The Capital Allocation Strategy

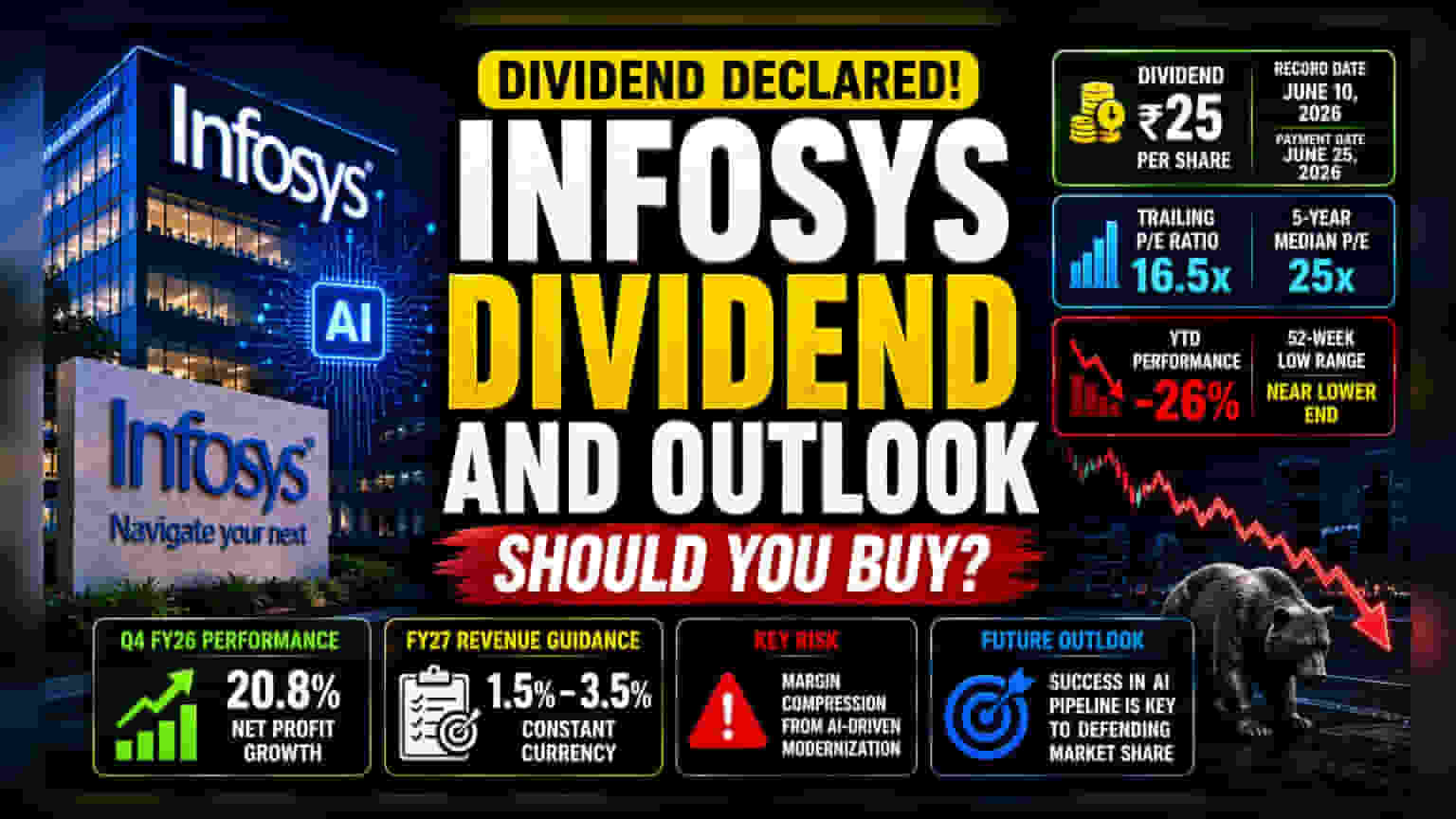

The Rs 25 per share dividend, scheduled for distribution on June 25, 2026, reinforces the company's reliance on dividend yields to anchor investor sentiment during a period of significant volatility. With the record date locked for June 10, the payout represents a consistent commitment to returning cash to shareholders, even as the firm navigates a transformative phase in the IT services sector. For long-term holders, this payout provides a predictable income stream, though it stands in sharp contrast to the capital-intensive investments required to pivot toward AI-integrated service models.

Valuation and Market Context

Trading at a trailing P/E ratio of approximately 16.5x, Infosys is currently situated well below its five-year median P/E of roughly 25x. This valuation gap suggests that the market is pricing in structural challenges rather than temporary cyclical downturns. While the company delivered a 20.8% net profit increase in Q4 FY26, year-to-date performance remains sluggish, with the stock down over 26% since the start of 2026. The divergence between resilient operational metrics and the declining share price points to an investor base wary of long-term sector disruption, specifically the cannibalization of legacy services by generative AI agents.

The Forensic Bear Case

The primary risk factor remains the compression of margins in traditional service lines. Unlike smaller, more agile competitors or pure-play AI firms, the company faces the 'modernization paradox'—where successfully automating client systems reduces the long-term billable hours that previously fueled double-digit revenue growth. Furthermore, the company’s FY27 revenue guidance of 1.5% to 3.5% (constant currency) is viewed by institutional analysts as conservative, potentially signaling a prolonged recovery window. Past volatility, including the severe 20% drawdown in February 2026, underscores the stock's sensitivity to macroeconomic shifts in the US and Europe, which remain the firm's largest revenue contributors. Any meaningful delay in client discretionary spending could further threaten the sustainability of these dividend payouts if free cash flow generation weakens.

The Future Outlook

While the dividend offers a tactical cushion, the strategic path forward depends on the company's ability to monetize its AI-augmented service pipeline. Analysts remain split on the timeline for this transition, with current sentiment reflecting a 'wait-and-see' approach regarding the firm’s ability to defend its market share against both niche digital disruptors and larger global competitors. With the stock currently trading near the lower end of its 52-week range, future price appreciation will likely depend on exceeding conservative growth forecasts in upcoming quarters rather than capital return programs alone.