The Operational Divergence

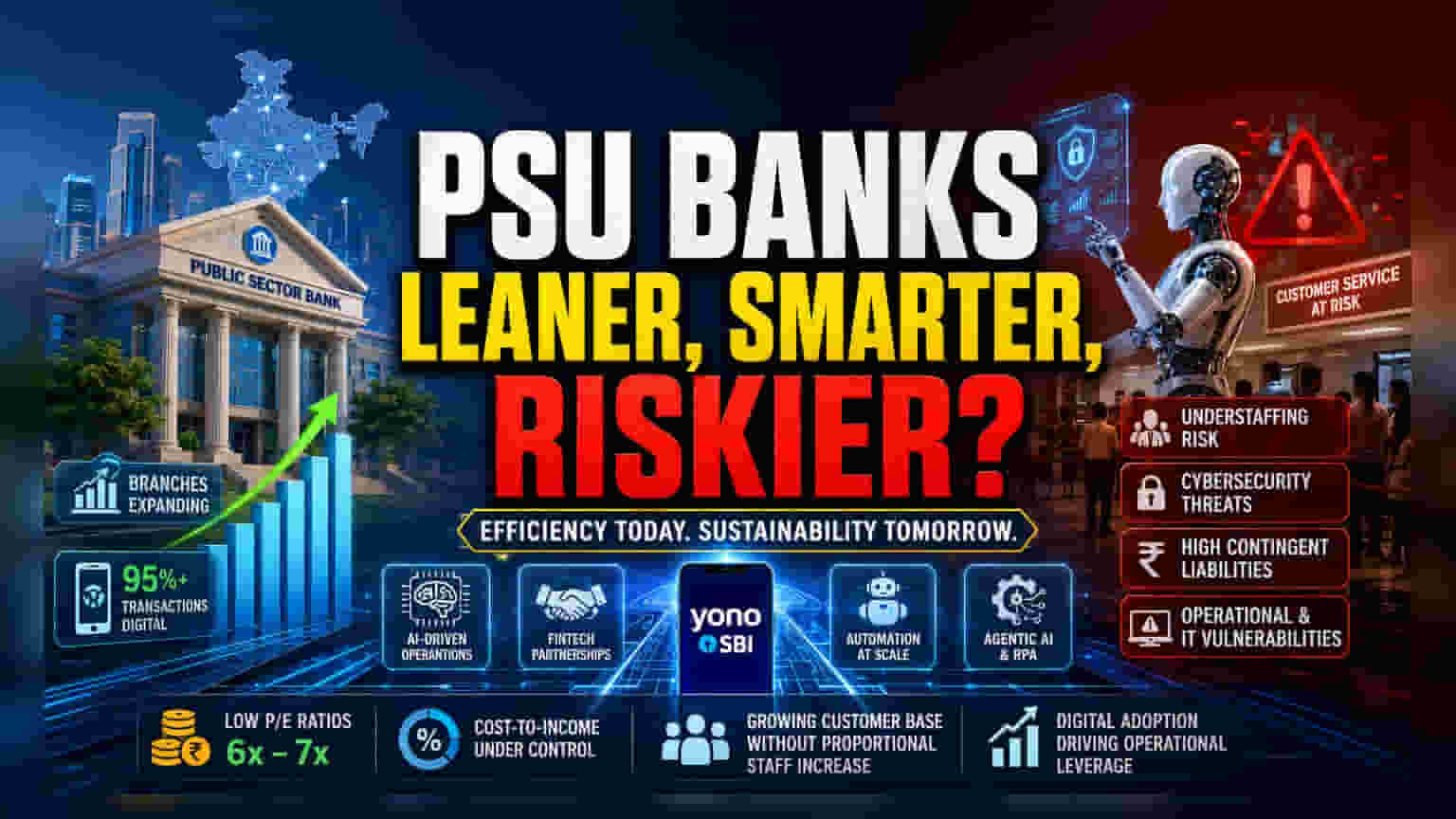

Public sector banks are currently navigating a structural paradox. Even as these institutions pursue aggressive physical branch expansion to deepen market penetration, the underlying workforce dynamics reflect a clear prioritization of automation over human capital. An examination of financial performance and staffing metrics between FY22 and FY26 reveals that for most state-run lenders, branch counts have climbed while employee numbers have stagnated or contracted. This decoupling of physical footprint from labor force indicates that banks are increasingly moving toward a high-tech, low-touch model.

Efficiency Drivers and Valuation Implications

This trend is underpinned by a transition toward digital-first operations. With many lenders reporting that upwards of 95% of transactions now occur through digital channels, the function of the physical branch has evolved from a transaction center to a sales and advisory hub. State Bank of India, which maintained a network of over 23,000 branches as of FY26, continues to leverage its Yono platform to capture a significant share of new accounts. Similarly, Indian Bank’s integration of AI-driven platforms and fintech partnerships has enabled it to scale its digital business to Rs 2.72 lakh crore. For investors, this shift offers a unique valuation lens. Banks like Bank of Baroda and Canara Bank are currently trading at low single-digit P/E ratios, often hovering between 6x and 7x, reflecting market caution regarding their ability to sustain growth. While cost-to-income ratios remain a focus, the ability to serve a growing customer base without a proportional increase in salary expenses is a central pillar of the current efficiency narrative.

The Forensic Bear Case: Risks in Lean Banking

Despite the apparent efficiency gains, the aggressive pursuit of a leaner model carries significant long-term risks. Employee unions have frequently voiced concerns that critical understaffing is degrading customer service quality, a factor that could impact long-term brand loyalty and deposit growth. Furthermore, as bank operations become increasingly reliant on algorithmic decision-making and robotic process automation, the sector faces heightened operational risks related to cybersecurity and systemic IT vulnerabilities. Unlike private-sector peers that have often pioneered these technological shifts with higher agility, public sector banks must navigate rigid administrative structures, which can impede the seamless integration of advanced AI. Contingent liabilities, which remain substantial across these lenders—frequently exceeding several lakh crores—further exacerbate the risk profile for investors looking for stability in a rapidly digitizing sector.

Future Outlook: Technology as the Primary Lever

The move toward agentic AI and automated reconciliation suggests that PSU banks will continue to decouple branch growth from staff recruitment. Market consensus expects that as digital adoption rates continue to climb, especially in retail and agriculture segments, the operational leverage of these institutions will improve. However, the path forward remains dependent on whether these banks can successfully manage the human resource challenges that accompany rapid automation without triggering wider labor unrest or service-related regulatory scrutiny.