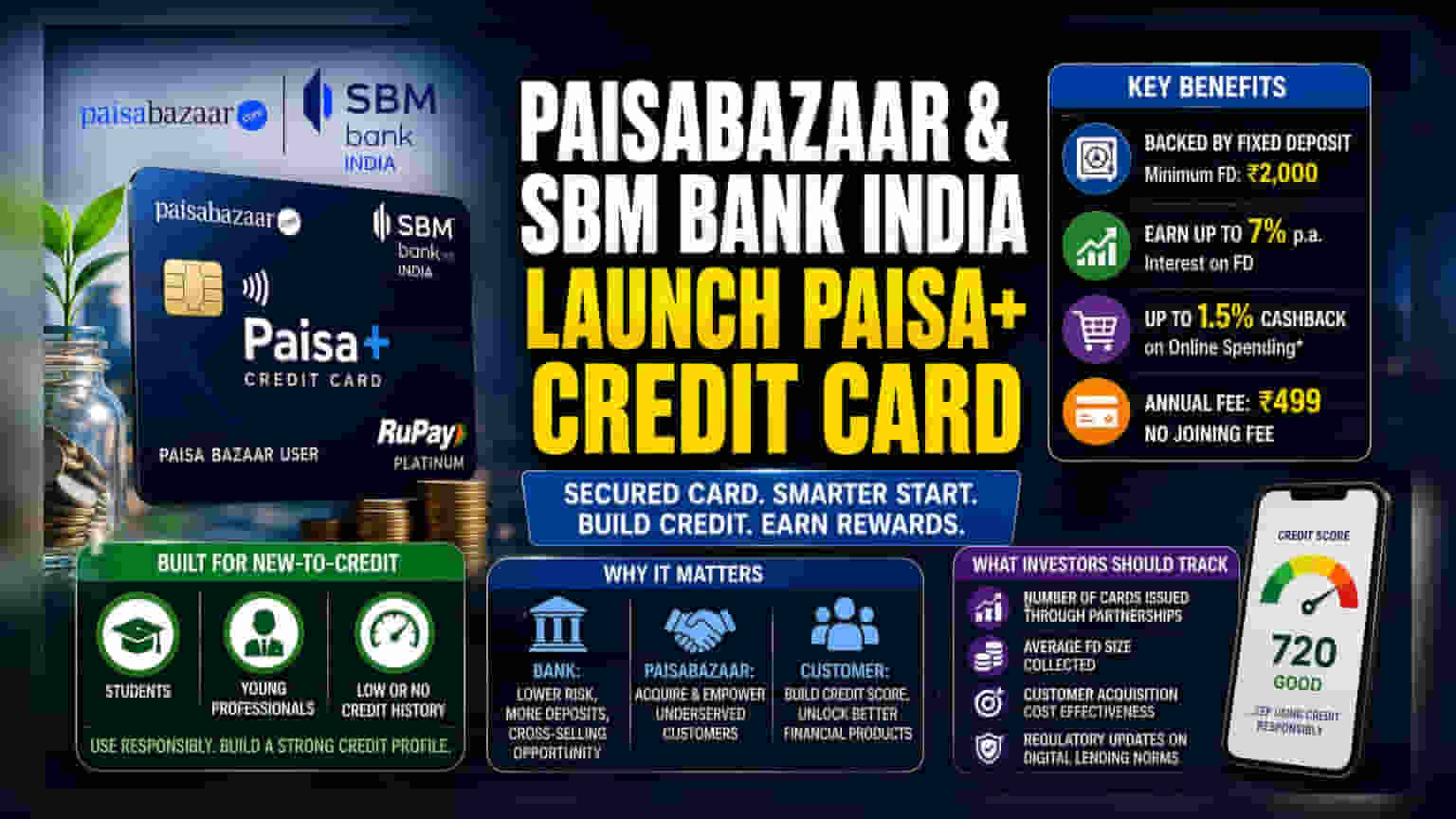

Financial marketplace Paisabazaar and SBM Bank India have announced the launch of the SBM Paisabazaar Paisa+ Credit Card. This is a secured credit card, which means the card is backed by a fixed deposit rather than being based on an unsecured credit score. Users can get this card by opening a fixed deposit with SBM Bank India with a minimum amount of ₹2,000. The credit limit on the card is tied to the amount deposited. The product offers an interest rate of up to 7% per annum on the fixed deposit, and cardholders can earn up to 1.5% cashback on online spending, depending on the deposit balance. The card carries an annual fee of ₹499 but has no joining fee.

The Strategy Behind Secured Cards

The launch focuses on the 'new-to-credit' segment. This includes students, young professionals, and individuals who do not have a credit history or have a low credit score, making it difficult for them to get traditional unsecured credit cards. By requiring a fixed deposit as collateral, the bank reduces its risk significantly. For the customer, it provides a structured way to build a credit profile. If used responsibly, this helps the customer become eligible for unsecured loans or cards in the future. For the fintech platform, this product helps in acquiring customers who might otherwise be rejected by standard credit underwriting systems.

Why This Matters for the Credit Market

Secured credit cards have become a standard tool for digital lenders and banks to expand their customer base without taking on high credit risk. In the Indian market, there is a large population that remains underserved by formal credit channels. Partnerships like this allow the marketplace to offer a financial product that serves two purposes: acting as a savings tool (via the FD) and a financial product (the credit card). For the bank, it is a way to gain deposits and cross-sell other banking products to new customers. The model is essentially a volume-driven play, where the goal is to bring a large number of first-time users into the banking ecosystem.

The Risk and Regulatory Landscape

While this product is low-risk for the bank due to the collateral, there are broader factors investors often watch in this space. The digital lending and co-branded credit card sector has seen increased scrutiny from the Reserve Bank of India (RBI) regarding data privacy, compliance, and lending practices. Investors typically monitor how such partnerships manage these regulatory requirements. Furthermore, the cost of acquiring customers (CAC) in the competitive fintech market can be high. If a company spends too much on marketing to get users for such products, it can put pressure on profit margins. Success depends on the ability to scale efficiently without overspending on customer acquisition.

What Investors Should Track

Investors may want to monitor the uptake of this product and the feedback from the new-to-credit segment. Key monitorables include the total number of cards issued through such partnerships, the average size of the fixed deposits collected, and the overall cost efficiency of the customer acquisition process. Additionally, any updates from regulatory bodies regarding digital lending norms are important, as they influence how fintech companies and banks structure their partnerships and credit products in the future.