India's banking system is seeing a record high loan-to-deposit ratio as credit demand outstrips deposit collection. This funding gap is forcing lenders to manage liquidity carefully, with private banks shedding high-cost deposits to protect profit margins while PSU banks lose deposit market share.

What Happened

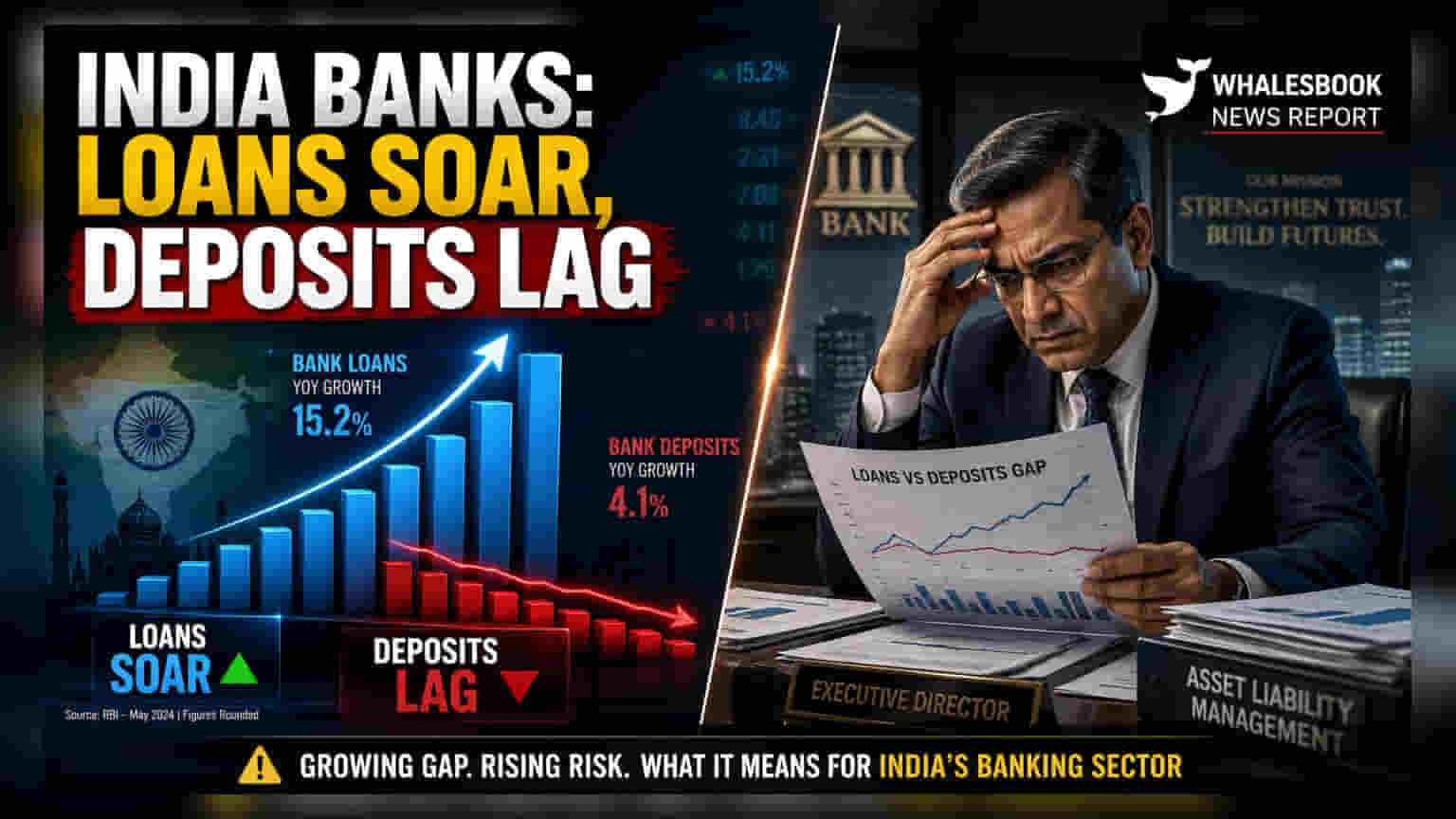

Indian banks are facing a challenging period as credit disbursement continues to outpace deposit mobilization. By mid-June 2026, deposit growth remained at approximately 12.2% year-on-year, while loan growth surged ahead, creating a credit-deposit growth gap of 5.4%. This widening disparity has pushed the banking system's loan-to-deposit (LDR) ratio to 82.7%, a level not observed in over a decade. While corporate and retail demand remains strong, the inability of banks to attract sufficient deposits is creating a structural funding squeeze that requires careful management of liabilities.

The Growth Mismatch

Several lenders reported robust loan growth during the first quarter of fiscal year 2027. Central Bank led the sector with approximately 28.8% year-on-year growth in global advances. Other notable performers included Tamilnad Mercantile Bank at 27%, Dhanlaxmi Bank at 26.5%, and J&K Bank at 25.5%. These gains were supported by sustained appetite from the retail, agriculture, and MSME sectors, as well as corporate borrowing. However, this aggressive lending is putting pressure on the liquidity buffers of these institutions.

Why Private Banks Are Shedding Deposits

A distinct trend has emerged among private lenders who are actively managing their balance sheets to protect profit margins. RBL Bank saw a 10.2% sequential decline in total deposits, largely due to the maturity of high-cost wholesale deposits. IDBI Bank and Bank of Baroda also recorded sequential deposit declines of 6.3% and 0.9%, respectively. By letting go of expensive bulk deposits, these banks are prioritizing profitability over sheer volume, a strategy aimed at insulating their net interest margins from the rising cost of funds.

Challenges for Public Sector Banks

While private banks manage their cost of funds, public sector banks (PSUs) are struggling with market share. According to data tracked by analysts, deposit growth for PSU banks has been around 10.7% year-on-year, consistently trailing the broader system's 12% growth. As PSU banks lose ground in the race for customer deposits, they face the risk of needing to rely on more expensive market-based funding to support their ongoing loan books.

Factors Influencing Credit Demand

The unexpected strength in credit demand during a typically quieter quarter is driven by specific economic factors. Increased borrowing by oil companies, extended working capital cycles due to supply chain issues linked to West Asia, and government-backed emergency credit schemes have kept loan demand high. Since retail fuel prices have not fully reflected global crude price volatility, oil companies have turned to banks for liquidity, adding to the total credit demand.

What Investors Should Track

Investors should monitor the credit-deposit ratio in upcoming quarterly filings to see if banks can bridge the funding gap. Key monitorables include the share of low-cost CASA (Current Account Savings Account) deposits, as a shift toward higher-cost term deposits can squeeze net interest margins. Additionally, tracking the cost of funds and any changes in lending rates will be crucial to understanding how effectively banks are navigating this liquidity environment.