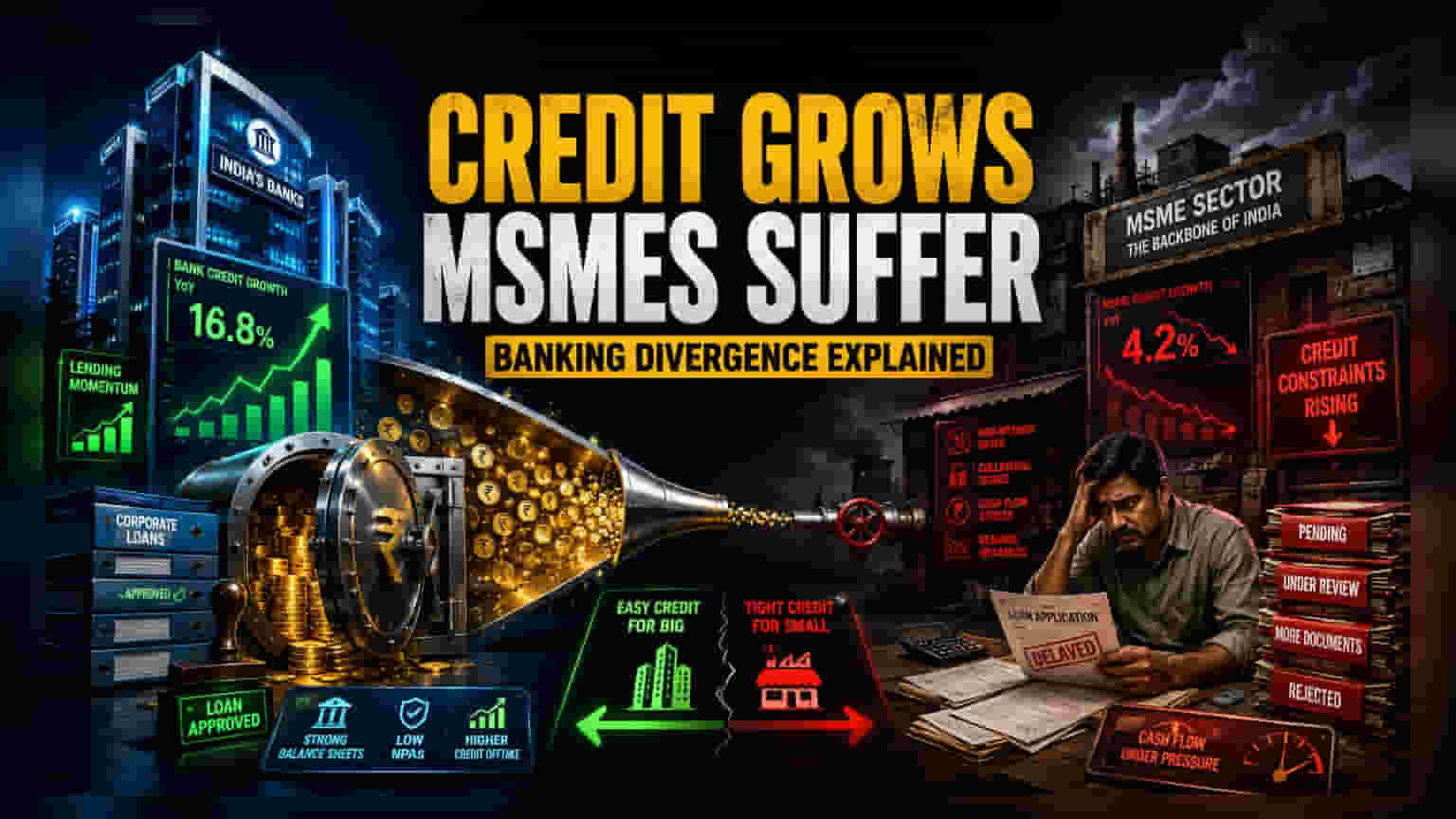

The Illusion of Credit Growth

Aggregate banking statistics often fail to capture the bifurcated nature of India’s current credit expansion. While the Reserve Bank of India reports double-digit growth in loan books, this figure is heavily skewed toward large corporates and retail consumption. Beneath these metrics lies a systematic reduction in risk appetite among both public and private sector lenders. Rather than expanding their reach to underserved segments, financial institutions are reinforcing their existing exposure to high-credit-score entities, effectively freezing out the MSME sector from affordable capital.

The Mechanics of Market Contraction

Financial institutions are recalibrating their internal risk models to prepare for potential interest rate volatility. Consequently, loan approval durations for micro-enterprises have surged by nearly 30% over the last two quarters. This bottleneck is not merely administrative; it is a deliberate capital allocation strategy. Banks are prioritizing high-collateral, low-risk loans to protect net interest margins as funding costs fluctuate. This trend places smaller firms at a distinct competitive disadvantage compared to their larger, cash-rich peers who maintain direct access to debt capital markets, further concentrating market share within dominant industrial players.

The Hidden Systemic Risk

Reliance on informal credit channels is on the rise as banks tighten their standards. This shift introduces significant hidden leverage into the economy. Historically, when traditional lenders retreat from the MSME space, defaults in the shadow banking sector tend to climb within twelve to eighteen months. The current strategy of defensive lending—while protecting individual bank balance sheets in the short term—creates a vacuum that could exacerbate sectoral debt distress. Unlike the resilient balance sheets of major private banks, smaller regional lenders are struggling to maintain liquidity, which threatens to trigger a localized credit crunch if the current risk-aversion trend persists through the end of the fiscal year.

Future Outlook and Sectoral Implications

Analysts expect the credit divergence to widen further as lenders favor firms with digitized, transparent cash flows. Businesses unable to demonstrate high operational efficiency or robust digital records will likely face continued exclusion from formal credit. The consensus among institutional observers suggests that unless there is a targeted government intervention or a significant easing in the cost of funds, the gap between large-scale enterprise accessibility and small-business capital starvation will remain a primary headwind for broader industrial expansion throughout the coming quarters.