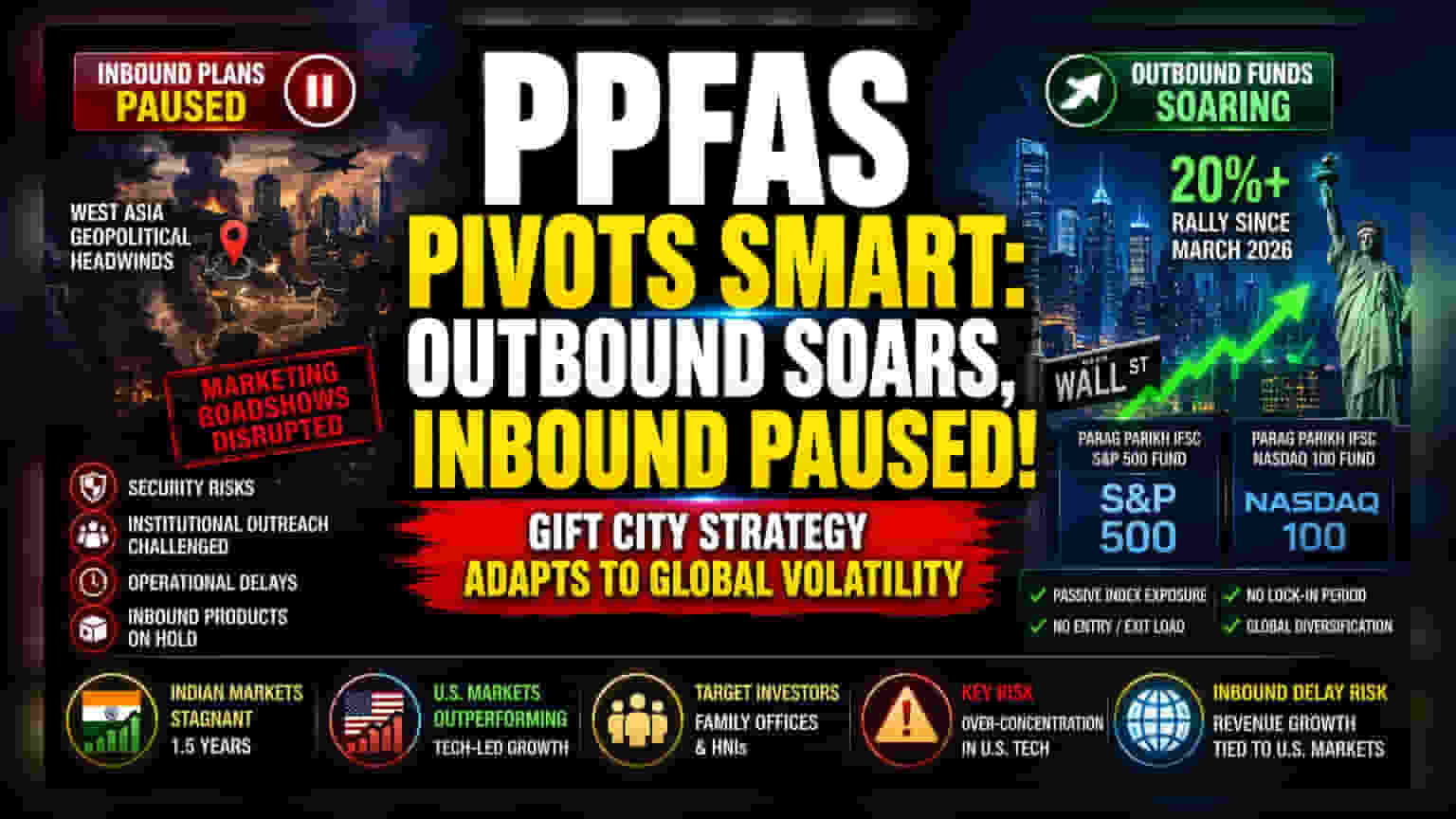

Navigating Geopolitical Headwinds

The strategic pivot by PPFAS Alternate Asset Managers reflects the deepening fragility of cross-border financial marketing during periods of acute regional volatility. While the firm initially envisioned a synchronized rollout of both inbound and outbound investment vehicles from the International Financial Services Centre (IFSC) in GIFT City, the reality of the current security climate has forced a divergence. Managing physical marketing roadshows and high-level institutional outreach in West Asian markets has become operationally taxing, effectively creating an artificial ceiling for the launch of Indian-centric equity products.

The Performance Divergence

Contrasting sharply with the stalled inbound plans, the firm’s outbound suite—specifically the Parag Parikh IFSC S&P 500 and Nasdaq 100 funds—has found tailwinds in the very volatility that disrupted other operations. Since their debut in March 2026, these funds have mirrored the aggressive recovery seen across US indices, which have climbed over 20 percent. This rapid appreciation has served as a tactical validation for the fund house’s decision to emphasize international diversification. By focusing on passive, index-linked exposure, the firm is effectively capturing the momentum of US-based innovation sectors, which continue to decouple from the broader geopolitical malaise affecting emerging markets.

Structural Limitations and Market Sentiment

The firm’s public stance regarding the relative stagnation of Indian equities over the last year-and-a-half highlights a broader trend among asset managers operating within the IFSC. By highlighting the lack of growth in domestic indices compared to the technological gains in the US, PPFAS is catering to a sophisticated investor base—family offices and high-net-worth individuals—who prioritize performance and liquidity. The absence of traditional friction points, such as entry or exit loads and restrictive lock-in periods, remains a core selling point for these GIFT City products, positioning them as flexible vehicles for global capital reallocation.

The Risk of Over-Concentration

While the current narrative favors the firm’s US-centric strategy, institutional risk remains elevated. Relying heavily on the performance of the S&P 500 and Nasdaq 100 introduces significant beta exposure to the US technology sector, which faces its own headwinds regarding antitrust regulations and interest rate sensitivity. Furthermore, the inability to execute on the inbound mandate exposes the firm to a lack of product diversity. If the West Asian crisis persists, the company faces a protracted period where its revenue growth remains tethered exclusively to its performance in foreign markets, leaving it vulnerable to any sudden correction in US equity pricing.