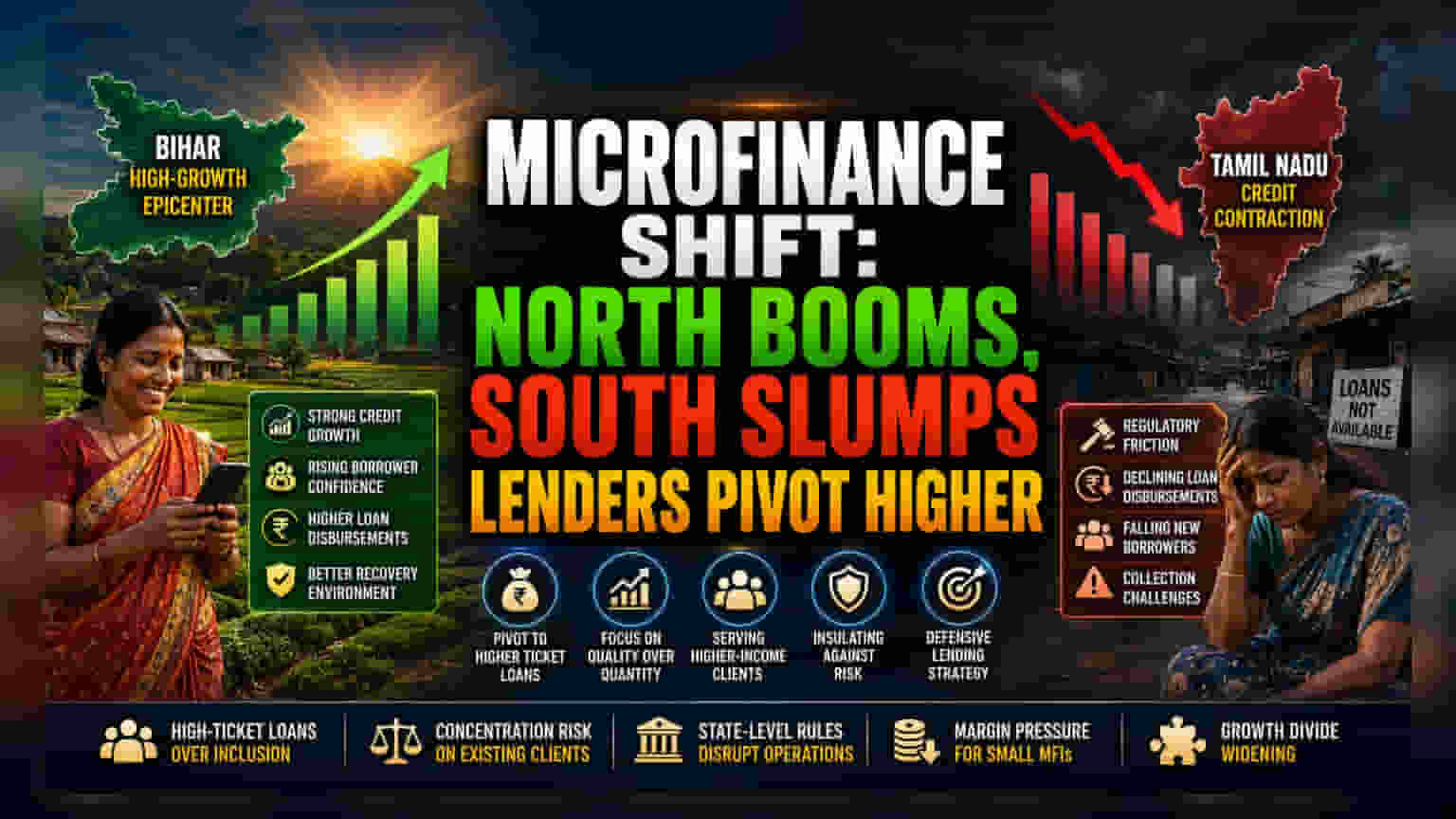

The Compression of Southern Micro-Credit

The national microfinance recovery appears robust on the surface, yet the regional concentration of capital is undergoing a profound transformation. While Bihar has consolidated its position as a high-growth epicenter, the stagnation in southern credit markets indicates that institutional lenders are pivoting away from historically saturated zones. The contraction in Tamil Nadu is not merely a statistical anomaly; it reflects a deliberate retreat by credit providers concerned by the impact of local regulatory constraints on collection efficiency and asset recovery timelines.

Strategic Pivot to High-Value Lending

Financial institutions are aggressively shifting their risk appetite by prioritizing larger loan tickets over the broader inclusion metrics that once defined the sector. This evolution toward higher-value originations suggests that lenders are insulating their balance sheets against the volatility of the sub-prime borrower segment. By pushing loans beyond the ₹80,000 threshold, institutions are effectively moving up the socio-economic ladder, leaving a vacuum for smaller, more vulnerable borrowers who are now facing diminished liquidity and limited access to credit facilities.

The Forensic Bear Case: Structural Risks

The reliance on high-ticket loan growth to mask declining borrower counts creates a fragility within the sector’s fundamental stability. When institutions prioritize the same loyal client base for larger loans, they increase their exposure to idiosyncratic risks rather than achieving true portfolio diversification. Furthermore, the persistent friction between Reserve Bank of India oversight and fragmented state-level legislative agendas introduces a recurring threat to operational continuity. Smaller microfinance entities, lacking the robust capital buffers of their bank-backed counterparts, face significant margin compression as they navigate these overlapping compliance requirements. Should economic headwinds increase, the tendency to favor existing, over-leveraged clients rather than acquiring new, lower-risk cohorts may trigger a spike in non-performing assets that current recovery narratives fail to account for.

Future Outlook and Sector Trajectory

Market participants should expect a continued flight to quality as lenders maintain a defensive posture. Institutional focus will likely remain concentrated on states where regulatory environments permit aggressive recovery tactics, leaving stagnant markets to suffer from sustained liquidity crunches. Unless a standardized national framework can harmonize collection practices across state lines, the divergence between the growth in northern states and the decline in the south is expected to widen, potentially necessitating further consolidation among smaller, liquidity-strapped institutions throughout the upcoming fiscal year.