The National Pension System (NPS) has introduced the Retirement Income Scheme (RIS), offering retirees new ways to access their corpus through Systematic Payout Rate (SPR) and Systematic Unit Redemption (SUR). These options allow retirees to keep their savings invested for potential market-linked growth while receiving periodic income, providing an alternative to traditional annuities.

What Happened

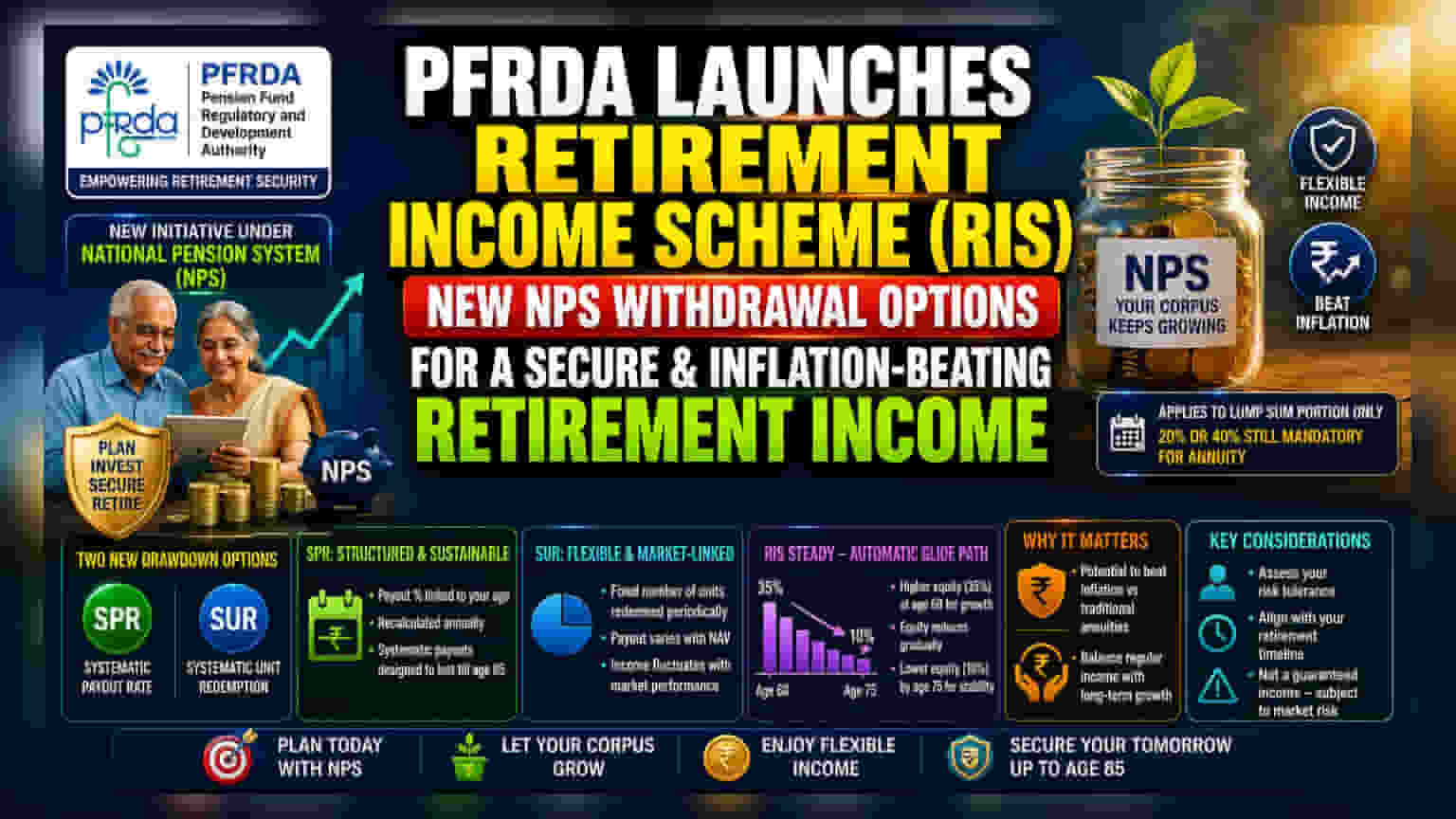

The Pension Fund Regulatory and Development Authority (PFRDA) has launched the Retirement Income Scheme (RIS) under the National Pension System (NPS). This new framework introduces two specific drawdown options—Systematic Payout Rate (SPR) and Systematic Unit Redemption (SUR)—to help retirees manage their corpus more effectively after age 60.

Previously, NPS subscribers had limited options for the portion of their corpus eligible for lump-sum withdrawal: taking it as a one-time payment or through Systematic Lump-sum Withdrawal (SLW). The new RIS options allow subscribers to leave a larger part of their savings invested in the NPS after retirement, potentially aiming for long-term market-linked growth instead of withdrawing it all at once.

How SPR and SUR Work

The RIS offers two distinct ways to receive periodic payouts from the NPS corpus:

- Systematic Payout Rate (SPR): This is designed for those seeking a more structured income. The payout percentage is linked to the subscriber's current age. The system recalculates the payout annually, adjusting it to ensure the corpus is spread out systematically, aiming for longevity up to age 85.

- Systematic Unit Redemption (SUR): This option focuses on redeeming a fixed number of units periodically. Since the number of units is fixed, the actual amount received each month, quarter, or year will fluctuate based on the Net Asset Value (NAV) of the underlying NPS funds. This can result in variable income depending on market performance.

Why This Matters for Retirees

For many retirees, the primary challenge is balancing regular cash flow with the need to beat inflation. Traditional annuities provide a guaranteed, fixed income for life but often struggle to outpace rising costs over 20-25 years.

The new RIS options provide a middle path. By keeping the corpus invested, retirees may benefit from potential equity and market-linked returns. This could offer a better hedge against inflation compared to fixed-income products. However, unlike an annuity, these payouts are not guaranteed.

Managing Market Risk: The RIS Steady Glide Path

To manage the volatility inherent in market-linked investments, the RIS framework utilizes a specific fund called "RIS Steady." This fund automatically adjusts the asset mix as the retiree ages, a process known as a glide path.

At age 60, the equity exposure is set higher (around 35%) to capture potential growth. As the subscriber grows older, the system automatically reduces equity exposure and increases the allocation to safer assets like government securities. For example, equity exposure is designed to step down gradually, reaching a lower level (around 10%) by age 75. This helps reduce the impact of market crashes as the retiree approaches the later stages of the withdrawal period.

What Investors Should Track

Investors considering these new options should note that these are not substitutes for mandatory annuity purchases. The rules requiring a portion of the corpus (20% or 40%, depending on the exit conditions) to be invested in an annuity remain unchanged. The new RIS drawdown options only apply to the remaining lump-sum portion.

When evaluating these options, it is important to consider:

- Risk Tolerance: Since SUR payouts depend on NAV, subscribers comfortable with market fluctuations may prefer it, whereas those seeking a more calculated, sustainable drawdown might find SPR more suitable.

- Corpus Longevity: The RIS is structured to last up to age 85. Investors should assess whether this timeline aligns with their personal retirement planning needs.

- No Guarantee: Unlike an annuity, which provides a fixed monthly pension for life, the RIS is subject to market risks. If the underlying investments perform poorly over a long period, the actual payouts or the residual corpus may be lower than expected.