What Happened

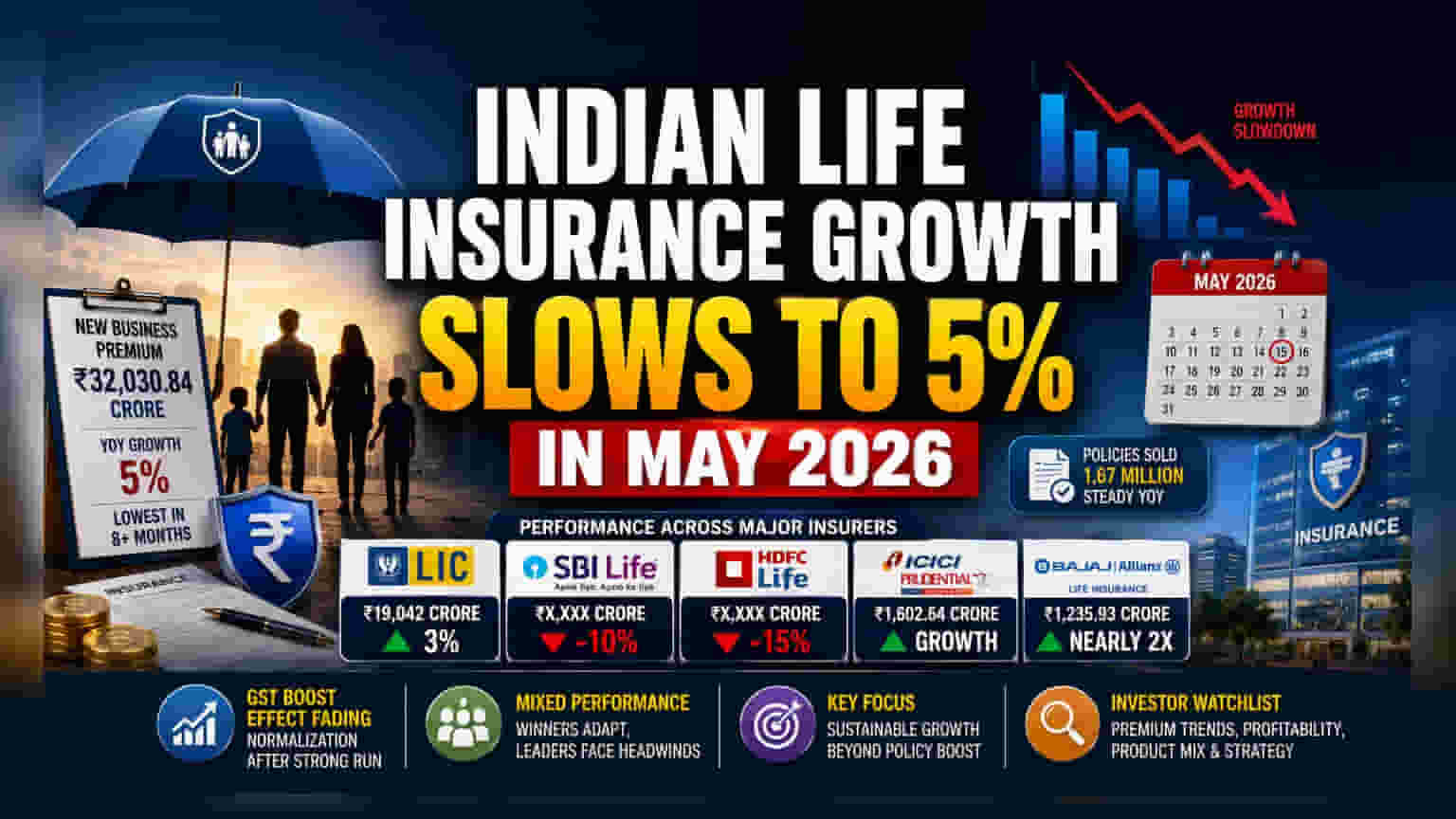

The Indian life insurance industry experienced a notable slowdown in May 2026, with year-on-year growth in new business premiums (NBP) falling to 5%. This is the lowest growth rate recorded by the sector in over eight months. The total new business premium collected reached ₹32,030.84 crore, compared to ₹30,463.21 crore in the same month last year. This performance stands in contrast to the rapid growth seen in April, when the industry reported a 39% surge, signaling that the initial boost from government policy changes is beginning to fade.

The Impact of Policy Changes

Investors are watching how the industry adjusts to the normalization of demand. In September 2025, the government introduced a GST exemption on individual life insurance products, including term policies. This change had acted as a major tailwind, driving strong growth in the months that followed. As that one-time impact tapers off, the sector is seeing a return to more moderate growth levels. The total number of policies sold, roughly 1.67 million in May, remained steady, suggesting that while the total premium growth has slowed, customer acquisition has not collapsed.

Performance Across Insurers

The performance among major players in the private sector showed a significant divide. Life Insurance Corporation of India (LIC) posted a 3% growth, bringing in ₹19,042 crore. Meanwhile, the collective group of 26 private life insurers reported an 8% growth, reaching ₹12,989 crore.

However, individual performance varied widely. SBI Life Insurance reported a 10% decline in its new business premiums, while HDFC Life Insurance saw a steeper drop of 15%. In contrast, ICICI Prudential Life Insurance managed to post growth, with its premium income rising to ₹1,602.64 crore. Bajaj Allianz Life Insurance stood out with a significant increase, nearly doubling its collections to ₹1,235.93 crore compared to the previous year.

How Investors May Read This

The uneven performance across top players highlights that market share and product mix matter greatly when the sector-wide tailwind of policy changes weakens. A decline in premium collection for large players like SBI Life and HDFC Life could indicate challenges in maintaining the rapid growth rates seen in early 2026. Conversely, the strong performance of others suggests that some companies are adapting better to the current environment, perhaps through more effective distribution or specific product offerings that continue to attract customers.

What Investors Should Track

Moving forward, the key factor for investors will be to monitor whether the 5% growth figure represents a temporary normalization or the start of a broader demand slowdown. Investors may track monthly premium data for individual companies to see if private insurers can regain momentum. Additionally, observing whether the stable number of policies sold leads to better profitability for these companies, even if premium growth is not as explosive as it was earlier in the year, will be crucial. Future management commentary regarding product mix and distribution strategy will be important to understand how these firms plan to grow without the artificial support of recent regulatory changes.