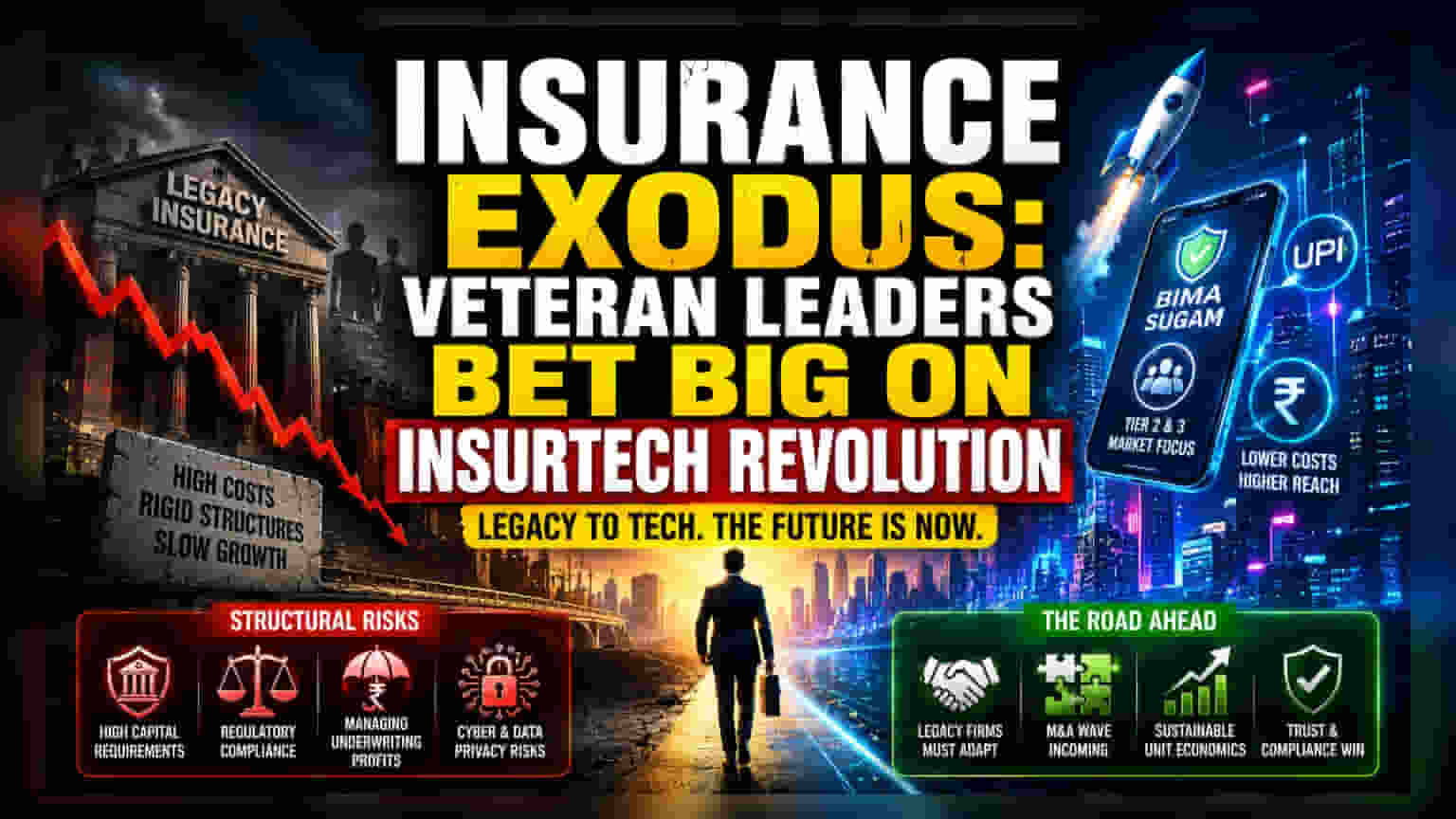

The Capital Shift Toward Insurtech

The exodus of veteran leadership from established insurance giants represents more than a career pivot; it signals a fundamental reassessment of distribution economics in the Indian market. By moving from legacy operations—often burdened by high acquisition costs and rigid hierarchical structures—toward nimble, tech-driven models, these executives are betting that the traditional insurance playbook is obsolete. The departure of former Generali India chief Anup Rau follows a clear strategic blueprint recently adopted by peers such as Neelesh Garg and Anuj Tyagi, who have similarly sought to capitalize on the widening gap between India's actual insurance coverage and its potential capacity.

Digital Infrastructure as the Primary Catalyst

While legacy firms struggle with the overhead of physical branch networks, the new generation of insurance ventures is leveraging India’s public digital infrastructure. The integration of the Bima Sugam platform and the ubiquity of UPI-based payments have dramatically lowered the barrier to entry for acquiring customers in Tier-2 and Tier-3 markets. This structural shift allows new entrants to bypass the expensive intermediary networks that historically compressed profit margins for established players. Consequently, private equity and venture capital firms are increasingly willing to fund these startups, viewing them as high-alpha plays in a sector where GDP-linked growth is inevitable but traditional distribution remains inefficient.

The Structural Risk of Scaling

Despite the bullish sentiment surrounding the insurtech space, the path to profitability remains fraught with regulatory and operational hazards. Startups attempting to replicate the scale of incumbents like HDFC Ergo or Tata AIG must grapple with the intensive capital requirements mandated by the Insurance Regulatory and Development Authority of India. Unlike agile fintech apps that operate on low-risk transactional models, insurance ventures carry massive long-term actuarial liabilities. Investors should monitor whether these new entities can maintain a healthy combined ratio while pursuing rapid growth, or if they will succumb to the same margin pressures that often plague established players during their initial expansion phases. The reliance on digital distribution also introduces vulnerability to cyber-security risks and changing data privacy regulations, which could necessitate significant unexpected compliance spending.

Future Outlook and Market Consolidation

Industry consensus suggests that the current wave of executive entrepreneurship will likely force legacy insurers to accelerate their own digital transformation agendas to remain competitive. As these startups begin their operational life cycles, the market will likely see a surge in M&A activity, with established insurance companies potentially acquiring these new ventures to buy back the innovation they failed to develop internally. The ultimate winner will not necessarily be the firm with the most sophisticated tech stack, but the one capable of navigating the complex regulatory environment while maintaining unit economics that satisfy both institutional investors and primary underwriting standards.