Nomura expects Indian banks to see a 12% rise in operating profit for the June quarter, though net interest margins may face mild pressure. While loan growth remains robust, higher credit costs are expected to limit overall profit growth to 6% year-on-year. Investors should note that deposit growth continues to lag behind credit growth across the sector.

As India's banking sector prepares for the June quarter (Q1FY27) earnings season, brokerage firm Nomura has released its expectations, highlighting a mix of resilient loan demand and potential margin challenges. The report forecasts a 12% year-on-year increase in core pre-provision operating profit, supported by a 9% rise in net interest income and disciplined control over operating expenses. However, the anticipated growth in profit after tax is more modest at 6%, primarily due to seasonally higher credit costs that are expected to weigh on the bottom line.

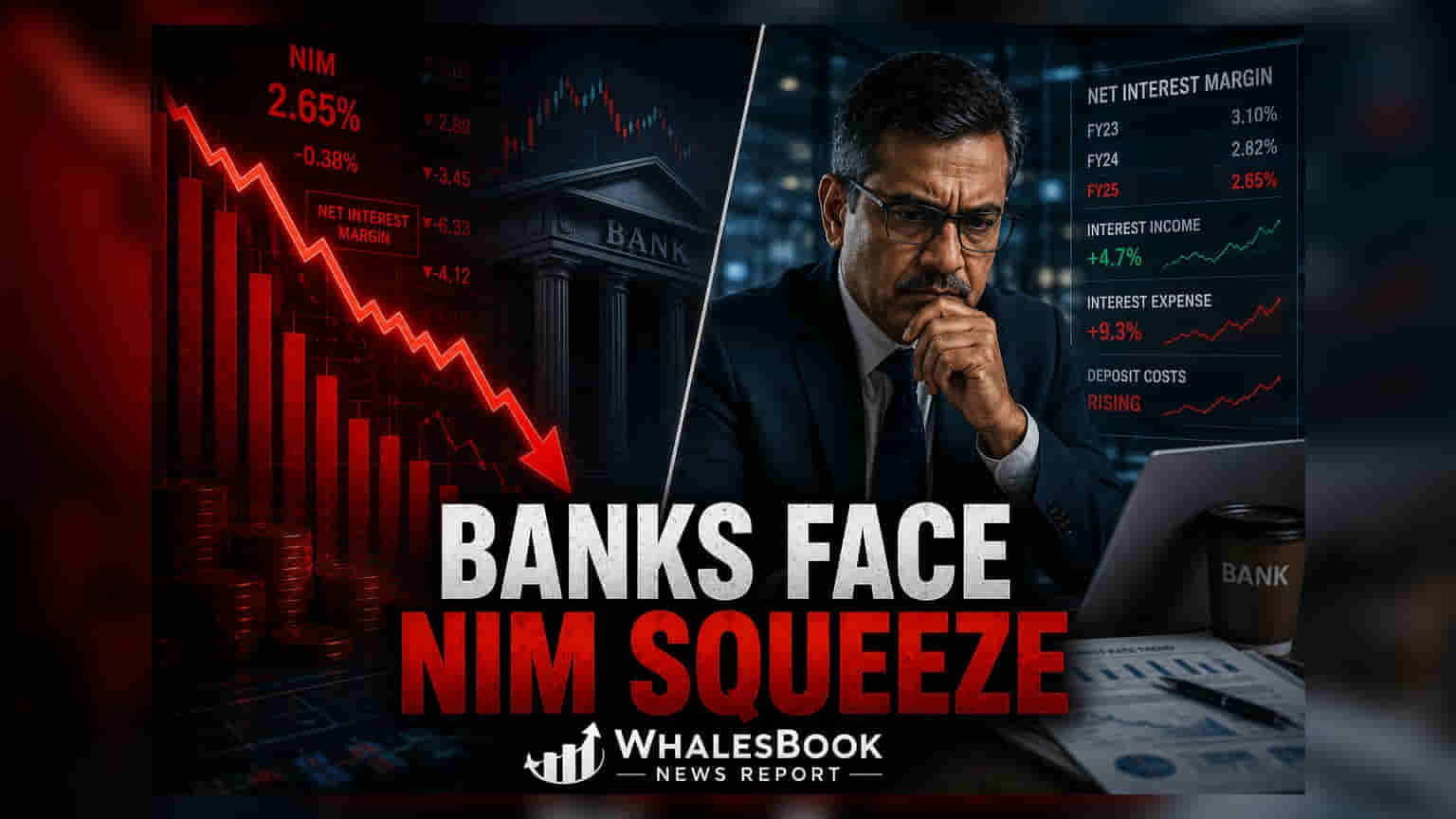

Margin Dynamics and Sector Variation

A key focus for the upcoming results is the performance of net interest margins, or the difference between the interest income earned on loans and the interest paid on deposits. Nomura expects a mild-to-moderate decline in margins for most lenders, noting that performance will likely depend on individual banks' loan portfolios and their ability to manage liabilities. While Federal Bank is identified as a potential outlier that may avoid this decline, other institutions such as Bank of Baroda and Axis Bank could experience more pronounced pressure. This margin squeeze is largely attributed to the ongoing rise in deposit costs and a strategic shift by some banks toward lower-yielding loan segments.

On the positive side, the banking sector may find some relief from treasury gains. Softer government bond yields are expected to provide a boost to investment portfolios, helping to offset some of the margin pressure. This effect is projected to be more beneficial for public sector banks, which typically carry larger bond portfolios.

Asset Quality and Economic Risks

Asset quality across the sector is currently viewed as stable, with signs of easing stress in segments like unsecured retail loans and microfinance. However, the sector faces a structural funding challenge as deposit growth continues to trail behind credit growth, keeping credit-deposit ratios at elevated levels. Nomura points to the Reserve Bank of India’s recent measures regarding FCNR(B) deposits as a potential stabilizing factor that could help address these funding gaps beginning in the September quarter.

Investors are also advised to monitor the impact of environmental factors. An uneven or delayed monsoon season poses a risk to loan portfolios in rural areas, as well as segments like MSMEs and commercial vehicles, which could face repayment pressure later in the fiscal year.

Sector Picks and Outlook

In its latest assessment, Nomura has updated its top preferences in the banking space, favoring HDFC Bank, ICICI Bank, and Kotak Mahindra Bank. Notably, HDFC Bank has re-entered the brokerage's preferred list, replacing Axis Bank. As the earnings season unfolds, the key monitorable for investors will be how effectively these banks manage their cost of funds and whether they can sustain loan growth momentum despite the broader funding and interest rate environment.