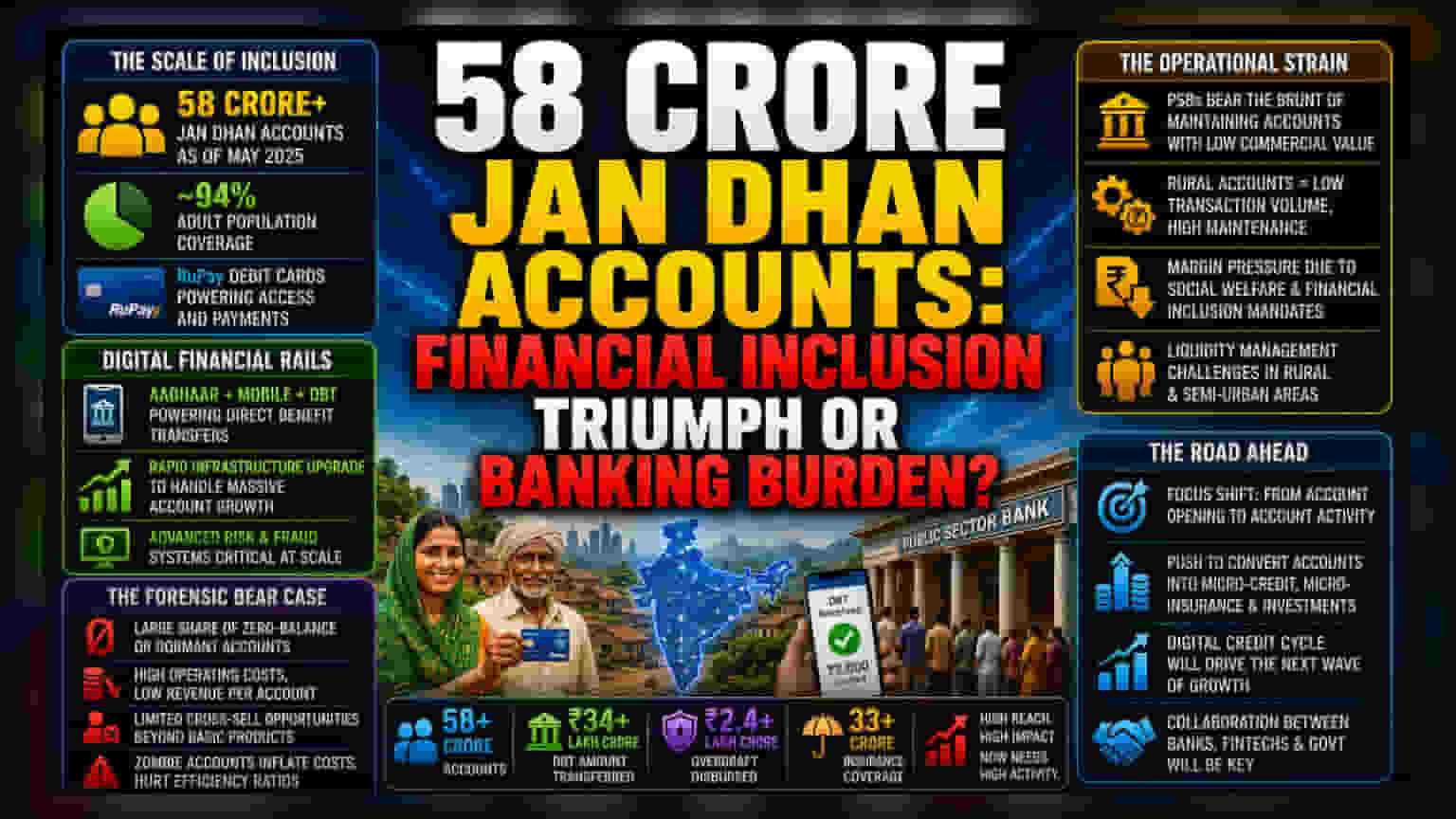

The Operational Strain of Massive Inclusion

Beyond the headline figure of 58 crore accounts lies a complex reality for the Indian banking sector, particularly for public sector banks tasked with maintaining this infrastructure. While the scheme has successfully integrated a massive portion of the population into the formal fold, the proliferation of zero-balance accounts creates a persistent drag on operational resources. Banks are required to support RuPay debit cards, maintain dormant account data, and facilitate frequent direct benefit transfers, often without generating sufficient interest income or fee-based revenue to offset these costs.

Scaling the Digital Financial Infrastructure

The sheer velocity of account growth since 2014 has forced a radical upgrade in India’s digital financial rails. Unlike private sector peers that prioritize high-net-worth individual acquisition, state-run lenders are effectively acting as the utility layer for government social welfare. Data suggests that while account penetration has reached roughly 94% of the adult population, the challenge has shifted from mere account opening to account activity. Managing the liquidity needs of rural depositors while simultaneously scaling the risk management systems required for overdraft facilities creates a unique margin pressure that is seldom reflected in broader market optimism regarding inclusion metrics.

The Forensic Bear Case: Efficiency and Liability

From a institutional risk perspective, the Jan Dhan model carries significant long-term liabilities. Critics point to the high density of rural and semi-urban accounts as a double-edged sword; these regions often lack the transactional volume necessary to make individual accounts profitable. Furthermore, the reliance on the RuPay ecosystem and government-subsidized insurance products limits the ability of banks to cross-sell higher-margin financial products. There is also the persistent risk of 'zombie accounts'—those opened to receive government grants but left otherwise inactive—which inflate administrative costs and skew internal efficiency ratios for large state-run banks. While the government frames this as a triumph of equity, shareholders in major public sector banks must navigate the reality that the bank's balance sheet is increasingly tethered to social welfare mandates rather than purely commercial growth strategies.

Future Outlook and Sector Implications

The trajectory of financial inclusion suggests a pivot toward digitizing the credit cycle for these account holders. Moving forward, the focus will likely shift to how these millions of newly minted banking customers can be transitioned into micro-lending and micro-insurance products. However, until such conversion rates improve, the administrative burden of maintaining the largest account base in the world will continue to act as a weight on the return on assets for the involved financial institutions.