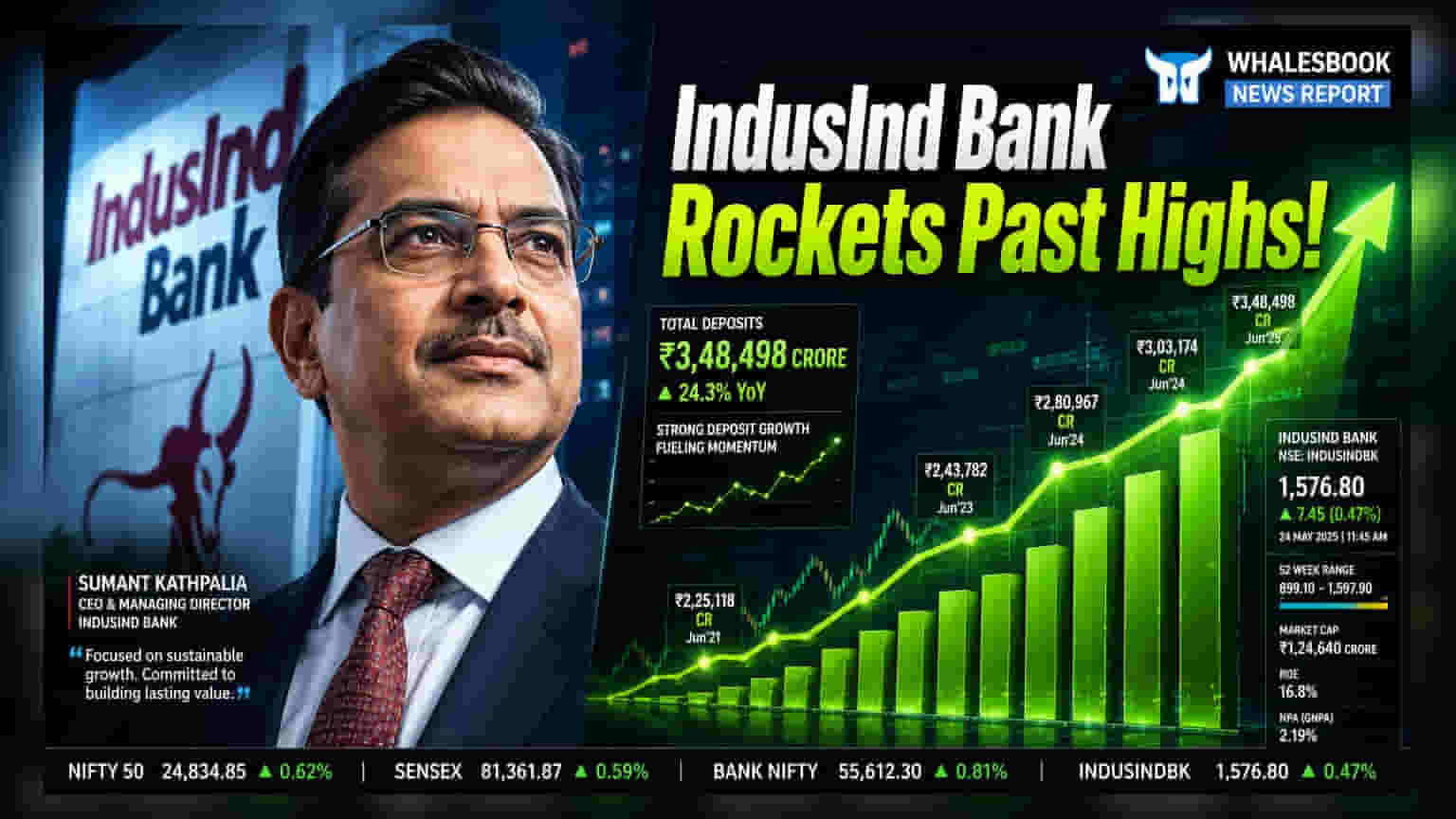

IndusInd Bank shares climbed to a 52-week high of ₹1,005.65 following a Q1 FY27 update showing 4.5% deposit growth. While deposit momentum remains steady, the bank faces pressure from a shrinking CASA ratio and cautious outlooks from rating agencies regarding profitability.

IndusInd Bank shares hit a new 52-week peak of ₹1,005.65 on Monday, recording a 3% intraday gain. This rise continues a four-day rally, during which the stock has gained roughly 10%, noticeably outperforming the broader BSE Sensex. The investor interest follows the release of the bank’s business update for the first quarter of the 2027 fiscal year.

Deposit Growth and CASA Challenges

For the quarter ending June 30, 2026, the bank reported total deposits of ₹4.14 trillion, reflecting a 4.5% year-on-year growth. However, the composition of these deposits remains a point of interest for investors. The Current Account Savings Account (CASA) ratio, which represents low-cost funds for the bank, contracted to 29.5% in Q1 FY27, down from 31.5% in the same period last year and 31.2% in the previous quarter. A lower CASA ratio often implies higher costs to maintain deposits, which can impact net interest margins.

While deposits grew, net advances stood at ₹3.26 trillion. Although this represents a 3.3% increase compared to the previous quarter, it marks a slight year-on-year decline of 2.3%. Investors will be watching whether the bank can balance its loan book growth while managing the cost of funds.

Rating Outlook and Profitability Concerns

Despite the positive stock price movement, India Ratings and Research (Ind-Ra) continues to maintain a 'Negative' outlook on the bank. The rating agency has pointed to a gradual reduction in the bank's market share for both advances and deposits over the last two years. Additionally, Ind-Ra raised concerns regarding a retail liquidity coverage ratio of 47.9% as of FY26 and high deposit costs.

Profitability is another area of focus. Projections indicate that the Return on Assets (RoA) may moderate to around 1% by the end of FY28, compared to the 1.8% average maintained during FY23 and FY24. Higher operating expenses related to scaling retail and SME (Small and Medium Enterprise) assets, along with necessary provisions for NPA (Non-Performing Asset) management and regulatory compliance, are expected to exert pressure on margins in the near term.

Asset Quality and Management Strategy

On the asset quality front, the bank reported a Gross NPA ratio of 3.43% for Q4 FY26, with Net NPA at 1%. Management has expressed confidence in controlling slippages throughout FY27 and intends to bring the Net NPA ratio down to approximately 0.6% over the medium term. They also noted that credit costs may have peaked, which could provide some relief to future earnings. The bank's management also indicated that there has been no material stress on the portfolio resulting from geopolitical conflicts in West Asia. The next important update for shareholders will be the full quarterly financial results, which will provide deeper insight into actual profit margins and the impact of the rising operating costs.