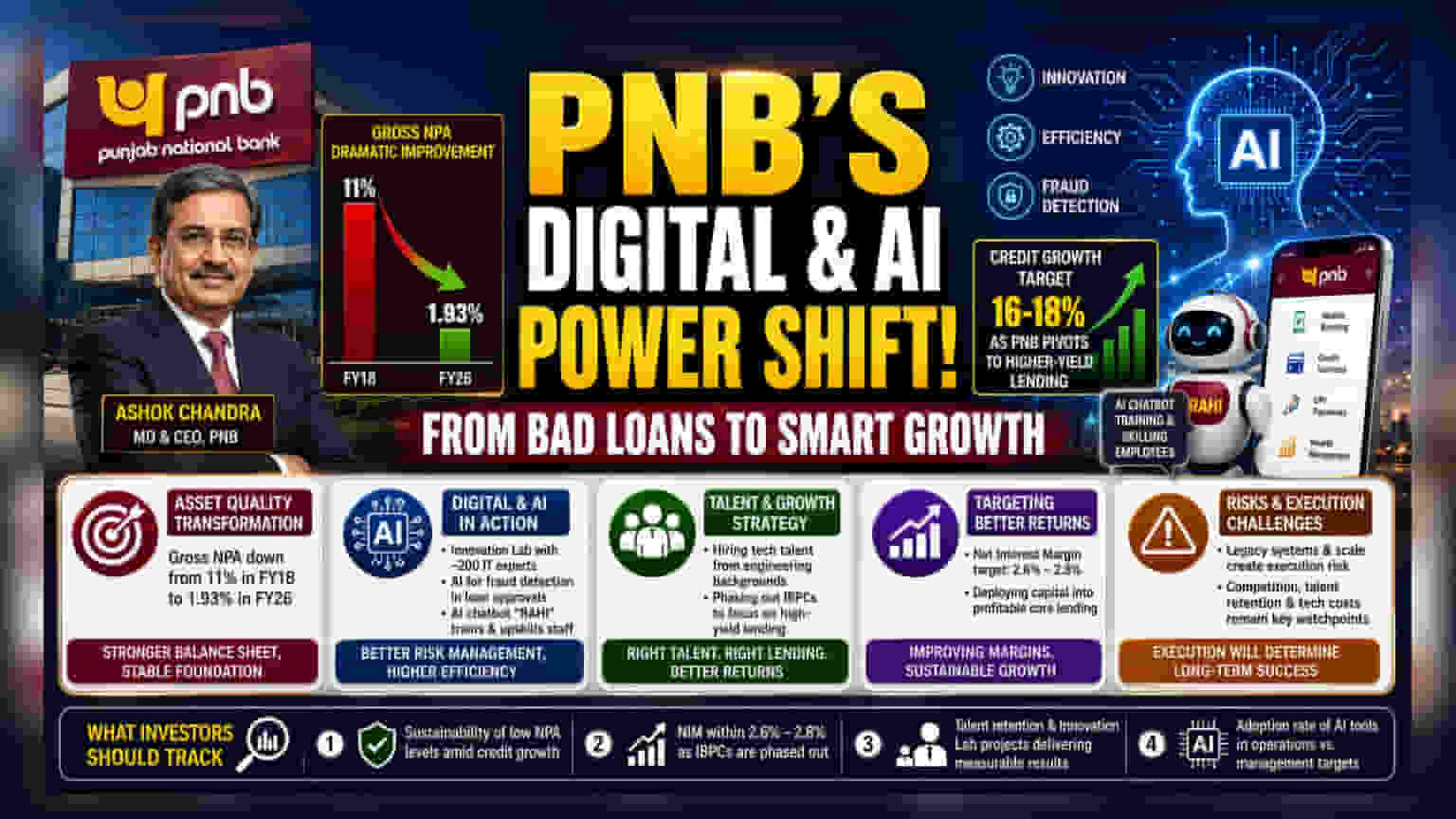

Punjab National Bank is shifting its focus toward artificial intelligence and digital processes to boost growth and efficiency. Under CEO Ashok Chandra, the bank has significantly reduced its bad loans, moving from 11% in FY18 to 1.93% by FY26. PNB is now targeting 16-18% credit growth by moving away from lower-yield certificates and focusing on core lending. For investors, the bank’s push to recruit engineering talent and use AI for fraud detection marks a change in how a traditional public sector lender plans to compete in a tech-driven banking environment.

What Happened

Punjab National Bank (PNB) has announced a strategic shift towards heavy digitalization and artificial intelligence (AI) adoption. Under the leadership of MD & CEO Ashok Chandra, the bank is integrating new technology across its operations, from fraud detection to internal training. The bank also reported a major reduction in its gross non-performing assets (NPAs)—a key measure of bad loans—which dropped from 11% in FY18 to 1.93% by FY26. PNB has stated it is targeting credit growth of 16-18% as it pivots its strategy toward higher-yield lending.

The Asset Quality Transformation

The most significant change for PNB has been the cleaning up of its balance sheet. Reducing gross bad loans from 11% to 1.93% over eight years is a substantial move for a large public sector lender. This indicates that the bank has moved past the legacy asset quality issues that once weighed heavily on its financial performance. For investors, this lower NPA level creates a more stable foundation for the bank to expand its lending book without the immediate pressure of managing old, stressed accounts.

Why Digitalization and AI Matter

PNB is using technology to solve two core banking challenges: efficiency and risk management. The bank has set up an "Innovation Lab" with roughly 200 young IT professionals to work on AI tools. This is a direct attempt to modernize operations. Practically, this involves using AI to improve fraud detection during the loan approval process, which can help prevent future bad loans. The bank is also using an AI-based chatbot, "RAHI," to train employees, assess their skills, and standardize product knowledge across its vast branch network. These measures are designed to help the bank operate with the agility typically associated with private sector lenders.

The Talent and Growth Shift

Traditionally, public sector banks have faced challenges in attracting specialized tech talent. PNB is addressing this by hiring from engineering backgrounds, with a significant portion of its management trainees now holding technical degrees. The bank aims to use this talent to accelerate its growth. A key part of this plan involves phasing out investments in lower-yield interbank participatory certificates (IBPCs). By moving away from these, PNB intends to deploy capital into more profitable core lending areas, aiming for a net interest margin (the difference between what it earns on loans and pays on deposits) toward the upper end of its 2.6%-2.8% guidance.

Risks and Execution Challenges

While the technology push is positive, investors should be aware of the inherent risks. Public sector banks often face hurdles in decision-making speed and recruitment flexibility compared to private peers. Integrating advanced AI and agentic AI systems across a massive, legacy-heavy branch network is complex and carries execution risk. If the technology adoption is slower than expected or if the cost of implementation does not lead to measurable efficiency gains, it could put pressure on the bank's profitability. Additionally, the banking sector remains competitive, and PNB must ensure its digital services remain attractive to customers who have many choices.

What Investors Should Track

Going forward, the key indicators for investors will be the sustainability of this credit growth and the actual impact of tech spending on the bank's bottom line. Investors may track the following:

- Success in maintaining the low NPA levels as the bank pursues aggressive credit growth.

- Whether the net interest margins can stay within the 2.6%-2.8% target as the bank phases out IBPCs.

- The bank's ability to retain its young IT talent and successfully scale its Innovation Lab projects to tangible revenue or cost-saving outcomes.

- Quarterly updates on the actual adoption rate of AI tools in day-to-day operations versus management's targets.