The board of Krishna Institute of Medical Sciences (KIMS) has approved a ₹600 crore preferential issue of warrants to its promoters. This move helps the hospital chain raise funds for expansion while increasing promoter shareholding. We look at the terms, the strategic rationale, and what this means for shareholders.

What Happened

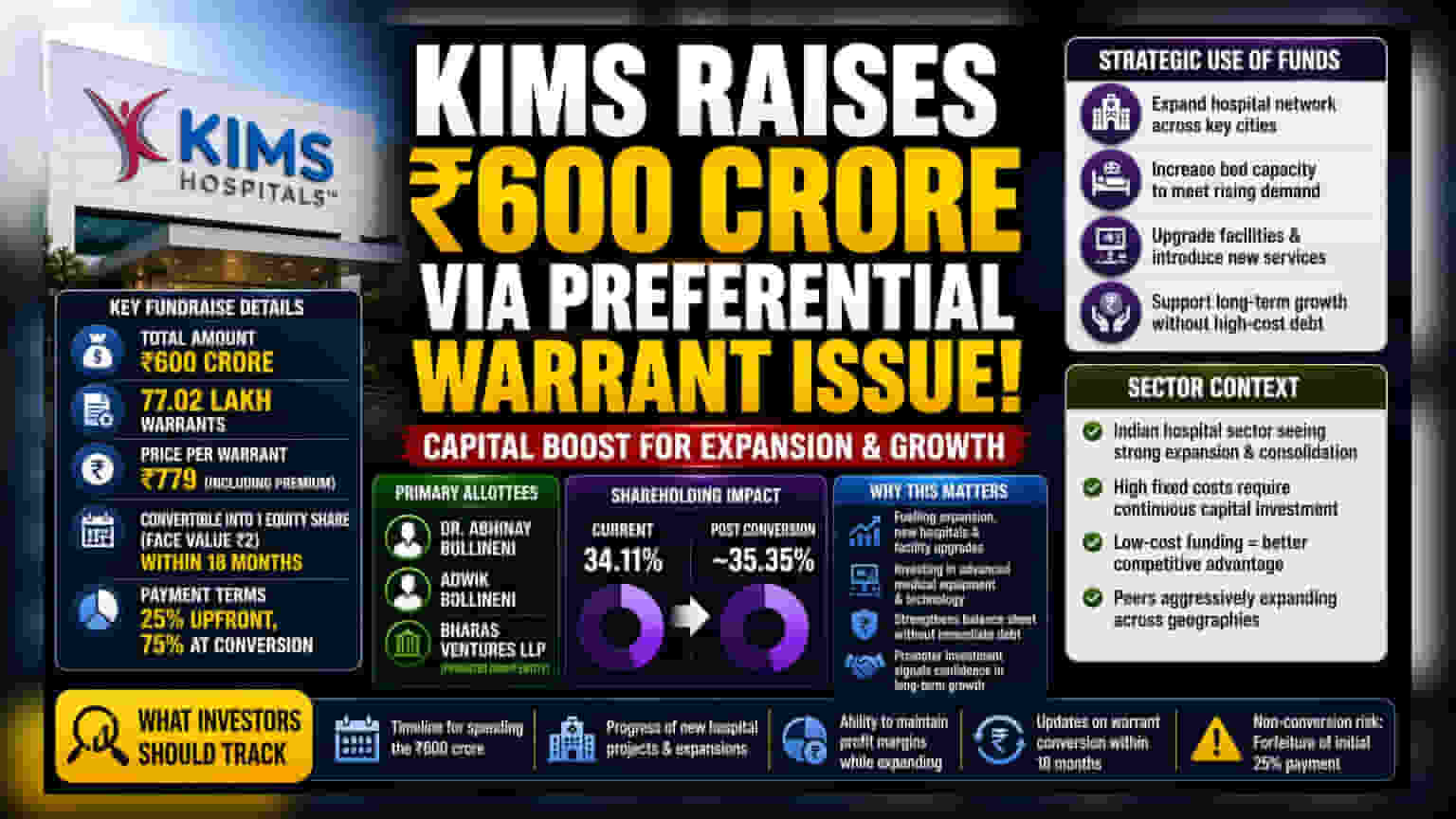

Krishna Institute of Medical Sciences Ltd (KIMS) has received approval from its board to raise ₹600 crore through a preferential issue of warrants. The company will issue 77.02 lakh warrants to its promoters and promoter group. Each warrant is priced at ₹779, which includes a premium, and can be converted into one equity share of face value ₹2 within 18 months from the date of allotment.

Under the terms, the allottees must pay 25% of the total amount upfront, with the remaining 75% due when the warrants are converted into shares. The primary allottees include Dr. Abhinay Bollineni and Adwik Bollineni, along with the promoter group entity Bharas Ventures LLP. Following the full conversion of these warrants, the collective shareholding of the promoter group in the company is expected to increase from the current 34.11% to approximately 35.35%.

Why This Matters for the Business

For a hospital chain like KIMS, this capital infusion serves a strategic purpose. Healthcare businesses are highly capital-intensive, requiring constant investment in new medical equipment, facility upgrades, and the expansion of bed capacity to capture demand in new regions.

By raising money through a preferential issue to promoters, the company secures funds for these growth plans without the immediate burden of interest payments associated with bank debt. This allows the company to maintain a healthier balance sheet while pursuing expansion. Additionally, the decision by promoters to invest ₹600 crore in the company is often viewed by the market as a sign of confidence in the long-term prospects of the business.

The Funding Strategy

This method of fundraising is common in the corporate world when promoters want to demonstrate commitment or when the company needs to bolster its cash reserves for future projects without diluting shares of public investors through a public offering. The 18-month timeline for conversion gives the company flexibility in how and when it brings the capital into the business, allowing it to align the cash inflow with its planned capital spending cycles.

Peer and Sector Context

The Indian hospital sector is currently seeing significant consolidation and expansion as players like Apollo Hospitals, Max Healthcare, and Narayana Health compete for market share. These companies regularly deploy capital to expand into new cities and increase bed count.

Because the hospital business relies on high fixed costs—such as buildings, expensive medical machinery, and staff salaries—the ability to fund expansion cheaply is a key competitive advantage. Companies that can fund growth through internal accruals or promoter support often face less pressure on their profit margins compared to those heavily reliant on high-cost external debt.

What Investors Should Track

While the promoter's infusion is a positive signal for capital availability, investors should monitor how effectively these funds are deployed. The key to long-term value in the hospital sector is the 'gestation period' of new hospitals. When a company builds a new facility, it often takes several years before the new unit reaches its full potential and starts contributing meaningfully to profit margins.

Key monitorables for shareholders include:

- The actual timeline for spending this ₹600 crore.

- The progress of any new hospital projects or expansions funded by this capital.

- The company’s ability to maintain its profit margins while expanding.

- Any future updates on the conversion of these warrants, as failure to convert them within the 18-month window would result in the forfeiture of the initial 25% payment.