LIC Housing Finance (LICHFL) is projecting a rebound in its Assets Under Management (AUM) growth to 10% in FY27, aiming for an upswing driven by a renewed focus on retail lending and specialized business units. This optimistic outlook contrasts with immediate financial results showing declining total income and squeezed profit margins, painting a mixed picture of the company's near-term prospects.

Analysts expect LICHFL's AUM growth to reach 10% in FY27 and 9% in FY28. Key drivers include increased retail loan originations, expanded third-party sourcing, co-lending partnerships, and a dedicated affordable housing unit. The company is also hiring approximately 200 new staff to boost loan origination capacity. This strategy aims to accelerate loan book growth, which stood at 4.4% year-on-year to ₹3,161.7 billion in the last reported quarter, despite a 9.7% rise in disbursements.

For the fourth quarter of FY26, LICHFL reported a 9% increase in net profit to ₹1,497 crore. However, total income slightly decreased to ₹7,195 crore from ₹7,283 crore in the same period last year, highlighting the challenge of translating loan originations into higher top-line revenue growth.

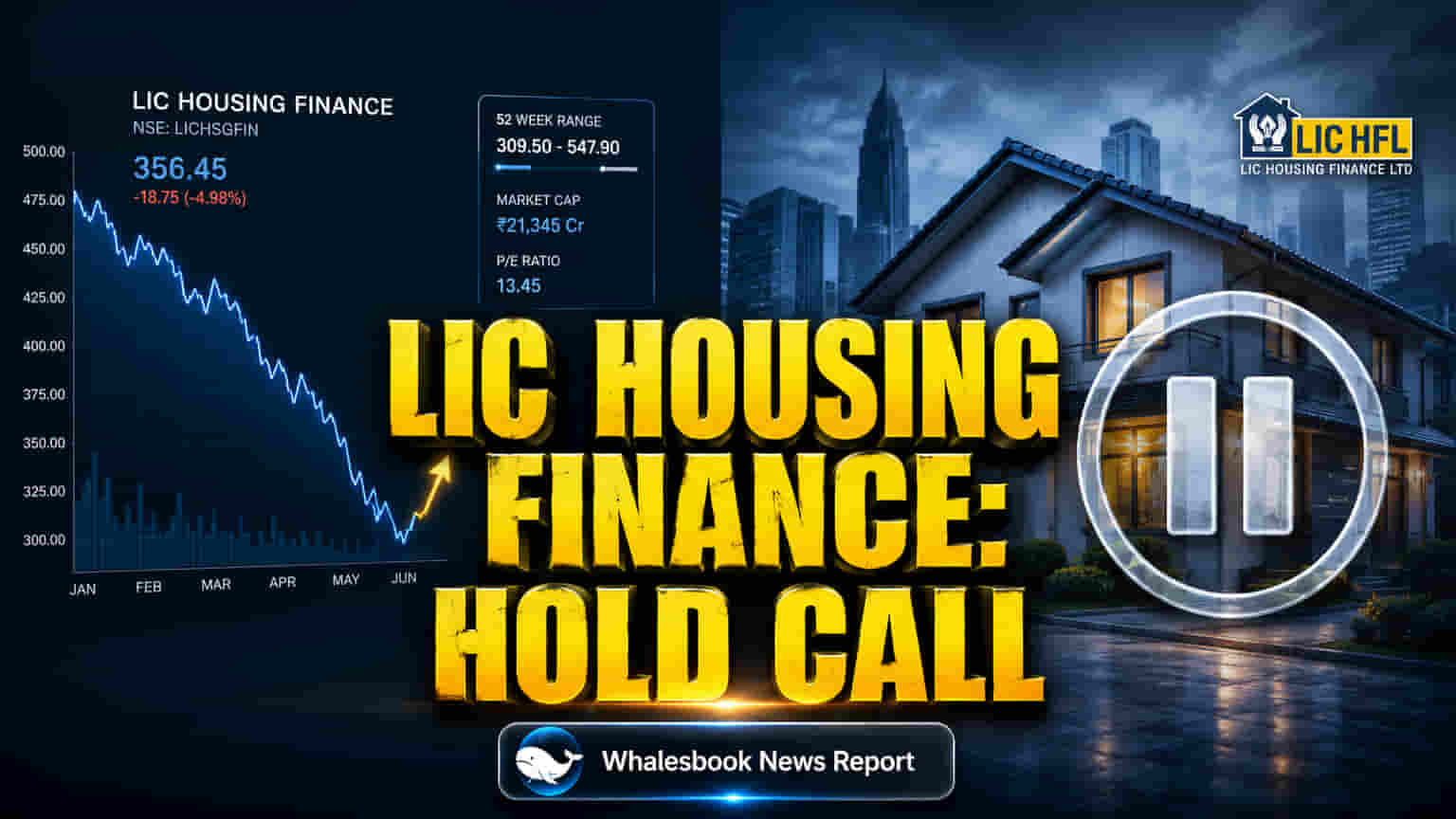

LICHFL's market capitalization is currently between ₹30,500 crore and ₹30,800 crore. Its Price-to-Earnings (P/E) ratio, trading between 5.3x and 5.9x historically, is significantly lower than competitors such as Bajaj Housing Finance (over 27x P/E) and PNB Housing Finance (around 12.1x P/E). Despite a strong Return on Equity (ROE) of 14-16%, LICHFL's price-to-book (P/B) ratio of about 0.8x indicates investor caution. This lower valuation, partly due to high leverage, appears substantial given its steady profitability and strong institutional backing. The broader Indian housing finance market is expanding rapidly, projected to grow from USD 430.74 billion in 2026 to USD 809.07 billion by 2031, driven by urbanization and government support. NBFCs, including housing finance companies (HFCs), are growing faster than public sector banks in this expanding market.

