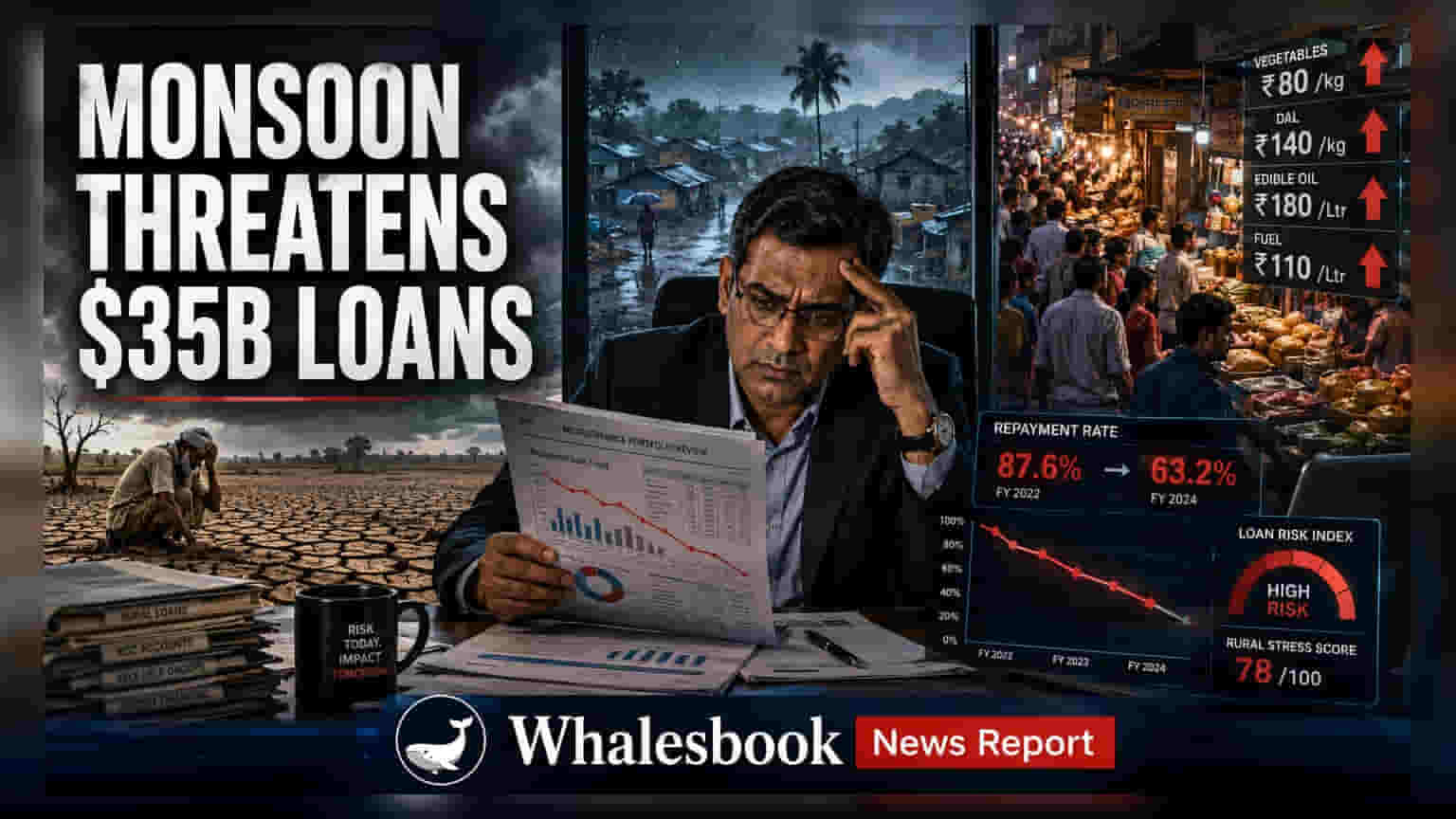

India’s $35 billion microfinance industry is facing fresh repayment concerns as poor monsoon forecasts and high inflation pressure rural household incomes. Lenders like Bandhan Bank and CreditAccess Grameen, which rely heavily on rural borrowers, may see rising loan defaults. Investors are closely watching how these institutions manage debt levels among borrowers who have taken loans from multiple sources.

The Indian microfinance sector, which serves as a critical credit lifeline for rural households, is encountering new challenges that could impact asset quality. With a loan portfolio totaling approximately $35 billion, the industry is sensitive to rural economic health, which is currently under pressure from a combination of uneven rainfall and sustained price increases for essential goods.

Impact on Rural Repayment Capacity

Microfinance institutions typically generate about 80% of their business from rural markets, often supporting agricultural and small-scale livestock activities. A weak monsoon directly threatens farm yields, which reduces the immediate income of many borrowers. When coupled with the rising cost of fuel and fertilizers, rural families have less disposable income to meet their monthly loan obligations. This creates a direct link between climatic conditions and the ability of these institutions to collect payments on time.

Debt Concentration and Borrower Stress

Data from rating agencies suggests that borrowers who hold loans from multiple lenders are at a higher risk of default. Approximately 20% of the microfinance customer base currently carries debt from more than one source. This concentration of debt makes these individuals particularly vulnerable to any sudden drop in income. As these households struggle to manage multiple payments simultaneously, lenders often see a rise in delinquency rates, which is when borrowers fail to pay on time.

Exposure of Key Lenders

Several listed lenders have significant exposure to this segment. For instance, as of the end of March, Bandhan Bank held 23% of its total loan book in micro-lending products. Other entities such as CreditAccess Grameen, Satin Creditcare Network, and Muthoot Microfin also maintain large portfolios in this space. These companies had previously tightened their loan approval processes following past periods of stress, which helped them recover and expand credit during early 2024. However, the current macroeconomic environment is testing the effectiveness of these stricter standards.

Future Monitorables for Investors

Investors in this space may want to track the trend of non-performing loans, or bad loans, in the upcoming quarterly results. The ability of these banks and financial companies to maintain their profit margins will depend on how effectively they manage credit costs while keeping loan growth steady. Additionally, any updates from the Reserve Bank of India regarding sector-specific lending guidelines or credit quality checks will be important to observe, as regulatory oversight often increases during periods of potential financial stress in the micro-lending industry.