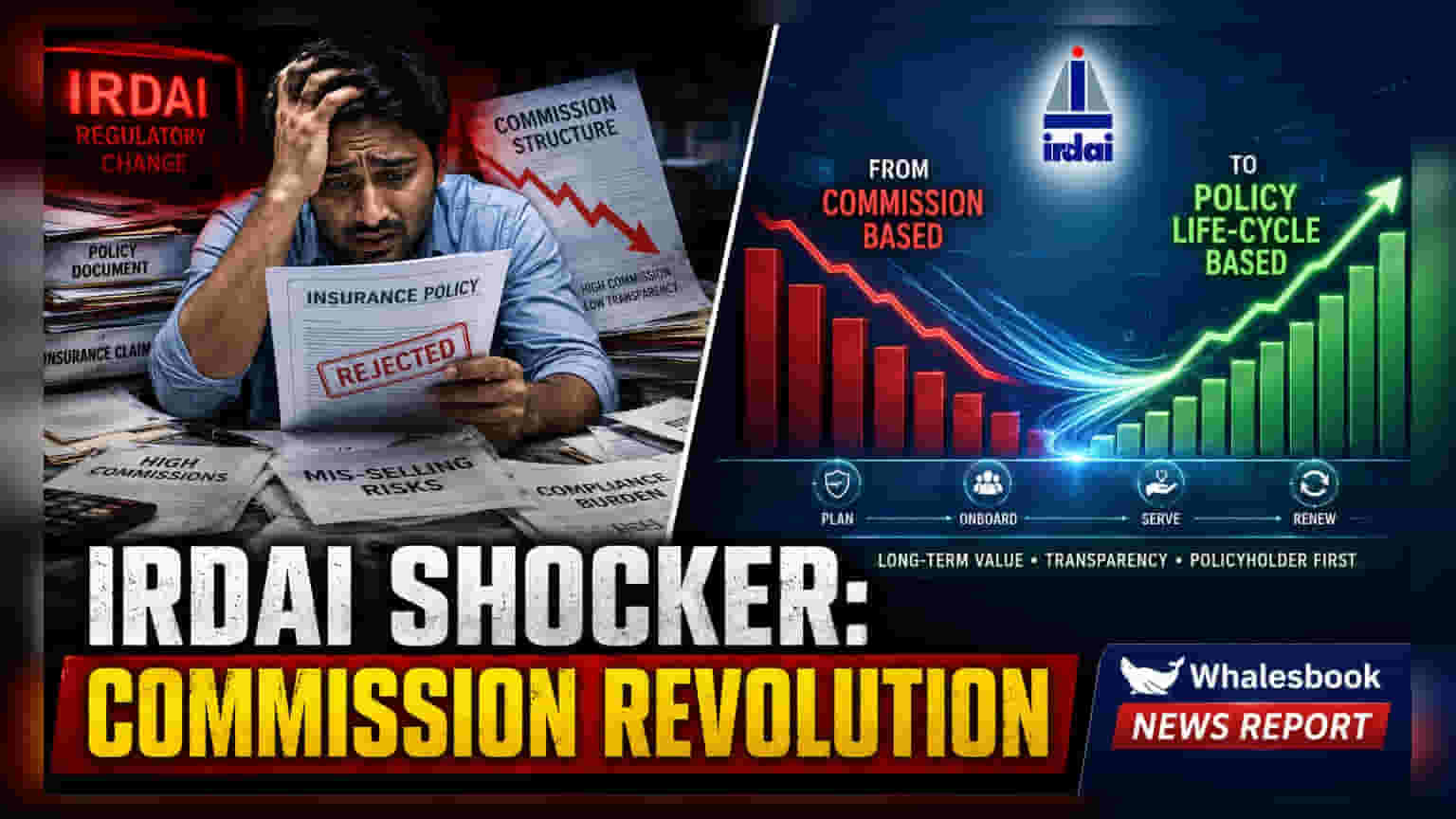

The insurance regulator plans to shift agent commissions from large upfront payouts to staggered, life-of-policy payments. This change aims to reduce mis-selling by aligning distributor incentives with long-term customer interests rather than initial sales volume.

What Happened

The Insurance Regulatory and Development Authority of India (IRDAI) is planning a major overhaul of how insurance agents and distributors are paid. The regulator is working on a framework to move away from the current system, where a significant portion of commission is paid upfront when a policy is sold. Instead, the new model proposes spreading these payments over the entire duration of the policy. IRDAI Chairman Ajay Seth has indicated that a consultation paper regarding these distribution reforms is expected by the end of July 2026.

Why This Matters For Investors

Currently, agents can receive as much as 40% of the first-year premium as an upfront commission on certain insurance and investment-linked products. Financial experts and the regulator have noted that this system often encourages sales staff to prioritize high-volume selling over whether a policy actually meets a customer's specific financial needs. By moving to a staggered payout model, the regulator intends to ensure that distributors remain committed to the customer for the life of the policy, which could improve policy retention rates and customer trust in the long run.

The Impact On Insurance Companies

For listed insurance companies like Life Insurance Corporation of India (LIC), HDFC Life Insurance, and ICICI Prudential Life Insurance, this shift could change how they manage their operating expenses. If commissions are spread over many years, the immediate cash outflow for acquiring new customers may decrease. However, companies will need to adjust their internal accounting and incentive systems to match these regulatory requirements. Increased transparency and a focus on long-term service could also shift competition away from aggressive sales tactics toward providing better personalized advice and easier claim assistance.

Sector Context And Market Reach

India’s insurance sector currently sees annual gross premium collections exceeding ₹11.9 lakh crore. Despite this large figure, the country's insurance penetration remains relatively low at 3.7% of GDP. The government has previously introduced measures like 100% Foreign Direct Investment (FDI) and tax adjustments for health insurance to improve these numbers. The upcoming commission reforms are another step in the broader effort to align India’s insurance practices with global standards seen in the US, UK, and Europe.

What Investors Should Track

The most important monitorable is the upcoming consultation paper from IRDAI. Investors should watch for specific details on commission caps, how different product categories are treated, and the implementation timeline. Additionally, management commentary from major life insurers during upcoming quarterly earnings calls will be critical to understand how these proposed changes might affect their new business margins and long-term operating costs.