The Valuation Gap

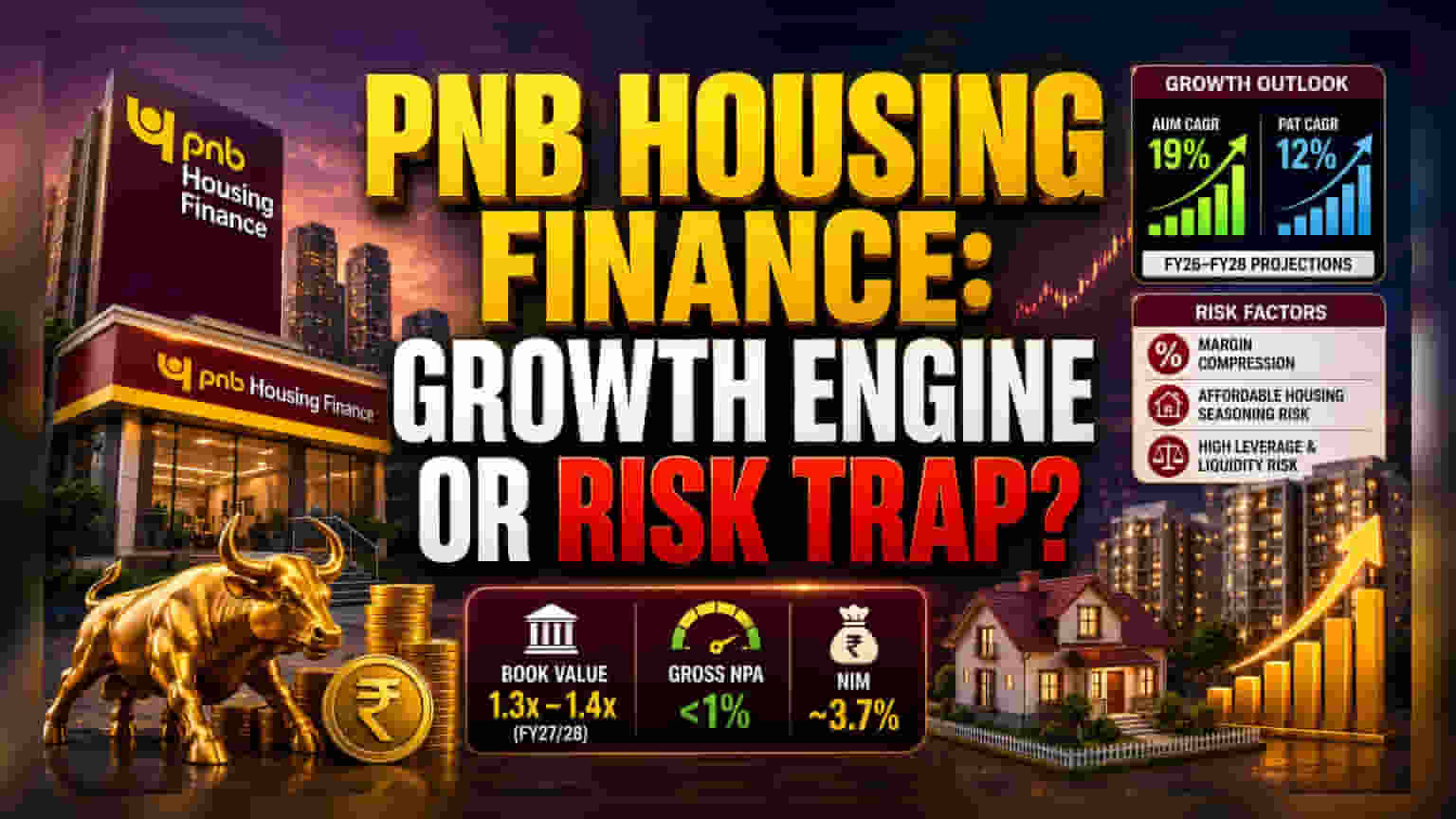

PNB Housing Finance has captured institutional attention as it balances aggressive expansion with structural transformation. While current market valuations see the stock trading at roughly 1.3 to 1.4 times FY27/28 book value, the bullish thesis from Motilal Oswal rests on the company’s ability to migrate its loan mix toward the affordable and emerging housing segments. This transition is not merely about volume; it is a margin-optimization strategy designed to counter the softening of yields observed across the broader non-banking financial company (NBFC) sector.

Analytical Deep Dive: The Growth Catalyst

The firm's roadmap, which aims to elevate the affordable housing share of its retail portfolio from 40% toward 50%, is supported by a significant expansion in branch infrastructure—nearly 40 new branches were added in the past fiscal year alone. Compared to peers like Aadhar Housing or Home First Finance, PNB Housing Finance leverages a massive existing distribution network to source high-yield loans at a lower cost of acquisition. Financial projections suggest a 19% CAGR for AUM and 12% for Profit After Tax (PAT) between FY26 and FY28. This expected performance is anchored in the company's improved operating leverage and the recent achievement of a sub-1% Gross NPA milestone, which signals a maturing risk-management framework after years of volatility.

The Forensic Bear Case

Despite the optimistic outlook, the institutional risk profile remains tied to the macro-environment. A primary concern for analysts is the potential for margin compression if the Reserve Bank of India (RBI) maintains current interest rates or refuses to pivot, which would limit the company's ability to pass on borrowing costs. Furthermore, the push into affordable and micro-housing introduces inherent seasoning risks. Unlike prime mortgage portfolios, these emerging segments require rigorous underwriting discipline; any unexpected deterioration in asset quality here would likely result in immediate credit cost spikes. Additionally, with promoter holding shifts and a debt-to-equity ratio that remains elevated compared to traditional bank competitors, PNB Housing Finance lacks the structural safety net of a diversified deposit-taking entity, leaving it more sensitive to liquidity cycles and sudden shifts in investor sentiment.

The Future Outlook

Market consensus remains cautiously optimistic, with the current price hovering near the 1,000 INR level, offering a significant spread to the street's revised targets. The success of the newly appointed strategy leadership will be tested by the ability to sustain these yields without sacrificing the quality of the retail franchise. Investors are closely watching upcoming quarterly disclosures for evidence that the affordable segment is scaling without diluting the company's net interest margins (NIM), which currently sit around 3.7%.