A recent Crisil report highlights that microfinance institutions are dealing with tougher loan repayments caused by inflation and rural income volatility. While state-level regulations in areas like Karnataka have hurt collections, lenders are seeing better portfolio quality from tighter new-loan standards.

What Happened

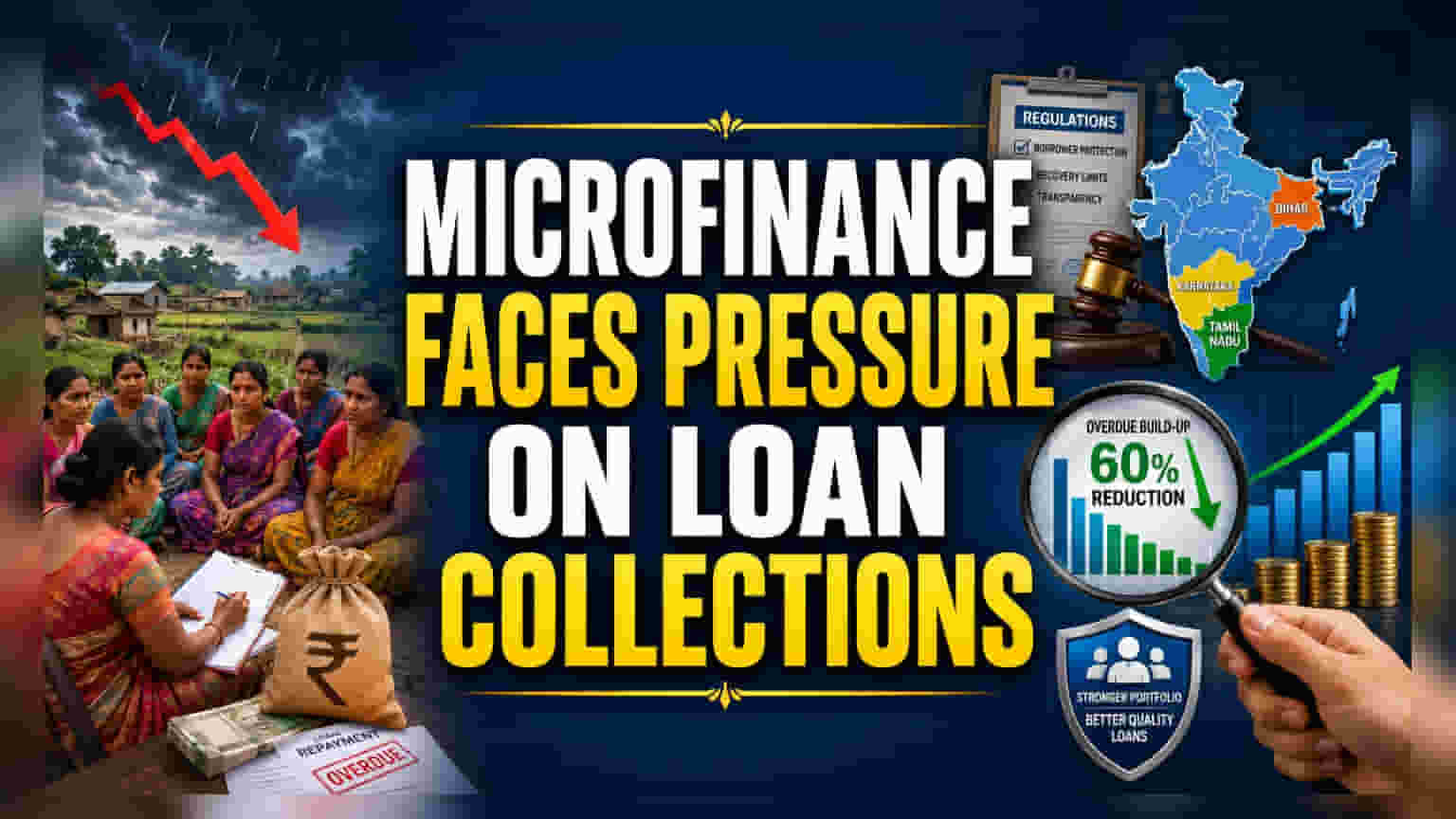

The microfinance sector is facing renewed pressure on loan collections, according to a recent report by credit rating agency Crisil. Rising inflation and unpredictable rural incomes—partly due to weather patterns—are making it harder for some borrowers to manage their repayments. Additionally, stricter state-level regulations, particularly in regions like Karnataka, have added layers of complexity to how lenders collect money from their clients, impacting operational efficiency.

The Regulatory and Regional Hurdle

Regulatory changes have become a significant focus for microfinance lenders. States including Karnataka, Tamil Nadu, and Bihar have implemented tighter rules to protect borrowers, which include stricter limits on how lenders can recover their money. The impact was immediately visible in Karnataka, where collection efficiency—the percentage of total expected loan payments actually received—dropped by 5-6% shortly after the state’s microfinance ordinance took effect in February 2025.

While lenders in Tamil Nadu and Bihar have largely adapted their operational styles to avoid similar sharp declines, the Karnataka experience serves as a reminder of how state-specific rules can suddenly disrupt local operations. When combined with the broader issue of borrowers having less cash to spare due to inflation, these regulatory shifts create an environment where lenders must be more careful.

Improving Loan Quality

Despite these headwinds, the sector shows signs of better risk management. Lenders have begun applying tighter rules for issuing new loans, often referred to as "guardrails." This strategy appears to be working. Data from securitized loan pools—loans bundled together and sold to investors—reveals a positive trend: there has been a 60% reduction in the buildup of overdue payments for loans issued after these tighter standards were put in place.

This trend suggests that microfinance institutions are becoming more selective. By limiting loans to borrowers who are already carrying too much debt and focusing on better-quality portfolios, lenders are attempting to build a cushion against potential economic stress.

What Investors Should Track Next

The key monitorable for investors is how microfinance companies manage their "asset quality" in the face of these combined pressures. Investors may track management commentary in upcoming quarterly results regarding three specific areas:

Geographic Exposure: Does the company have a high concentration of business in states with strict or evolving regulatory frameworks?

Collection Trends: Is there stability in the collection efficiency numbers despite the pressure from inflation?

Underwriting Standards: Are the companies continuing to prioritize the quality of new loans over the sheer speed of growth?

Monitoring these factors will help determine if the shift toward more cautious, high-quality lending will effectively protect profit margins from the risk of rising bad loans.