The insurance regulator plans to overhaul commission structures by January 2027. Payments will be linked to product complexity and policy renewals to improve transparency and reduce mis-selling. These changes aim to shift the industry focus toward long-term customer value rather than high initial sales incentives.

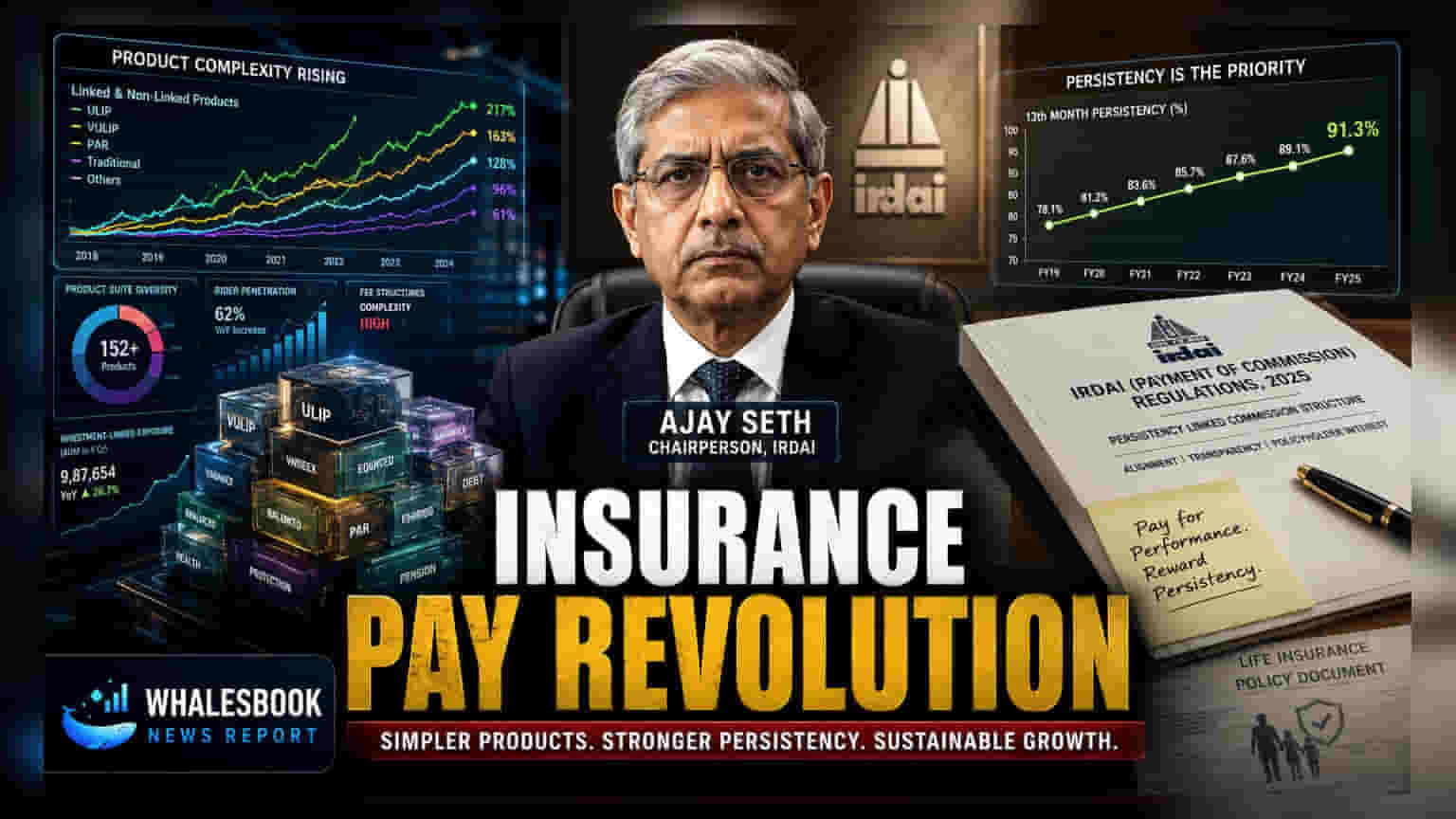

The Insurance Regulatory and Development Authority of India (IRDAI) has released a consultation paper aimed at restructuring how insurance agents and distributors are compensated. This move represents a shift in the regulatory approach toward the insurance industry, moving away from a one-size-fits-all commission model to one that rewards transparency and long-term service quality.

Linking Pay to Product Type and Renewals

A central feature of the proposal is the plan to tie commissions directly to the type of product sold. Under the current structure, agents often receive a standard commission regardless of the effort or advice required. The regulator suggests that simpler products, such as basic term life or health insurance plans, may carry lower commission rates. Conversely, more complex financial products like Unit Linked Insurance Plans (ULIPs) or annuities—which often require ongoing advisory support—could justify different remuneration levels.

Additionally, the regulator wants to tie a portion of distributor pay to policy persistency. Persistency refers to the rate at which customers continue to renew their policies over several years. In the industry, low renewal rates are frequently viewed as a sign of aggressive selling or products that do not actually meet the buyer's needs. By making pay dependent on whether a customer stays with the policy, the IRDAI aims to encourage agents to prioritize long-term customer interests over immediate sales.

Mandatory Disclosure and Industry Impact

The regulator is also pushing for mandatory public disclosure of commission policies by all insurance companies. While there are existing caps on how much commission an insurer can pay, the internal details regarding how these payouts vary across different channels—such as individual agents, bank partners, and insurance brokers—have historically been less transparent. Greater disclosure is expected to provide regulators and policyholders with a clearer view of the costs involved, potentially reducing conflicts of interest that occur when high upfront commissions lead to the sale of unsuitable products.

These proposed reforms are currently in the discussion phase. The IRDAI is inviting feedback from insurance companies and other market participants before finalizing the framework. While the target implementation date is January 2027, the exact structure of these new models will depend on the responses received during this consultation process.

For investors, the key monitorable will be how these changes affect the operational margins of insurance companies and the revenue models of bancassurance partners, which are banks that sell insurance products. Companies that have historically relied heavily on aggressive upfront commission models may need to adjust their business strategies to align with these new, service-oriented incentives.