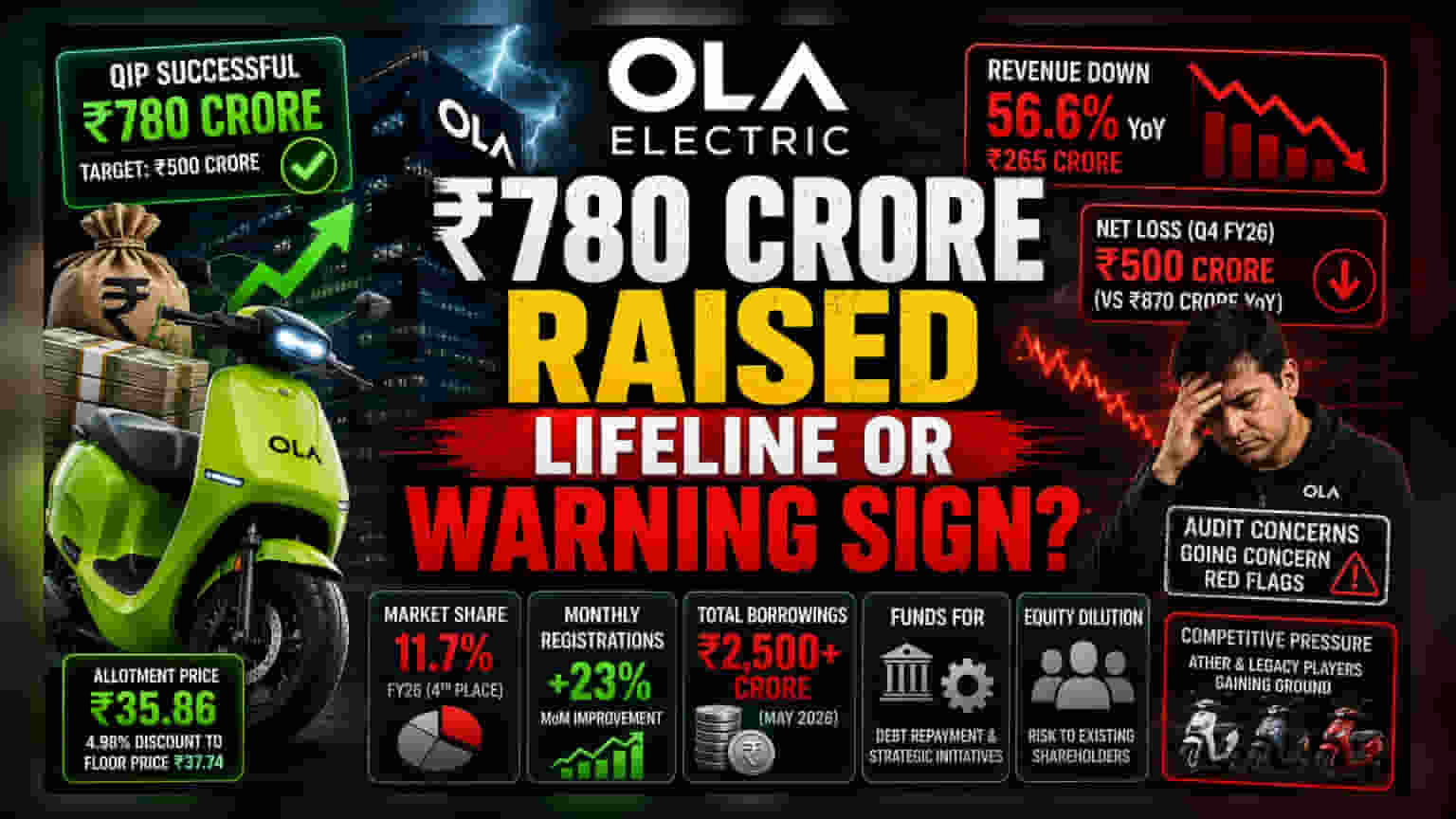

The Capital Infusion

Ola Electric Mobility has officially concluded its Qualified Institutions Placement (QIP), securing Rs 780 crore—well above its initial Rs 500 crore target. The transaction involved the allotment of 217.58 million equity shares to institutional buyers at Rs 35.86 per share, a 4.98% discount to the SEBI-mandated floor price of Rs 37.74. While the raise successfully bolstered the balance sheet, the pricing reflects a cautious market reception, trailing significantly behind the company's valuation at the time of its initial public offering.

The Operational Reality

This fundraising comes as the company navigates a volatile transition period. Financial disclosures for the quarter ending March 31, 2026, reveal a consolidated net loss of Rs 500 crore, narrowing from Rs 870 crore in the previous year but highlighting persistent profitability hurdles. Perhaps more pressing is the 56.6% year-on-year revenue contraction, which fell to Rs 265 crore. The capital is designated for debt repayment and strategic initiatives, essentially functioning as a bridge for a firm attempting to regain its footing as growth momentum has visibly decelerated.

Competitive Erosion

Once the undisputed leader in India’s electric two-wheeler market, the company has seen its market share slip to approximately 11.7% in FY26, relegating it to fourth place. Legacy automotive incumbents and nimble rivals like Ather Energy have aggressively gained ground by leveraging superior distribution networks and more stable customer support structures. While recent monthly registration data shows a 23% month-on-month improvement, the company remains under pressure to convert these registrations into sustained, profitable revenue growth in a market now favoring established, broad-based automotive players.

The Forensic Bear Case

From a risk-averse perspective, several red flags persist. Beyond the obvious equity dilution for current shareholders, the company faces scrutiny over its long-term financial viability. Audit reports have previously flagged concerns regarding inventory control, audit-trail integrity, and the company's status as a going concern. Furthermore, the broader sentiment around Bhavish Aggarwal’s entities has soured, exacerbated by recent massive valuation markdowns in the ride-hailing arm (Ola Consumer) by global asset managers. With total borrowings for the firm and its subsidiaries exceeding Rs 2,500 crore as of May 2026, the company is effectively utilizing high-cost capital to manage a debt-heavy structure while operating in a capital-intensive sector that shows no signs of slowing its competitive intensity.