NPCI has partnered with HSBC India to enable real-time foreign exchange settlement for cross-border UPI payments. This integration allows Indian travelers to see the exact cost of international purchases in Indian Rupees at the point of sale, removing ambiguity in currency conversion rates. The move aims to boost UPI's global adoption by competing with traditional card networks.

What Happened

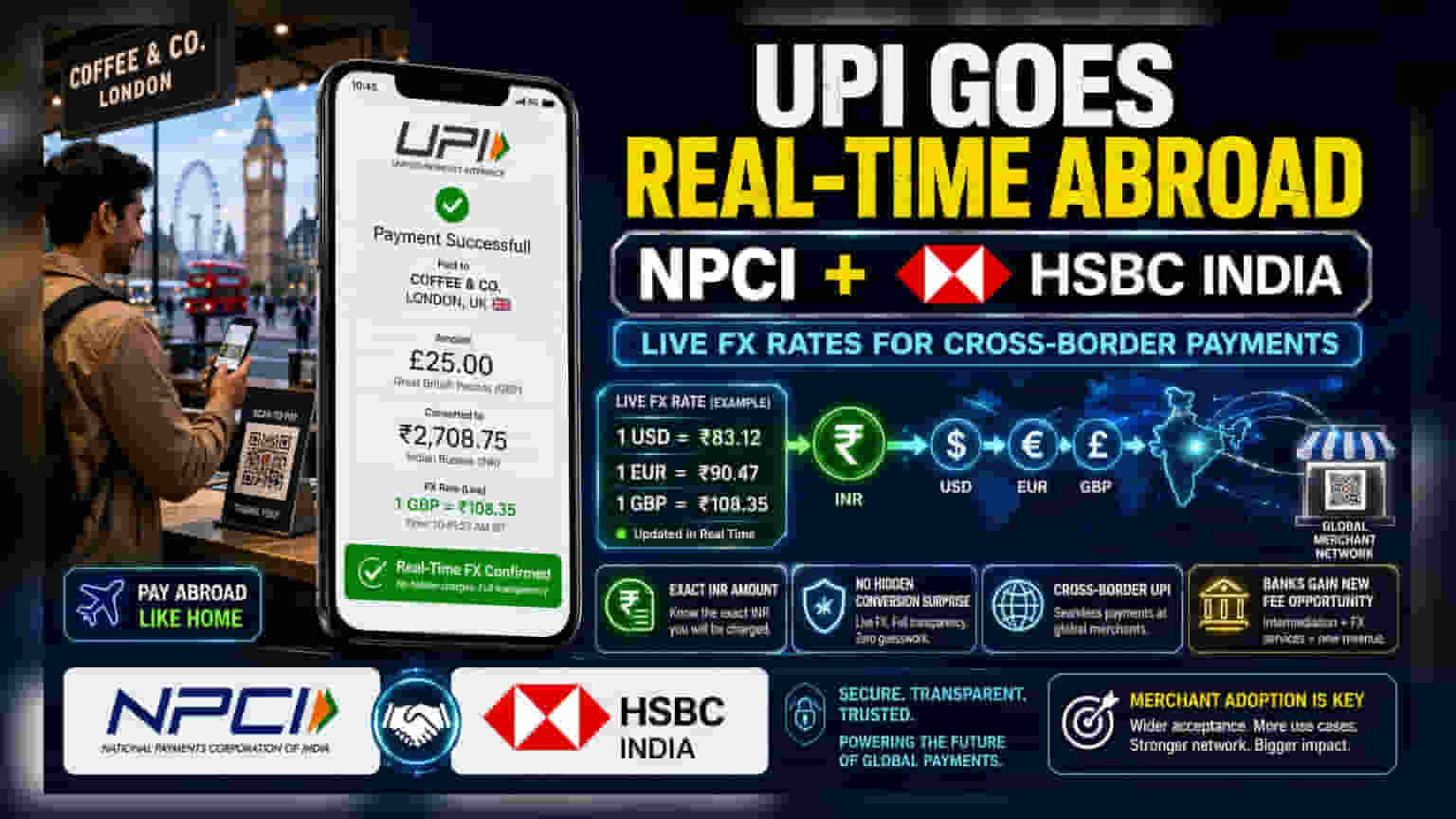

The National Payments Corporation of India (NPCI) has entered into a collaboration with HSBC India to introduce real-time foreign exchange (FX) settlement for cross-border transactions made using the Unified Payments Interface (UPI). By using HSBC India’s infrastructure and API connectivity, the system will now provide travelers with the precise conversion rate and the final cost in Indian Rupees (INR) at the exact moment of a purchase abroad.

Why This Matters For Transparency

Traditionally, international payments made via debit or credit cards often involve a delay in conversion, with the final amount in rupees sometimes differing from what was expected due to fluctuating exchange rates and hidden conversion fees. By integrating real-time FX settlement, this partnership aims to remove this uncertainty. When an Indian user scans a QR code at a participating merchant abroad, they will see the exact INR amount they are paying, rather than finding out the final cost later when the bank processes the transaction.

The Banking Opportunity

For banks like HSBC and other potential partner institutions, this development opens a new channel for fee-based income. Managing cross-border payments is a complex business, and by acting as the banking partner for these settlements, banks can secure a role in the growing digital payment ecosystem. As UPI expands into more countries, the ability to facilitate these transactions efficiently could become a differentiating factor for banks looking to capture volume in the travel and retail payments sector.

Challenges In Cross-Border Payments

While the technology promises convenience, the expansion of UPI internationally faces inherent business challenges. The most significant is the regulatory landscape in foreign countries. Every nation has its own financial data privacy laws, central bank regulations, and anti-money laundering requirements. A model that works in one country may require complex adjustments to comply with local laws in another. Additionally, UPI is a direct competitor to established global card networks like Visa and Mastercard, which currently dominate cross-border retail payments. Success for this initiative will depend on how quickly these payment rails can gain acceptance among local merchants in foreign markets who are accustomed to traditional card or cash payments.

What To Watch Next

Investors and market observers will likely track the scale of merchant adoption, as the utility of this service depends entirely on whether foreign retailers accept UPI. Furthermore, the pace at which the NPCI adds more banking partners for similar FX integrations will be a key signal of how fast this system is scaling. Other monitorables include the competitive reaction from traditional card networks and whether this real-time transparency model leads to a shift in consumer behavior for international spending.