Non-banking financial companies have overtaken banks in new housing and vehicle loan growth between March and May 2026. This shift occurs as banks turn cautious, facing deposit mobilization challenges while NBFCs leverage specialized lending models.

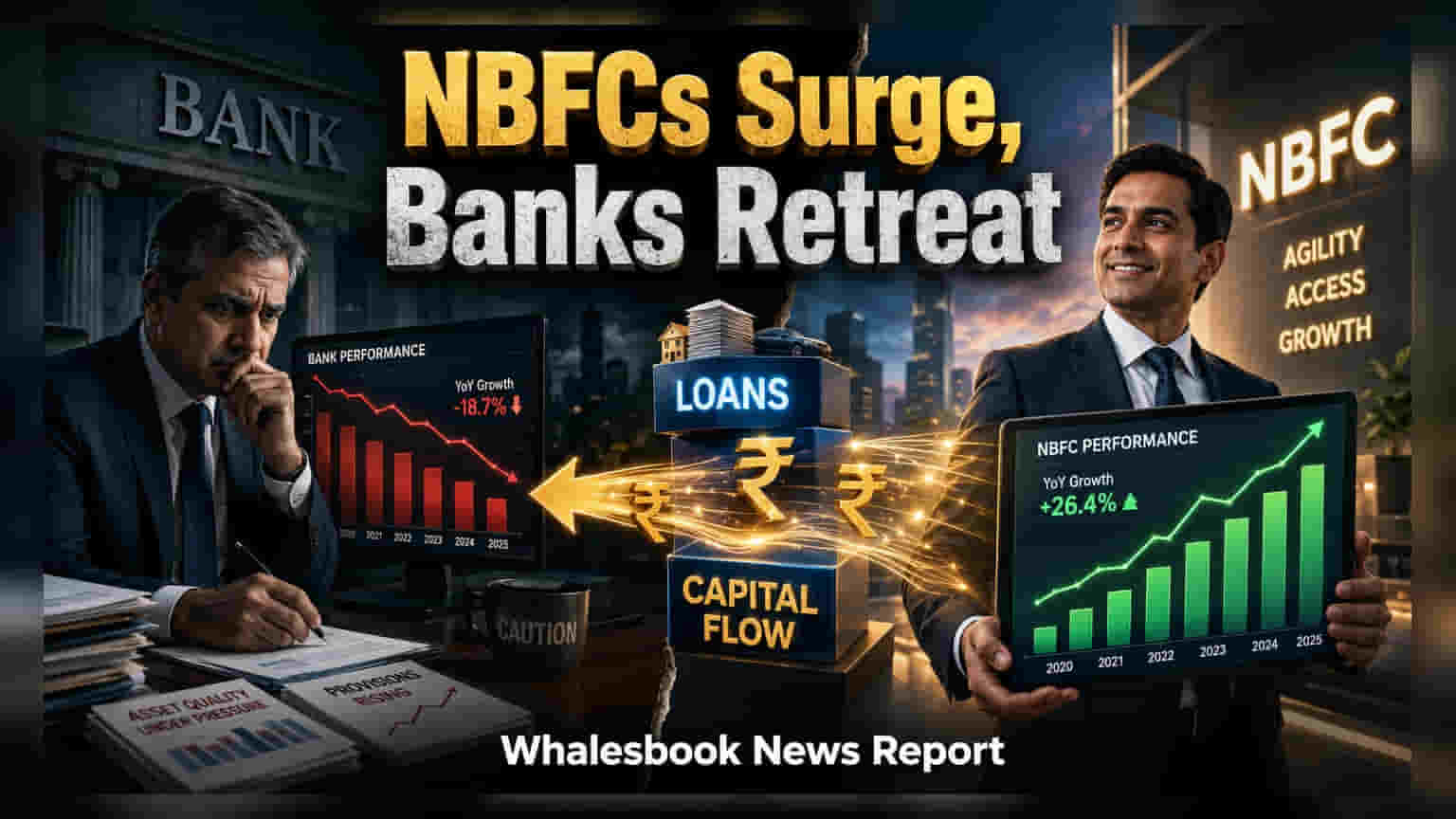

Non-banking financial companies (NBFCs) are increasingly capturing market share in retail lending as traditional banks adopt a more conservative approach. According to recent data from the Reserve Bank of India (RBI), covering a sample of approximately 87% of the non-bank loan system, NBFCs outperformed banks in key lending areas between the end of March and May 2026.

In the housing loan segment, NBFCs extended ₹13,413 crore in new credit, exceeding the ₹13,072 crore provided by banks. The difference was more significant in the vehicle and consumer durable sectors. NBFCs recorded a ₹13,840 crore increase in vehicle loans and a ₹9,991 crore rise in consumer durable financing during the two-month period. In comparison, banks saw their vehicle loan portfolio grow by ₹9,772 crore, while their consumer durable financing rose by only ₹944 crore.

Strategic Differences in Lending Focus

The divergence in growth patterns is largely attributed to the distinct operational models of the two sectors. Banks, which manage a massive loan book of approximately ₹215 trillion, often face constraints related to deposit growth, leading them to prioritize lower-risk, lower-yield segments such as home loans for prime borrowers. Consequently, banks have shown more caution in sectors that require higher operational intensity or cater to profiles that fall outside standard risk parameters.

In contrast, NBFCs operate with focused business models. Many non-banks specialize in specific product categories like auto finance or mortgage lending. This specialization allows them to develop deeper expertise in assessing borrowers who may not have traditional credit histories. Furthermore, the decentralized structure of many NBFCs, which empowers local vertical heads to make credit decisions, enables these firms to respond more quickly to emerging demand compared to the more centralized decision-making processes often found in large banking institutions.

Risks and Future Monitoring

While this growth highlights the increasing importance of non-banks in formalizing credit access, investors should track several factors that influence the sustainability of this trend. A primary monitorable for the NBFC sector is the cost of liquidity. Although liquidity remains available, the cost of funds has been a recurring challenge for these firms in recent quarters. Any tightening of financial conditions could pressure the interest margins that NBFCs earn on these retail loans.

Additionally, while analysts at firms like Motilal Oswal note that NBFCs have cleaned up their balance sheets following past asset quality issues, their performance remains sensitive to economic cycles. Unlike banks, which benefit from a stable base of low-cost deposits, NBFCs rely more heavily on market borrowings, making them more vulnerable to shifts in interest rates. Investors will likely look for future updates on how these firms manage their cost of funds and maintain asset quality as their retail loan portfolios expand.