Analysts anticipate pressure on Net Interest Margins (NIMs) as funding costs rise. NIMs are expected to decrease by 6 basis points in FY27 and 18 basis points in FY28, with potential interest rate hikes adding risk. LICHFL's NIM for Q4 FY26 was 2.80%, down from previous periods where it ranged between 2.62% and 3.1%. These margins face pressure from increasing borrowing expenses, a situation made worse by LICHFL's high leverage. The company's Debt-to-Equity ratio is around 7.08x to 7.44x, far above the peer average of 3-4.5x. This high debt level magnifies the effect of higher borrowing costs on earnings.

The housing finance sector is benefiting from government backing for affordable housing, advancements in digital lending, and expansion into smaller cities. Programs like PMAY-Urban 2.0 are helping lower monthly loan payments and increase homeownership access. While this strong demand provides an opportunity for LICHFL, the company must still manage competitive pricing and funding challenges.

Skepticism regarding LICHFL's projected AUM growth stems partly from its high leverage. The company's Debt-to-Equity ratio, near 7.44x, makes it more vulnerable to interest rate changes and potential financial strain if funding costs rise or asset quality worsens. This leverage, along with past NIM compression, likely contributes to the market's low valuation multiples. Investors also point to the departure of the General Manager (Marketing) in April 2026 as potentially raising questions about customer acquisition strategies. The company's stock performance has also lagged, falling 1.84% in 2026 and 12.60% in 2025 while the broader sector gained.

Analysts hold a mixed view on LICHFL's prospects. While one firm rates it 'Hold' with a ₹575 target, the general consensus recommendation is 'Buy', with price targets ranging from ₹578.17 to ₹626.52, suggesting potential upside. Some analysts also expect dividend increases. The company's strategy to focus on the prime salaried segment and expand its digital channel via the HomY app is intended to improve asset quality and customer acquisition. Future growth will depend on LICHFL's ability to manage funding costs, leverage its parent company's support, and maintain asset quality in a competitive housing finance market.