Homebuyers often focus only on interest rates, but processing fees, legal charges, and tenure decisions can significantly inflate the total loan cost. Understanding these hidden expenses is essential for long-term financial health.

What Happened

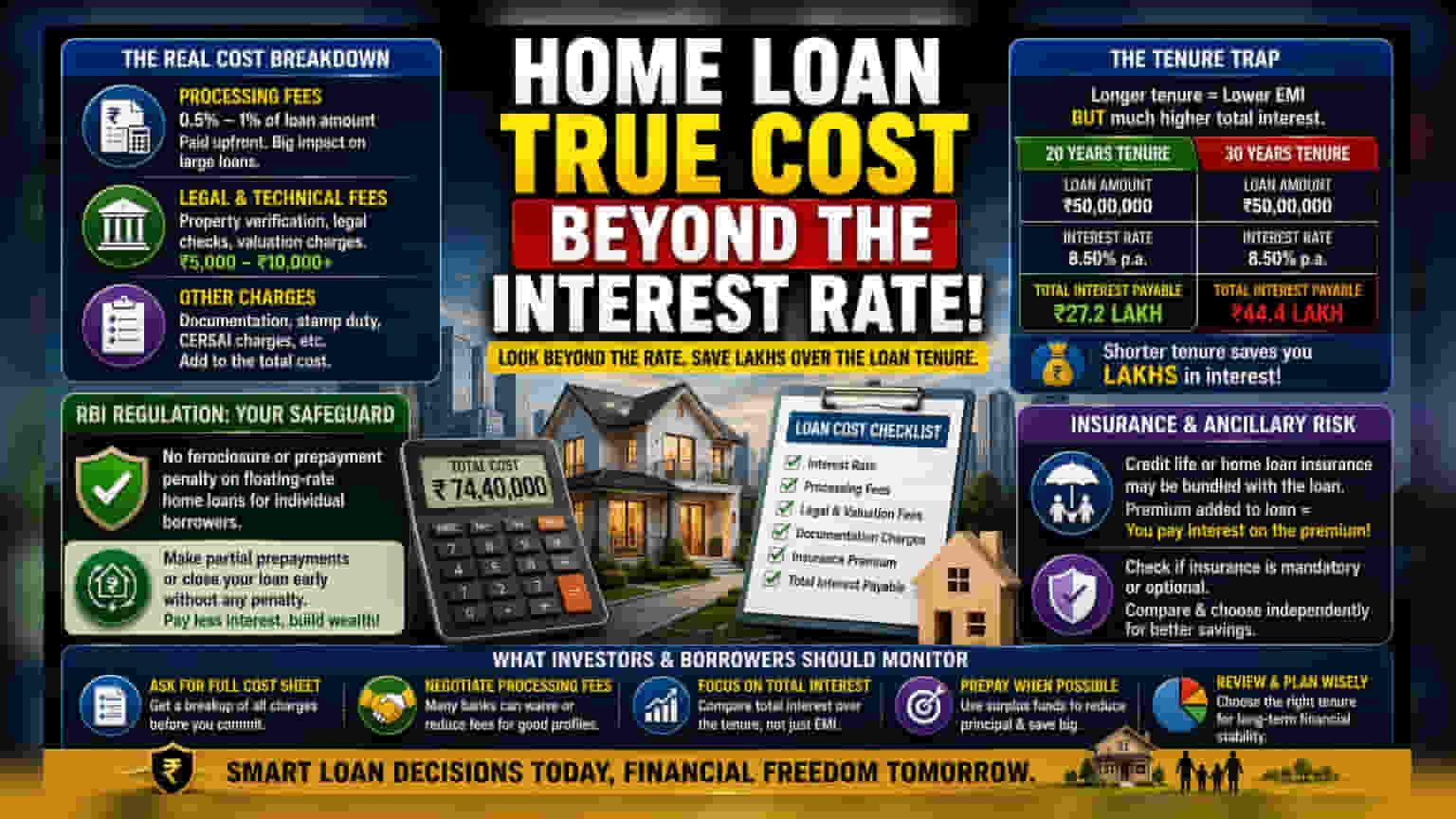

When choosing a home loan, most borrowers focus heavily on the advertised interest rate. While the rate is a primary factor, it often fails to represent the full financial impact of the loan. In addition to the interest, several ancillary costs and structural decisions can significantly increase the total amount a borrower pays over the life of the loan.

The Real Cost Breakdown

Home loans come with a set of charges that are often deducted upfront or added to the loan balance. Processing fees, which are essentially the administrative costs charged by the bank, typically range between 0.5% and 1% of the total loan amount. While this might seem like a small percentage, on a large loan, it translates to a significant upfront payment. Additionally, banks levy legal and technical valuation charges to verify property titles and assess market value. These fees can range from a few thousand to over ten thousand rupees, depending on the property's location and value.

The Tenure Trap

A common strategy for managing monthly cash flow is to opt for the longest available loan tenure, often up to 30 years, to keep the Equated Monthly Installment (EMI) as low as possible. While this provides immediate relief to the monthly budget, it creates a much higher total interest outgo over the long term. Because interest is calculated on the reducing principal balance, a longer duration means the borrower pays interest for more years, effectively increasing the total cost of the house significantly compared to a shorter-tenure loan.

The Regulatory Angle

It is important for borrowers to understand current regulations regarding loan modifications. Under Reserve Bank of India (RBI) guidelines, banks are generally prohibited from charging foreclosure or prepayment penalties on floating-rate home loans for individual borrowers. This is a crucial financial safeguard. If a borrower has extra funds and chooses to make a partial prepayment or close the loan early, this rule ensures they are not penalized for reducing their principal balance ahead of schedule, which is one of the most effective ways to reduce total interest outgo.

The Insurance and Ancillary Risk

Many lenders may bundle credit life or home loan insurance with the loan product. In some cases, the insurance premium is added to the loan amount, meaning the borrower pays interest on the premium itself. While having insurance is a prudent financial decision, borrowers should clarify if the insurance is mandatory or optional and whether they can source it independently, which might be more cost-effective.

What Investors and Borrowers Should Monitor

When evaluating a home loan offer, the focus should shift from the headline interest rate to the total cost of ownership. Borrowers may find it useful to ask for a full list of all upfront charges, including processing, legal, and documentation fees. It is also common practice to negotiate the processing fee, as banks often have flexibility in waiving or reducing these charges for creditworthy customers. Finally, tracking the total interest paid over the entire tenure is more important than focusing solely on the monthly EMI. Understanding these factors helps in making a decision that aligns with long-term financial stability rather than just short-term cash flow management.