Public sector banks (PSBs) are aggressively raising term deposit rates to reclaim market share from private lenders. This move is a strategy to secure liquidity as loan growth outpaces deposits. Investors should note that while this may help attract more savers, it risks squeezing the Net Interest Margins (NIMs) of public banks, as the cost of borrowing rises.

What Happened

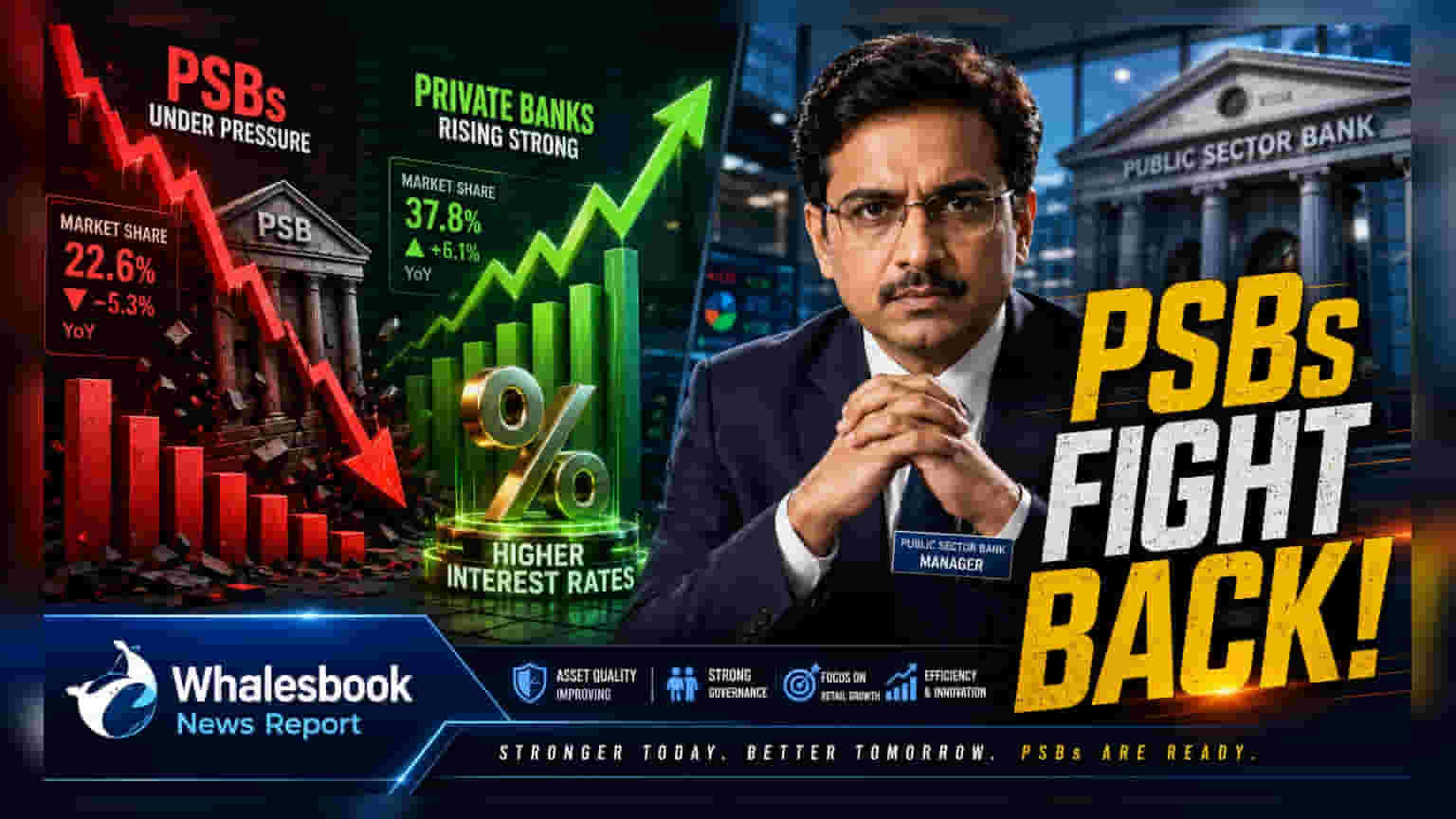

Public sector banks (PSBs) in India have begun raising interest rates on fixed and term deposits. This move marks a strategic shift to combat the steady loss of market share to private sector competitors over the last decade. While PSBs are increasing rates to attract depositors, private sector banks have taken a different path, recently reducing their rates. RBI data indicates that the weighted average rate for fresh term deposits at PSBs rose by 15 basis points to 6.33% in May, contrasting with a 5-basis-point cut by private banks to 5.96%.

Why Banks Need Deposits Now

The banking industry is currently facing a tight liquidity environment. Loan growth has been strong, meaning banks are lending out money faster than they are collecting it from depositors. This is reflected in the credit-deposit ratio—a metric that shows how much of a bank's deposits are being used to fund loans—which remains high at approximately 82.5% for the system. When this ratio is high, it indicates that banks are under pressure to find more funds to keep up with loan demand. For PSBs, losing further deposit market share is a challenge they are now actively trying to prevent by offering more competitive interest rates.

The Margin Trade-Off

For investors, the most critical impact of this rate hike is on the Net Interest Margin (NIM). The NIM is essentially the difference between the interest a bank earns on loans and the interest it pays to depositors. Traditionally, PSBs have relied on a large base of low-cost current and savings accounts (CASA) to maintain healthy margins. However, by hiking interest rates on term deposits, the cost of funds for these banks increases. If banks cannot pass on these higher costs to borrowers by raising loan rates proportionally, their profit margins will come under pressure.

Why Private Banks Are Different

Private banks have been more selective in their approach to deposit gathering. Having grown their deposit market share from 19.4% to 36.4% over the last decade, private lenders have a more diverse customer base and stronger fee-based income streams. This allows them more flexibility to prioritize profit margins over aggressive deposit accumulation. In contrast, PSBs are now choosing to sacrifice some short-term profitability to stop the erosion of their deposit base.

What Investors Should Track

Investors monitoring banking stocks should keep a close watch on a few specific indicators in the upcoming quarterly results. First, monitor the reported Net Interest Margin (NIM) to see if the cost of the new, higher-interest deposits is hurting profitability. Second, track the 'cost of funds' reported by these banks; a rising cost of funds without a corresponding rise in loan yields is a negative signal for margins. Finally, watch management commentary on deposit growth. The key question for shareholders will be whether these higher rates are successfully bringing in new retail depositors or if the banks are simply paying more for existing ones without gaining significant new market share.