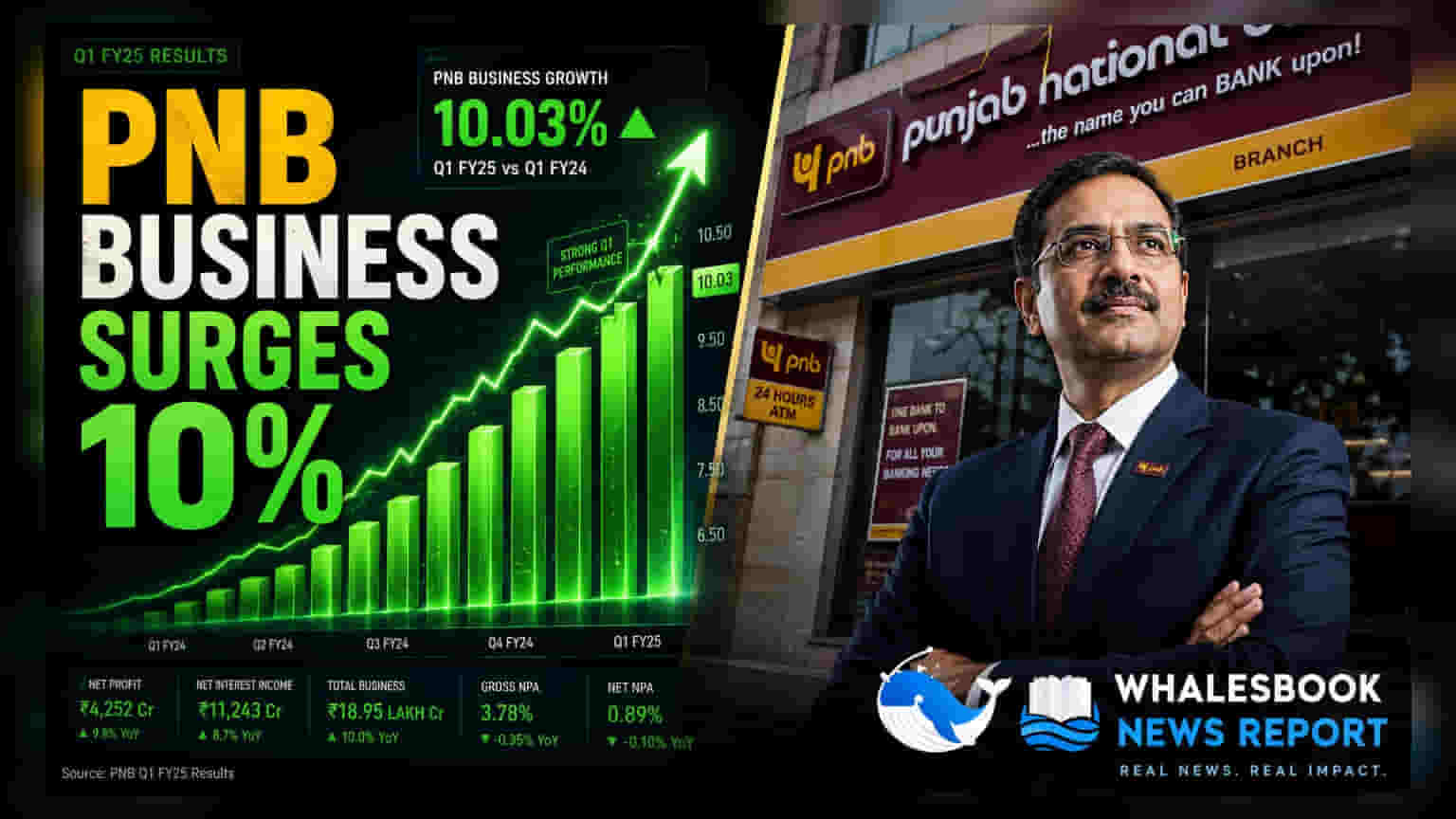

Punjab National Bank reported a 10.32% year-on-year growth in global business to nearly ₹30 lakh crore for the quarter ending June 2026. While the bank highlighted its strategy to boost retail and low-cost deposits, the stock closed marginally lower. Investors should note these figures are provisional and await final audit.

What Happened

Punjab National Bank (PNB) released its provisional business update for the first quarter of the 2026-27 financial year, showing a 10.32% year-on-year increase in global business. As of June 30, 2026, the bank's total global business reached ₹29,99,876 crore. This growth was driven by consistent increases in both deposits and loan disbursements. The bank noted that these figures are currently provisional and will be subject to final verification by the Statutory Central Auditors.

The Business Growth Picture

The data shows that the bank's global deposits stood at ₹16,70,180 crore, while global advances, which represent the money lent to customers, reached ₹12,05,763 crore. Within the domestic market, the bank recorded total business of ₹28,75,943 crore.

For investors, the Credit-Deposit (CD) ratio—a key metric indicating how much of a bank's deposits are being lent out—is a crucial figure to watch. PNB reported a CD ratio of 73.92% for the quarter. A healthy ratio typically suggests that the bank is effectively using its deposit base to generate income through loans without over-extending its liquidity.

Strategic Focus: RAM and CASA

The bank continues to emphasize its growth strategy centered on RAM advances and CASA. RAM stands for Retail, Agriculture, and MSME (Micro, Small, and Medium Enterprises) sectors. Focusing on these areas is a common strategy for Indian banks to diversify their loan books and reduce dependency on large corporate loans, which can sometimes carry higher risk.

Additionally, the bank is working to increase its CASA ratio. CASA refers to Current Account and Savings Account deposits, which are considered the lowest-cost source of funds for any bank. Because the interest paid on these accounts is generally very low compared to other deposits like Fixed Deposits (FDs), a higher CASA ratio can help a bank improve its profit margins. As of March 31, 2026, the bank's domestic CASA share was 37%.

How The Market Reacted

Despite the growth in business volume, shares of Punjab National Bank closed marginally lower, falling 0.51% to ₹106.95 on the BSE on July 2, 2026. Market reactions like this can happen for several reasons, such as investors booking profits after recent gains or waiting for the final audited financial results, which will provide details on net profit, interest margins, and asset quality (bad loans).

What Investors Should Track

As this was a provisional update, the actual financial performance will be revealed in the full quarterly results. Investors should look out for the following in the final report:

- Net Interest Margin (NIM): This measures the gap between the interest the bank earns on loans and the interest it pays on deposits. It is a primary driver of profit for banks.

- Asset Quality: Updates on Gross and Net Non-Performing Assets (NPAs) will be critical to see if the loan growth is healthy or if bad loans are increasing.

- Final Auditor Sign-off: Check if there are any significant differences between these provisional business numbers and the final audited financial statements.

- Cost of Funds: Monitor whether the bank is successfully maintaining its CASA levels to keep borrowing costs under control.